Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

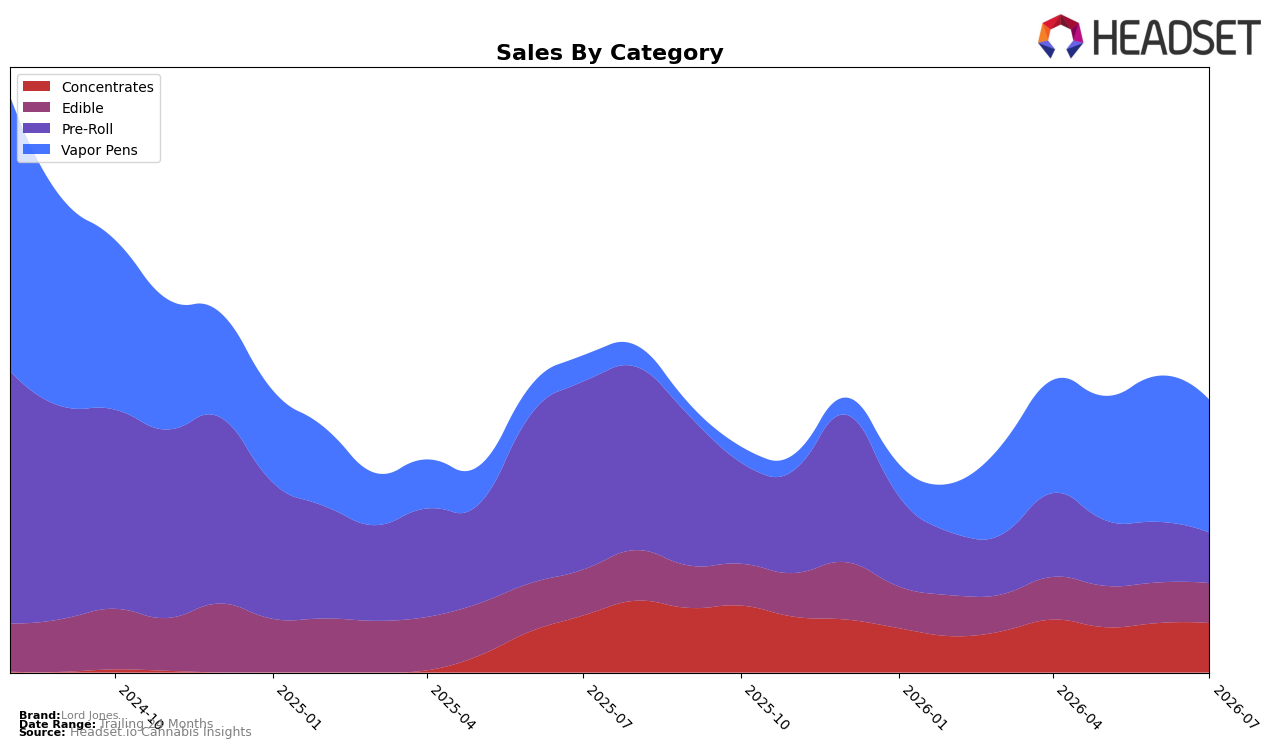

In July 2026, Lord Jones shifted toward Vapor Pens, which held 48.75% share with 410.24% year-over-year growth but a 9.10% month-over-month decline, while Pre-Roll dropped to 18.50% share with a 73.23% year-over-year contraction and a 16.69% month-over-month pullback. Concentrates maintained 18.16% share with a 13.27% year-over-year decline and a flat 0.15% month-over-month uptick, and Edible held 14.60% share with a 13.01% year-over-year decline and a 1.63% month-over-month dip. Despite brand-level sales down 14.08% year over year and average price up 10.05%, the surge in Vapor Pens mix alongside broad declines elsewhere indicates a concentration strategy that is masking weakness in legacy formats.

The category tilt implies Lord Jones is trading breadth for depth: Vapor Pens’ rapid year-over-year expansion alongside a month-over-month softening and a Vapor Pens rank of 25 in Saskatchewan suggests the brand is gaining relevance in a single growth lane while ceding ground in Pre-Roll and Edible. With Ontario as the leading province and Vapor Pens carrying a materially higher average price than Edible, the mix shift points to a pricing and positioning move up the value ladder, but the 48.73% two-year sales decline combined with category contraction in Pre-Roll and Edible signals vulnerability if Vapor Pens momentum normalizes.

