Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

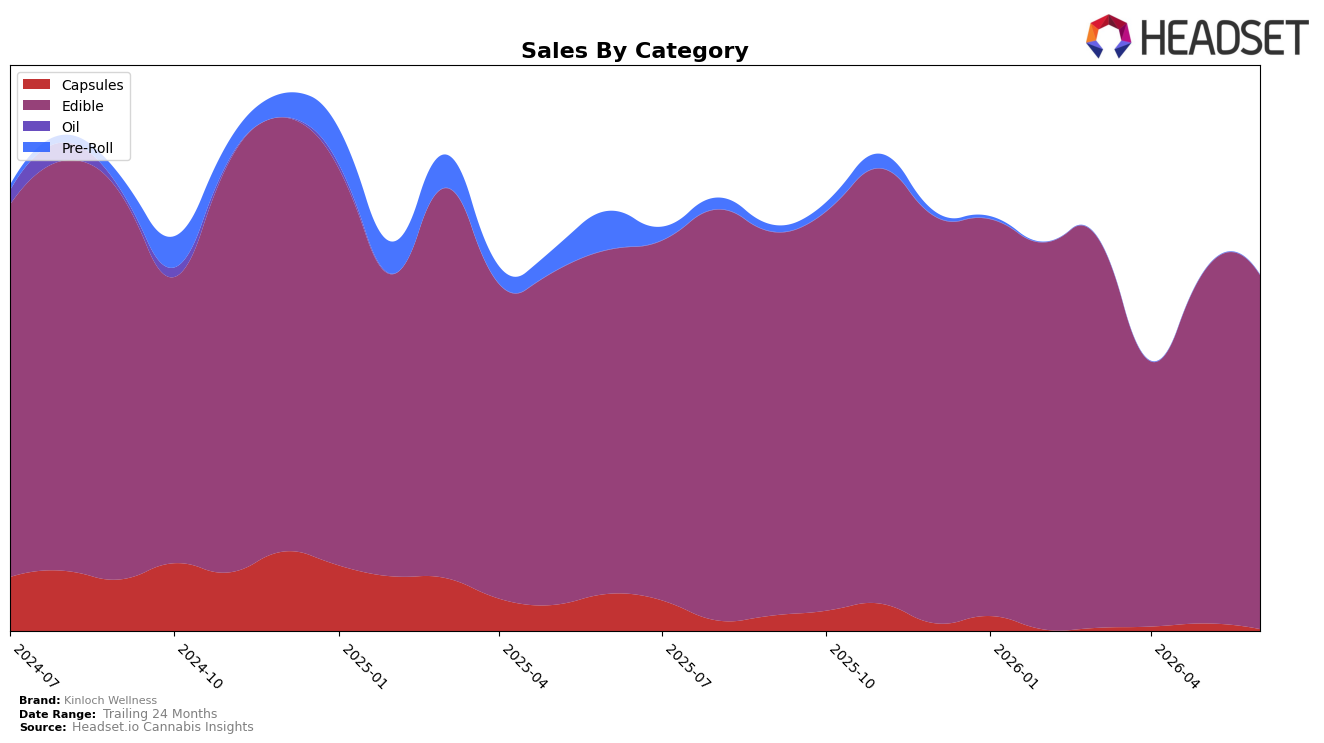

In June 2026, Kinloch Wellness concentrated 99.52% of sales in Edible, up 2.95% year over year and 0.35% month over month, while Capsules fell to 0.48% share with a 95.36% YoY decline and a 76.63% MoM drop; together with an Edible average price of $29.29 and a brand-level average price up 32.18% YoY, this mix shows consolidation rather than diversification. With Edible ranked 18th in Ontario and overall brand sales down 15.14% YoY despite category-level stability, the pattern implies Kinloch Wellness is increasingly reliant on Edible for volume while price and shrinking Capsules exposure are not offsetting unit pressure.

The near-total pivot into Edible at 99.52% share alongside a 2.95% YoY category uptick and a 15.14% YoY brand sales decline indicates that price-led strategy (average price +32.18% YoY) is outpacing demand elasticity; the 0.35% MoM Edible gain versus a 76.63% MoM Capsules contraction suggests short-term steadiness is coming from a single format. Holding the 18 rank in Ontario while Capsules collapse by 95.36% YoY implies Kinloch Wellness is positioned as an Edible specialist with limited cross-category hedge, and the thesis is that maintaining share will require either moderating price in Edible or reintroducing a viable second category to stabilize units.

