Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

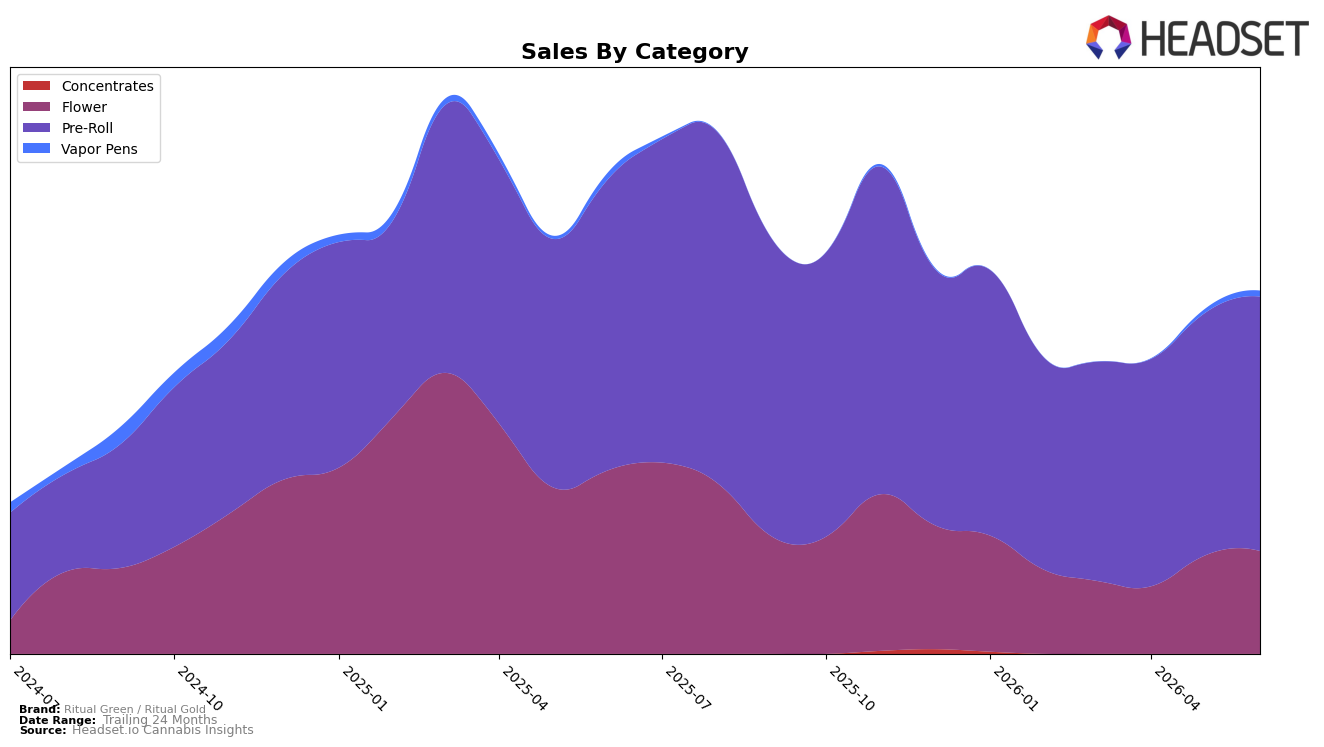

In June 2026, Ritual Green / Ritual Gold concentrated 70.14% of sales in Pre-Roll, up 4.97% month over month but down 12.66% year over year, while Flower held 28.30% share with a 4.73% month-over-month uptick against a 44.06% year-over-year decline; Vapor Pens remained 1.57% of mix with a 48.44% month-over-month rise and a 12.92% year-over-year drop. Despite a 7.74% year-over-year decrease in average price to $21.24, category elasticity diverged: Pre-Roll’s lower average price of 17.22 coincided with share stability, whereas Flower’s higher 49.24 price aligned with deeper year-over-year contraction, implying the portfolio is tilting toward lower-ticket formats as a defensive response to a 24.64% brand sales decline year over year.

