Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

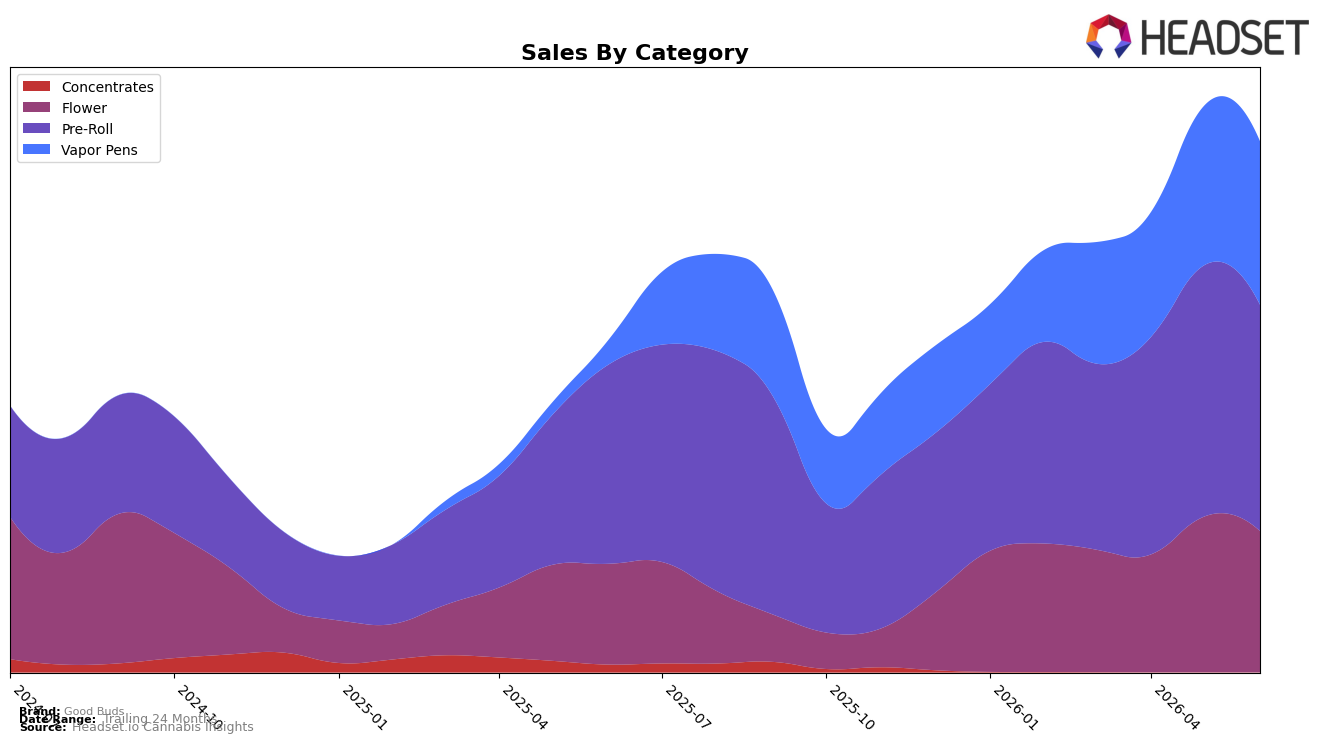

In June 2026, Good Buds concentrated 42.61% share in Pre-Roll with a 13.73% YoY lift but a -10.00% MoM dip, while Vapor Pens expanded to 30.80% share on a 570.07% YoY surge and a 2.34% MoM increase; Flower held 26.59% share with 40.31% YoY growth and a -9.36% MoM decline. