Where to Buy

LivWell is stocked at 93 licensed dispensaries across New York, Maryland, and 2 other states, 59 of them in New York, with the deepest coverage in New York, Queens, Buffalo, Depew, and East Syracuse. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

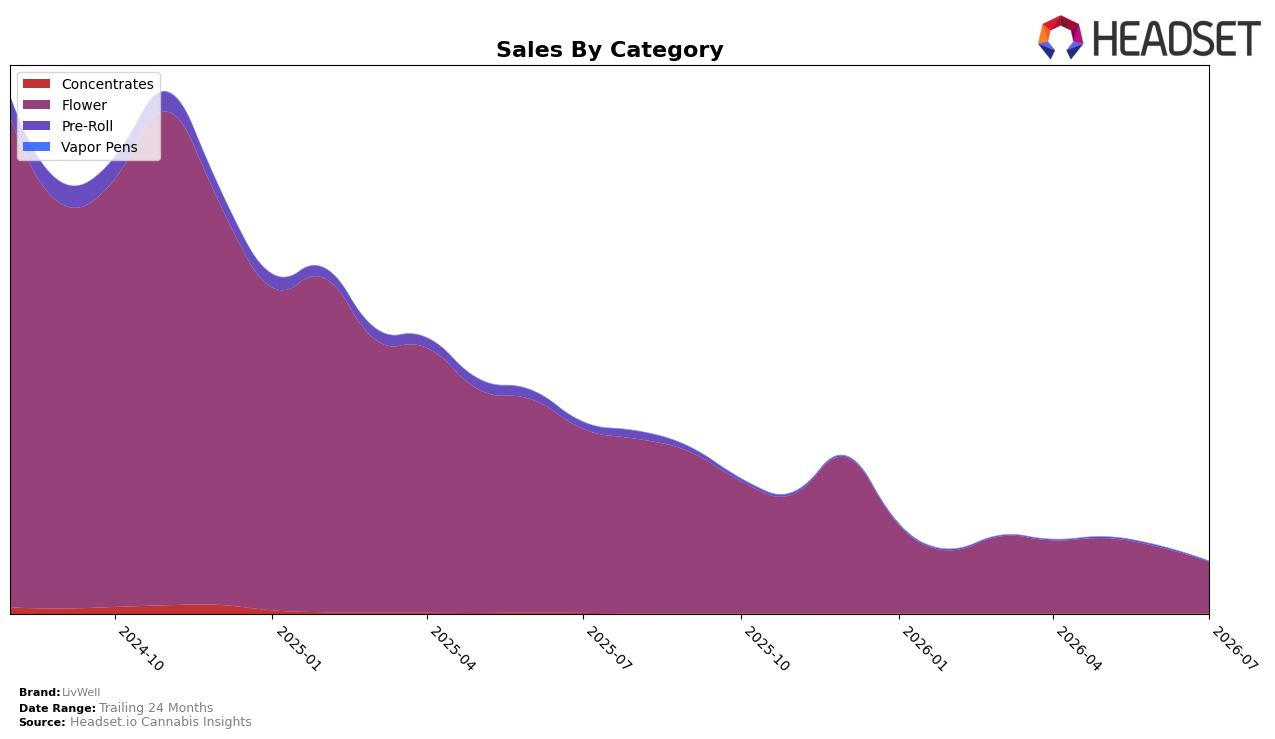

LivWell’s July 2026 mix is almost entirely Flower at 99.57% share, with Flower sales down 72.11% year over year and 22.74% month over month, while Pre-Roll sits at 0.34% share after a 97.33% YoY and 81.26% MoM drop. Concentrates remains tiny at 0.09% share, but its MoM change of 184.49% contrasts with a 92.51% YoY decline, and average price across the brand rose 12.93% YoY to $76.22. With Flower ranked 32 in New York and the brand’s overall sales down 73.04% YoY, the data indicate a narrowing presence where dependence on a single category and rising prices are coinciding with share and rank pressure.

The tilt toward Flower at 99.57% alongside a 22.74% MoM contraction implies exposure to category-specific volatility, while the 184.49% MoM rebound in Concentrates from a 0.09% base suggests a potential test bed rather than a material hedge. The 12.93% YoY price increase against a 73.04% YoY brand sales decline indicates price elasticity is biting more than mix is buffering, and the 97.33% YoY collapse in Pre-Roll further reduces cross-category capture. Taken together with a Flower rank of 32 in New York, the pattern implies LivWell’s current positioning is drifting toward a price-sensitive, single-category niche where small, fast-moving subcategory pilots matter for stability more than broad-based scale.