These shifts point to a deliberate emphasis on velocity over ticket size: maintaining a number 7 rank in Pre-Roll within Saskatchewan alongside a 4.97% month-over-month gain suggests prioritization of a scalable lead category, while Flower’s 44.06% year-over-year drop and only 4.73% monthly lift indicate reduced competitive pull in premium-priced segments. The 48.44% month-over-month surge in Vapor Pens at just 1.57% share signals a low-risk test for incremental reach rather than a mix overhaul, implying the brand’s near-term positioning hinges on defending Pre-Roll share and selectively probing adjacent demand while de-emphasizing high-price Flower exposure.

Competitive Landscape

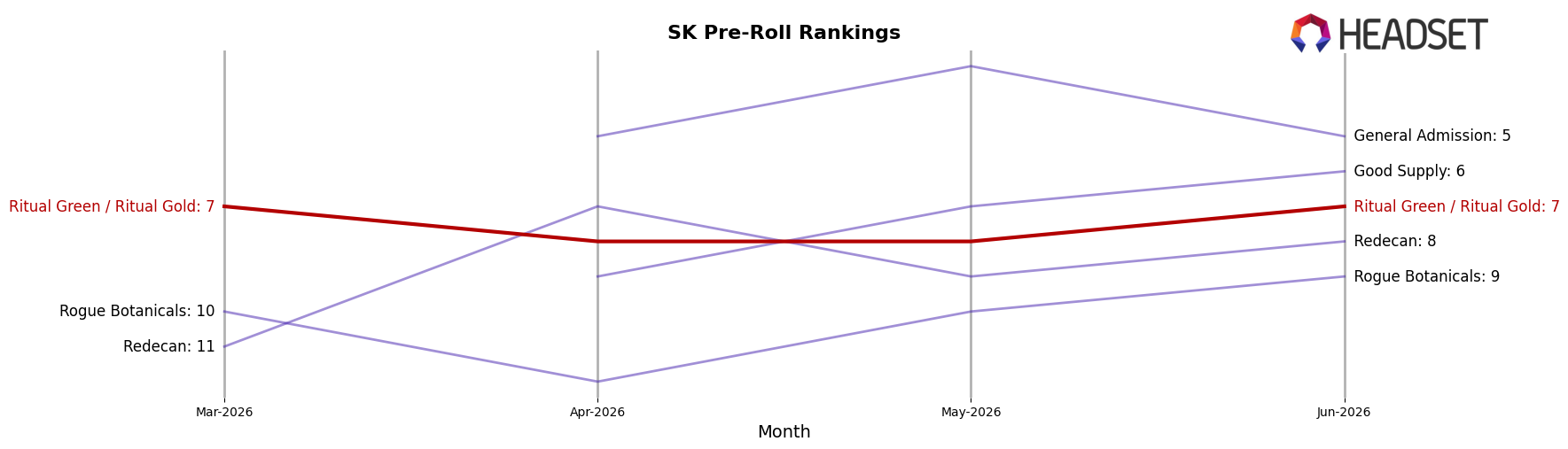

Ritual Green / Ritual Gold sits at rank #7 in SK Pre-Roll for June 2026, down 1 position year over year from #6, and flat versus March 2026 at #7, while its historical peak was #5 in August 2025; in contrast, Back Forty / Back 40 Cannabis holds #1 with 0 rank change and 134.2% YoY sales growth, and Doobie Snacks climbed from #9 to #3 with 282.0% YoY growth, indicating that mid-tier share is consolidating upward as rivals convert growth into rank gains while Ritual Green / Ritual Gold stagnates around the #7 band.

Notable Products

Ritual Sticks - Strawberry Rizz Pre-Roll 3-Pack (1.5g) posted the steepest decline at -33.1% and slid to rank 5, while Ritual Sticks - Black Mamba Pre-Roll 3-Pack (1.5g) gained +48.0% to reach rank 4; this divergence signals a reordering of consumer preference within the flavored pre-roll set. French Cookies Pre-Roll 3-Pack (1.5g) held rank 1 despite a -5.5% dip, and the French Cookies Pre-Roll 12-Pack (6g) climbed +34.9% at rank 7 with $31,902 in June 2026 sales, indicating trade-up alongside sustained single-pack leadership; eight of the top ten are Pre-Roll SKUs, concentrating demand in one format. The pattern implies the portfolio is consolidating around pre-roll multipacks and a few hero strains, guiding near-term mix toward scalable pack sizes and fewer flavor variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.