Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Lime is stocked at 218 licensed dispensaries across California, with the deepest coverage in Los Angeles, Sacramento, San Diego, San Jose, and Santa Rosa. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

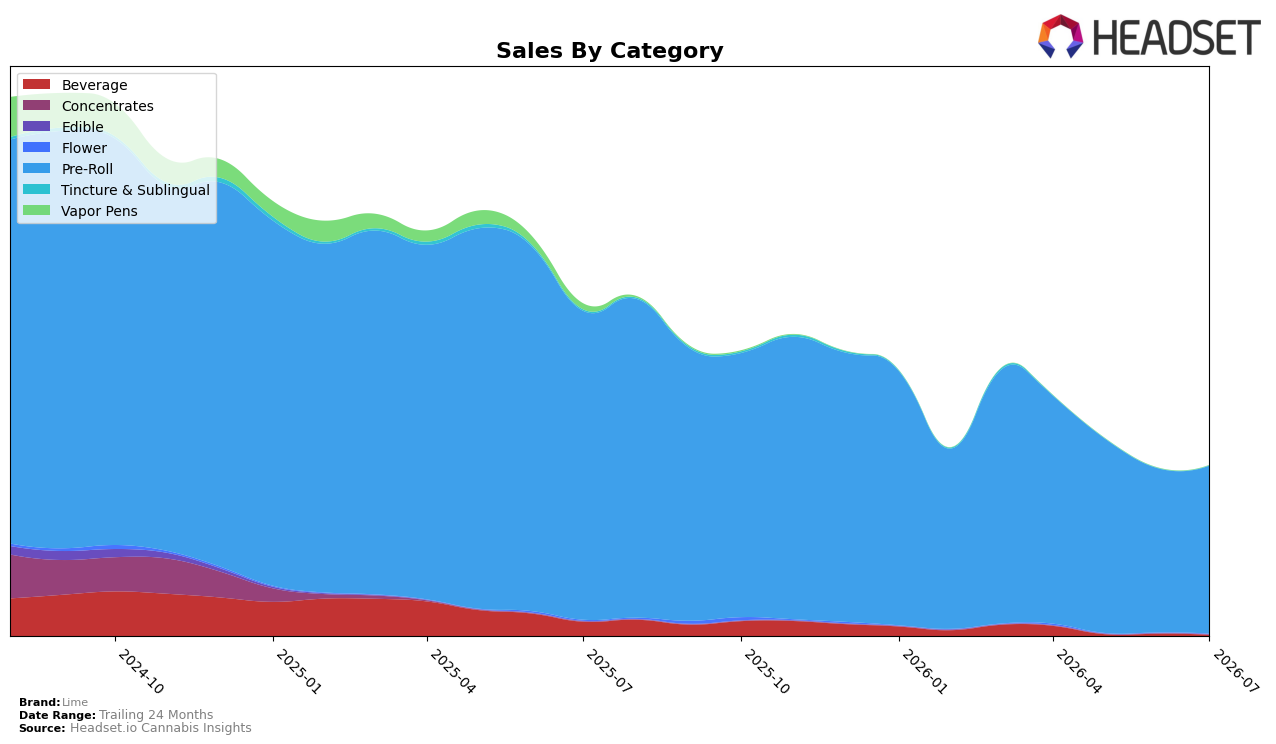

Pre-Roll accounted for 99.46% share in July 2026 while Beverage held 0.54%, with Pre-Roll down 45.65% year over year and up 2.34% month over month, versus Beverage down 93.58% year over year and down 56.87% month over month. Against a brand-level sales decline of 48.95% year over year and a 22.66% year-over-year drop in average price, the mix skew toward Pre-Roll consolidates Lime’s reliance on a single category while the steep Beverage contraction reduces diversification, implying concentration risk even as Pre-Roll’s month-over-month uptick cushions sequential volatility.

Holding rank 25 in Pre-Roll in California while Pre-Roll commands 99.46% of sales, and with average price at $11.21 alongside a 22.66% year-over-year price decline, positions Lime as a value-leaning Pre-Roll player rather than a multi-category operator. The 2.34% month-over-month Pre-Roll gain paired with a 56.87% month-over-month Beverage drop suggests that incremental share defense will come from pricing and pack architecture within Pre-Roll, not cross-category expansion, implying near-term positioning centered on price-elastic, high-volume Pre-Roll segments rather than premium or niche adjacencies.