Competitive Landscape

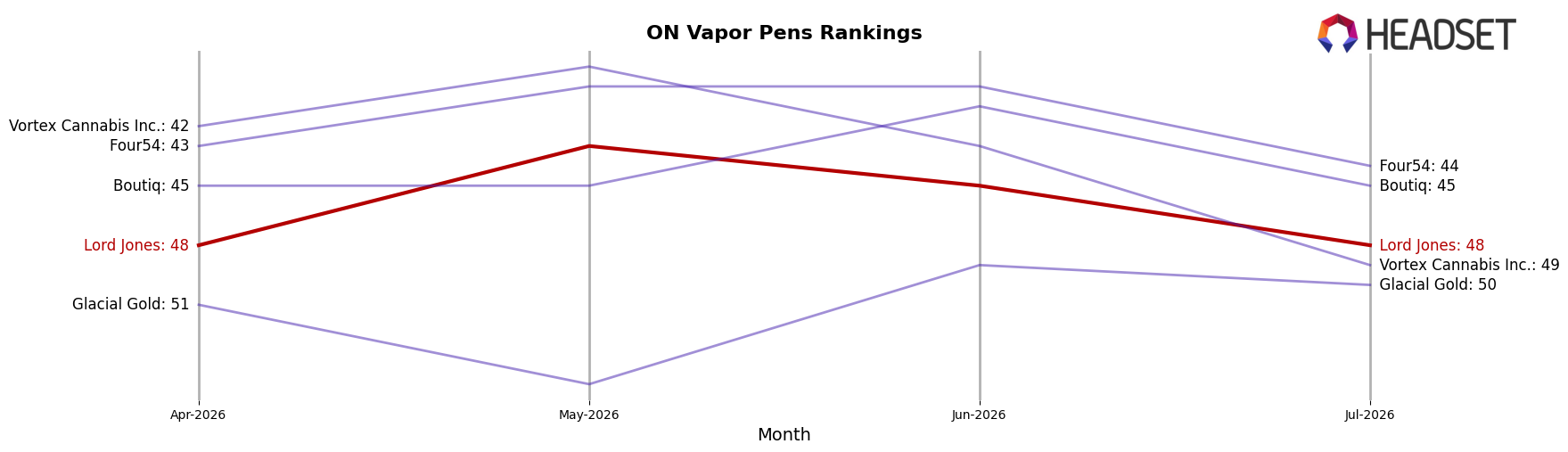

Lord Jones sits at rank #48 in ON Vapor Pens in July 2026, improving 40 positions from #88 year over year, yet remaining flat versus April 2026 at #48; this follows a retreat from a peak at #23 in August 2024, a 25-rank slide over 23 months. In contrast, Spinach climbed from #4 to #1 with 144.7% YoY sales growth, while Back Forty / Back 40 Cannabis edged from #1 to #2 despite 9.3% YoY growth, indicating that Lord Jones’s rebound in rank has not broken into the top tier; the pattern implies stabilization off a mid-2024 high but a need for incremental share capture to convert YoY rank gains into sustained top-30 presence.

Notable Products

Cookies & Cream Fusion Chocolate 5-Pack (10mg) posted the steepest move in July 2026 with a -20.6% MoM decline and slid to rank 4, while Orange Velvet Live Resin Caviar (1g) fell -22.9% to rank 9, signaling pressure on non-core SKUs. In contrast, Hash Fusions -Taster Infused Pre-Roll 3-Pack (1.5g) climbed +16.1% MoM to rank 2 and Gorilla Grape Live Resin Caviar (1g) rose +17.7% to rank 6, but Sour Blueberry Liquid Diamonds Live Cartridge (1g) dipped -1.5% at rank 5. Two Vapor Pens SKUs sit in the top 10 alongside two Concentrates and two Edibles, and the top-ranked CBD/THC 1:1 Salted Caramel Crunch Fusions Chocolate 5-Pack (10mg CBD, 10mg THC) grew +3.2% MoM at rank 1 with $64,671, whereas Gorilla Grape Liquid Diamonds Live Resin Cartridge (1g) dropped -20.3% to rank 8. The pattern implies a tilt toward inhalables driving momentum while legacy Edibles fragment, suggesting prioritization of Pre-Rolls and select Concentrates over broader flavor extensions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.