Competitive Landscape

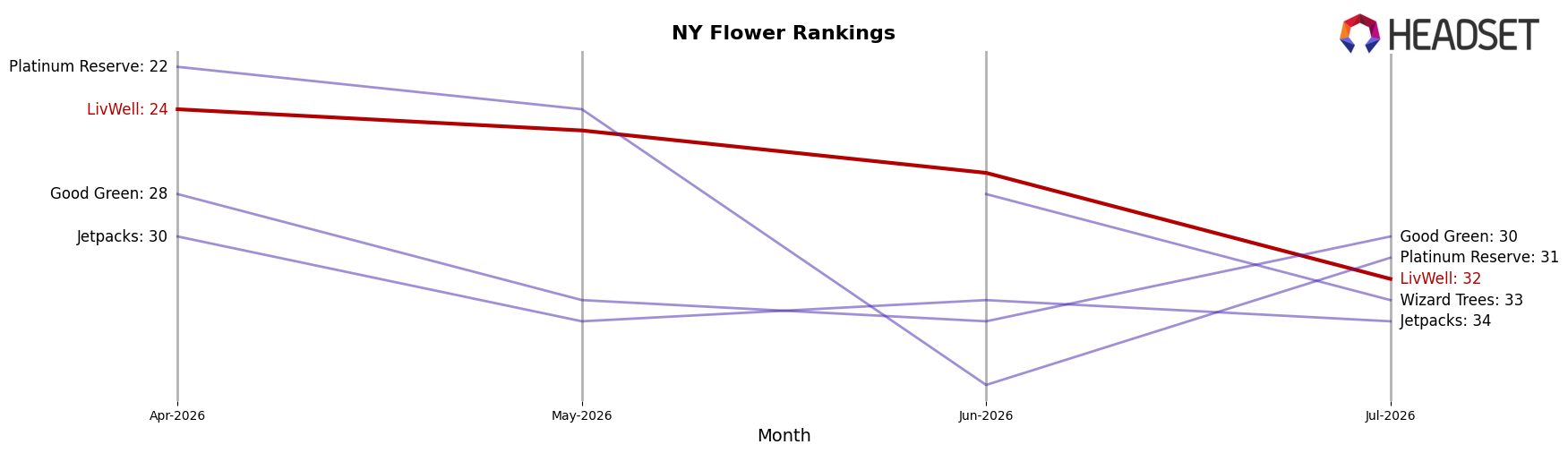

LivWell sits at rank #32 in New York Flower in July 2026, sliding 22 positions from its #10 spot in July 2025, and down 8 places from #24 in April 2026; the drop contrasts with its earlier peak at #2 in February 2025 and indicates a multi-quarter retreat in share of voice. Meanwhile, Find. advanced from #8 to #1 year over year while posting a 46.7% sales increase, and Grassroots climbed 15 ranks to #5 with 79.8% sales growth, whereas Dank. By Definition rose just 1 rank to #3 despite a 51.5% sales decline—evidence that rank mobility is driven by relative momentum rather than absolute volume. The pattern suggests LivWell’s rank trajectory—down 22 ranks YoY and 8 ranks since April 2026—signals erosion in competitive momentum that will persist unless assortment or price architecture counters the outsized gains from faster-moving rivals.

Notable Products

Strawberry Cookies (28g) posted the steepest move in July 2026 with a -42.8% month-over-month drop while falling to rank 4, and Apple Fritter (28g) also contracted by -28.9% yet held rank 1, indicating top-heavy demand pressure at the very front of the lineup. Mendo Breath (28g) was a counterweight with a +25.5% month-over-month rise at rank 2, narrowing the gap to the leader as Apple Fritter (28g) retreated, with Apple Fritter (28g) booking $59,961 in July 2026 sales. Four of the top ten are Berry-family SKUs, concentrating share inside a single flavor profile even as Strawberry Cookies (28g) underperformed and Burnout Cookies (28g) sat at rank 9 without a reported month-over-month change. The pattern points to a mix reset where dependence on cookie-themed names risks volatility while Berry variants provide breadth, implying LivWell should lean into the stable mid-pack while insulating the flagship tier from sharp month-over-month swings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.