Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Nanticoke is stocked at 288 licensed dispensaries across New York, with the deepest coverage in New York, Buffalo, Rochester, Syracuse, and Queens. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

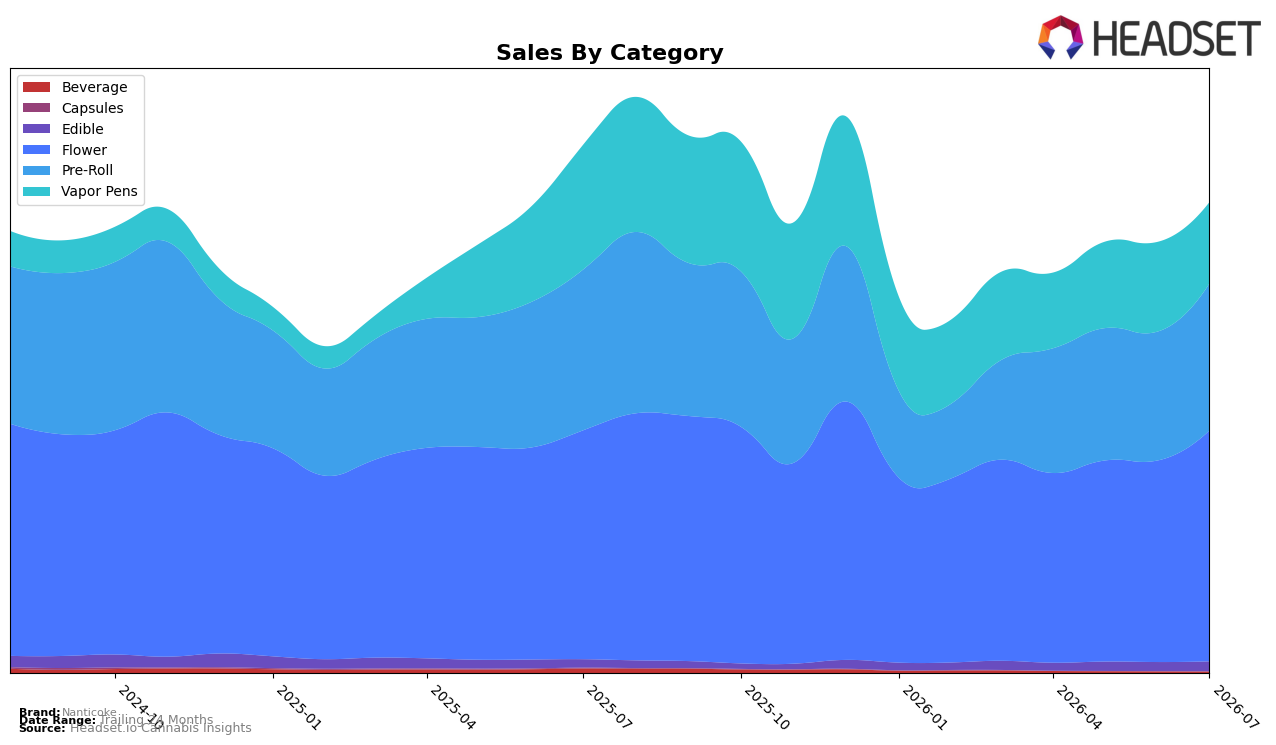

Nanticoke’s mix in July 2026 leans on Flower at 49.09% share with year-over-year growth of 0.86% and month-over-month growth of 14.50%, while Pre-Roll holds 31.25% share with a -8.55% year-over-year change but a 14.06% month-over-month lift. Vapor Pens account for 17.26% share with a -34.91% year-over-year decline and a -9.34% month-over-month drop, whereas Edible sits at 2.06% share with 17.99% year-over-year growth and 9.24% month-over-month growth. Beverage is 0.33% share with -66.09% year-over-year and -7.80% month-over-month. With Flower ranked 12 in New York for the category, the simultaneous month-over-month climbs in Flower and Pre-Roll alongside the retreat in Vapor Pens imply the portfolio is consolidating around inhalables with higher velocity while trimming exposure to slower-moving formats.