Competitive Landscape

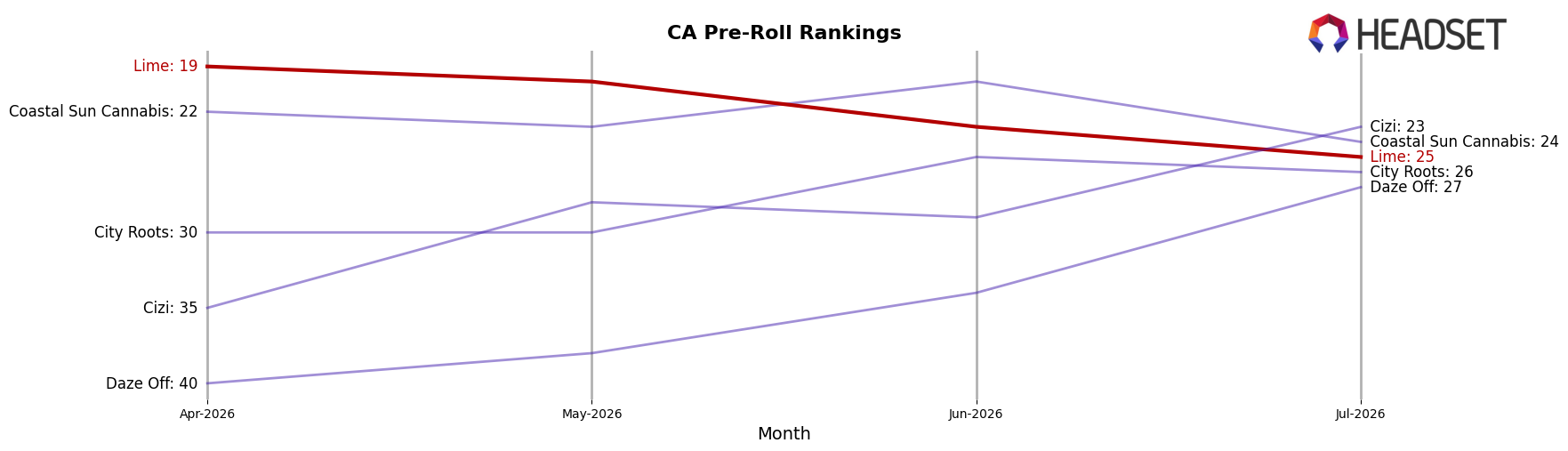

Lime sits at rank #25 in CA Pre-Roll in July 2026, down 14 positions year over year from #11 and 6 positions since April 2026 when it was #19, while its prior peak at #9 in December 2024 marks a 16-position slide from that high; by contrast, Jeeter held #1 both this year and last as its sales grew 6.1% year over year, and STIIIZY maintained #2 with a 12.9% year-over-year lift, indicating Lime is losing relative share as top-tier incumbents consolidate rank stability. This pattern implies Lime’s trajectory is one of sustained rank erosion driven by stronger year-over-year momentum among leaders, requiring a shift toward regaining velocity against competitors widening their advantage.

Notable Products

Lil Limes - Alien Gas Live Resin Hash Infused Pre-Roll (0.6g) slid 19.5% month over month to rank 4, while Lil' Lime - Purple Zaza Diamond And Hash Infused Pre-Roll (0.6g) climbed 40.4% to rank 2, indicating mix volatility concentrated in minis. Lil Lime - Maui Wowie Live Resin Hash Infused Mini Pre-Roll (0.6g) rose 23.0% to take rank 1, and the Lil Limes - Maui Wowie Live Resin Hash Infused Pre-Roll 5-Pack (3g) dipped 8.5% at rank 8 with $33,937 in July 2026 sales, framing a split where single minis accelerate as larger pack formats soften. With eight of the top ten SKUs in Pre-Roll minis or infused formats, July 2026 demand is consolidating around smaller, potency-forward options, implying Lime’s product strategy is tilting toward high-velocity minis over bulk units.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.