Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

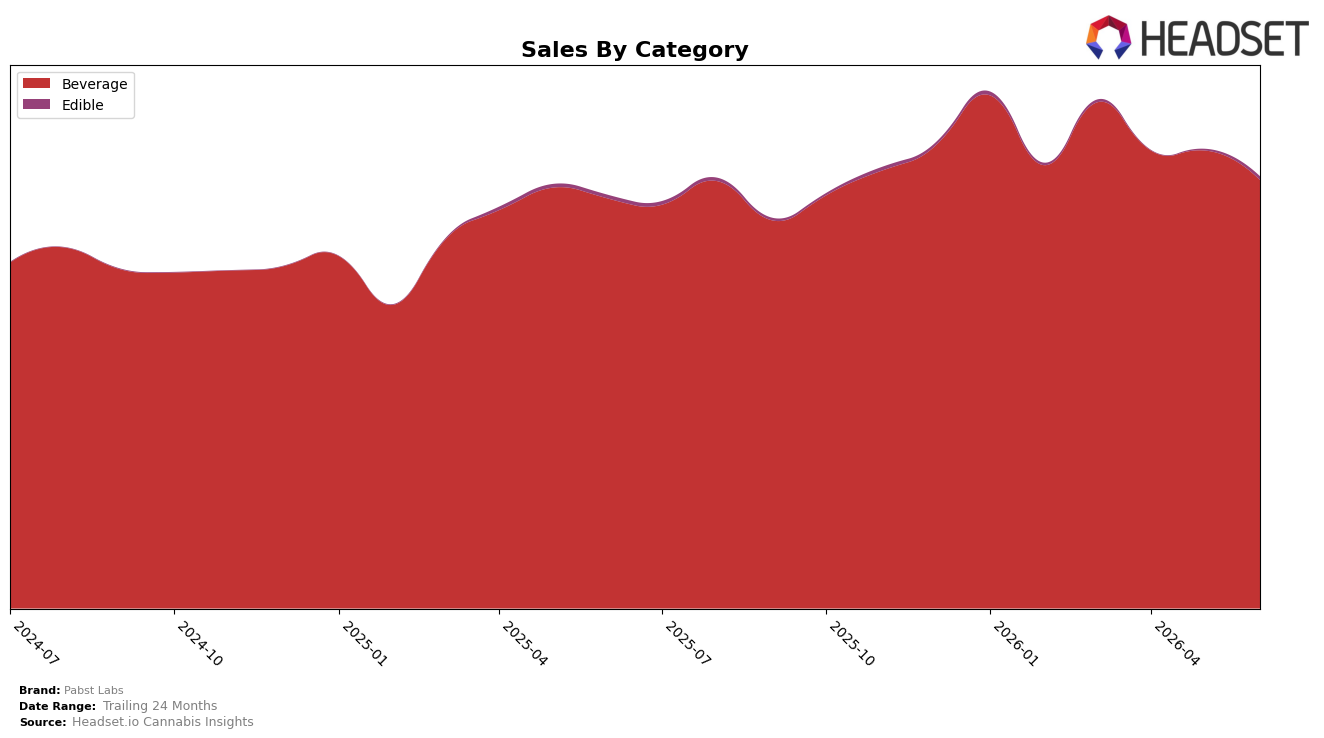

Pabst Labs concentrated 99.20% of June 2026 sales in Beverage while Edible held 0.80%, with Beverage down 6.46% month over month but up 4.52% year over year, and Edible up 155.69% month over month with a 4.52% year-over-year lift. Average price fell 14.34% year over year to $6.58 while Beverage priced at $6.54 versus Edible at $17.43, indicating mix pressure even as total brand sales grew 4.52% year over year; the thesis is that volume is tilting toward lower-priced Beverage even as a tiny Edible base expands rapidly month over month, keeping category concentration high but creating a small optionality wedge.

Within California Beverage, Pabst Labs ranked 6th in June 2026, and the 6-position standing alongside a 6.46% month-over-month Beverage decline implies share stability depends on defending core Beverage turns while nurturing Edible’s 155.69% month-over-month surge without diluting focus. The 19.91% 24-month sales gain against a 14.34% price decline suggests the brand’s positioning leans volume-led in Beverage, and the thesis is that maintaining a top-10 rank at 6 while expanding the 0.80% Edible mix incrementally can hedge against category price compression without eroding Beverage leadership.

Competitive Landscape

Pabst Labs sits at rank #6 in CA Beverage for June 2026, down 2 positions year over year from #4, and 1 position lower than March 2026 when it was #5; the brand’s peak of #4 in February 2026 contrasts with today’s placement, indicating a two-rank slide from peak to current. Meanwhile, St Ides held #1 year over year and remains #1 now as its sales grew 16.5% YoY, and CANN Social Tonics advanced from #7 YoY to #5 with 73.6% YoY sales growth, overtaking Pabst Labs as Pabst moved from #4 to #6; Almora Farms climbed from #6 YoY to #4 while Uncle Arnie's stayed at #2 as Pabst Labs fell 1 spot since March 2026. The pattern implies that unless Pabst Labs reverses a two-position YoY rank decline and a one-position quarter-over-quarter slip, faster-rising rivals will continue to compress its share of top-5 visibility.

Notable Products

Watermelon Melon Soda Pop 4-Pack (25mg THC, 12oz) posted the steepest decline at -45.6% month over month while holding rank 7, whereas Cherry Limeade Soda Pop (25mg THC, 12oz, 355ml) climbed 41.6% to rank 2; this split between sharp multi-pack erosion and single-can acceleration signals a shift in shopper preference toward single-serve trial. High Seltzer - THC/THCV 2:1 Daytime Energy Guava Seltzer (10mg THC, 5mg THCV, 12oz) rose 40.0% and maintained rank 1, while Lemon High Seltzer (10mg THC, 12oz) gained 9.1% at rank 3; four of the top ten are 4-packs, yet two of those 4-packs fell between -29.0% and -45.6%, indicating pack-size pressure despite broad shelf presence. Cherry Limeade Soda 4-Pack (100mg, 12oz, 355ml) countered the 4-pack softness with a 28.7% lift at rank 8 and $33,106 in June 2026 sales, but Strawberry Kiwi Seltzer 4-Pack (40mg) dropped -29.0% at rank 9; the pattern implies Pabst Labs is consolidating momentum in high-velocity single cans and a select few 4-packs tied to flavors with clear identity cues, guiding assortment toward fewer multi-pack SKUs with stronger pull.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.