Despite total brand sales declining -10.89% year over year in July 2026 and average price inching up 0.30%, the category shifts point toward defending core inhalable share through Flower’s double-digit month-over-month expansion and Pre-Roll’s parallel 14.06% lift, while managing down a Vapor Pens decline of -34.91% year over year. Edible’s 17.99% year-over-year growth and 9.24% month-over-month increase offer a small diversification counterweight at 2.06% share, whereas Beverage’s -66.09% year-over-year contraction at 0.33% share reduces drag. The pattern implies Nanticoke’s positioning is tilting to a two-pillar inhalables strategy anchored by Flower’s rank of 12 in New York and supported by Pre-Roll, with selective expansion in Edible to mitigate volatility from Vapor Pens.

Competitive Landscape

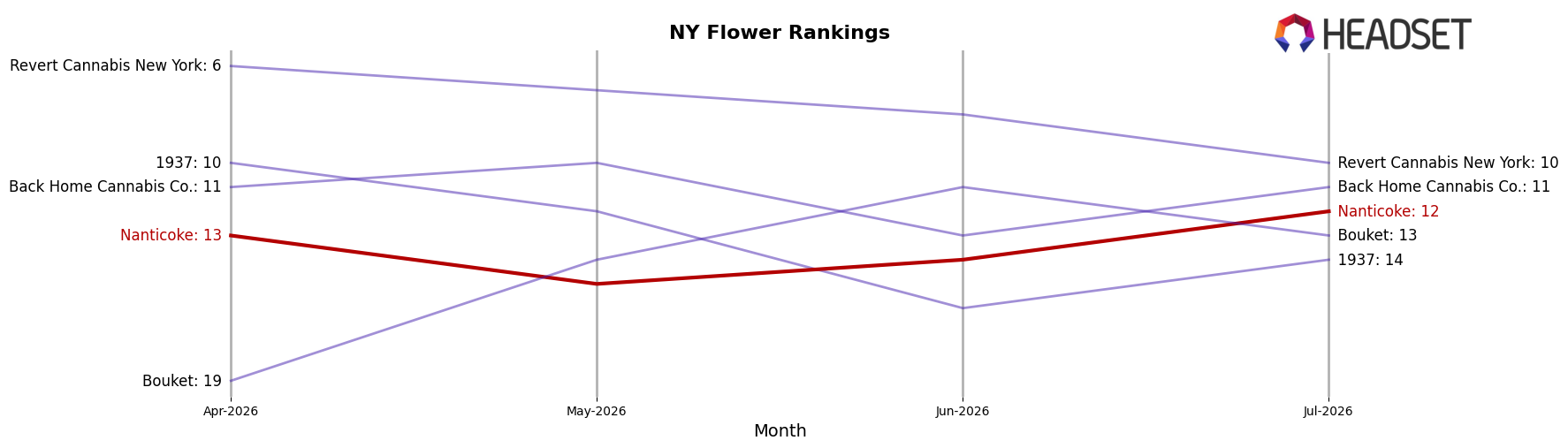

Nanticoke sits at rank #12 in July 2026 with a 0-position year-over-year change from July 2025, while its three-month trend improved 1 place from #13 to #12; against this stability, Find. climbed from #8 to #1 (a +7 rank gain) and Grassroots advanced from #15 to #5 (a +10 rank gain), indicating competitors are converting momentum into share as evidenced by 46.7% and 79.8% year-over-year sales growth respectively. Nanticoke’s historical ceiling at #5 in September 2024 contrasts with Dank. By Definition sliding from #1 to #3 alongside a 51.5% sales decline, and Leal moving from #7 to #2 (+5 ranks), collectively signaling a market where rapid ascents and declines are common; the flat year-over-year rank and small three-month uptick imply Nanticoke is holding ground but not compounding gains, so absent a catalyst its path points to share preservation rather than a return toward the prior #5 peak.

Notable Products

Durban Poison Pre-Roll (0.5g) posted the standout move in July 2026 with a 105.97% month-over-month gain, vaulting into rank 5 while All Gas Pre-Roll (0.5g) slipped 12.08% and Blue Dream Pre-Roll (0.5g) declined 8.65% at rank 4. Sour Diesel Pre-Roll (0.5g) rose 13.23% to hold rank 1, and Lemon Cherry Gelato Pre-Roll (0.5g) advanced 20.73% at rank 3, while Coconut Cream Pre-Roll (0.5g) added 4.59% at rank 2; eight of the top ten are Pre-Roll SKUs, concentrating volume in one format. This pattern implies Nanticoke is leaning into Pre-Rolls as the commercial engine, while a single outsized mover is reshaping mix risk and replenishment priorities.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.