Competitive Landscape

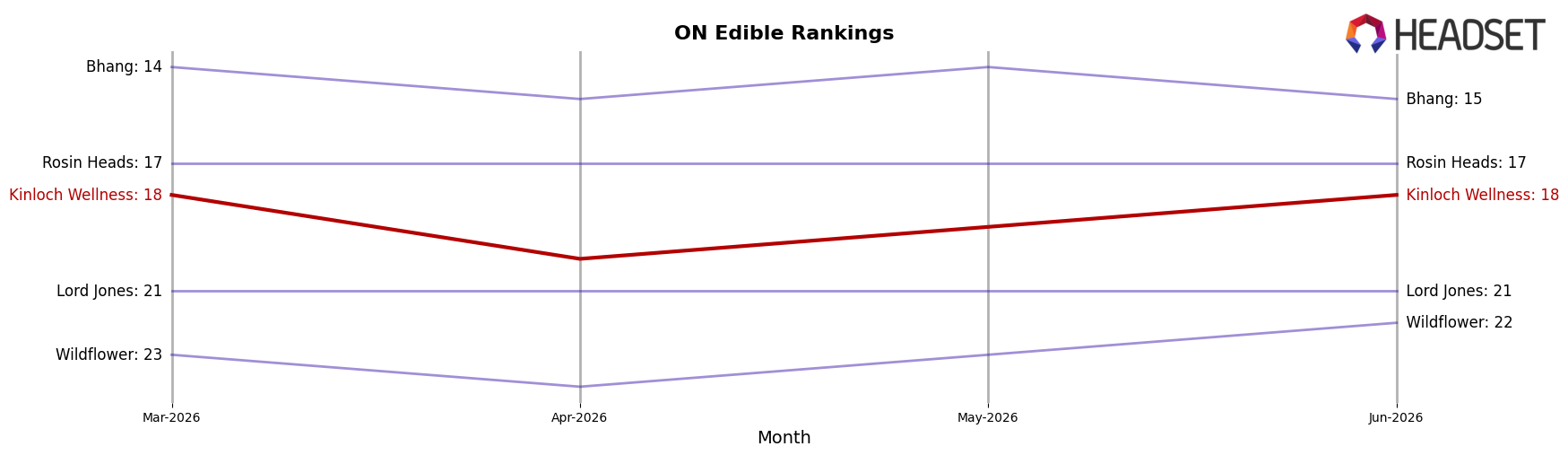

Kinloch Wellness sits at rank #18 in ON Edible in June 2026, improving 4 positions from #22 year over year, while holding flat versus March 2026 at #18; by contrast, Wyld moved up from #4 to #3 and Olli climbed from #7 to #4, indicating faster upward mobility among leaders. Kinloch Wellness also reached its peak rank of #18 in June 2026, whereas Spinach maintained #1 year over year and Gron / Grön held #2, reinforcing a stable top tier that has not ceded spots despite Olli’s 120.7% sales growth and Wyld’s 21.9% increase. The pattern implies Kinloch Wellness’s modest rank gain amid a static three-month position and entrenched top-five movement will require share capture from mid-tier neighbors rather than displacing the top cohort in the near term.

Notable Products

CBN:CBD Softgels 4-Pack (40mg CBN, 80mg CBD) posted the sharpest move in June 2026 with +235.4% MoM, leaping into rank 6, while CBZ CBD/CBN 2:1 Pomegranate Berry Gummy 4-Pack (80mg CBD, 40mg CBN) plunged -87.2% MoM to rank 5, signaling a redistribution from nighttime CBN gummies toward capsule formats. Serene7f- CBD Green Apple Gummy 30-Pack (1500mg CBD) held rank 1 despite a -5.9% MoM dip, and three of the top five are Edibles with two registering +53.2% and +139.4% MoM gains that outpaced the rank-stable leader. Refresh - CBD:CBG 1:1 Mango Gummies 15-Pack (300mg CBD, 300mg CBG) surged +139.4% MoM to rank 3 as Elevate7f CBD Blackberry Lemon Gummy 30-Pack (900mg CBD) climbed +53.2% MoM to rank 4, while the smaller Refresh - CBD/CBG 1:1 Mango Gummies 4-Pack (80mg CBD, 80mg CBG) advanced +47.4% MoM to rank 2 on $2,197 sales. The pattern implies Kinloch Wellness is tilting toward higher-potency multipack gummies and reintroducing capsules as a complementary nighttime solution, concentrating volume in large-format Edibles while pruning weaker CBN-forward SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.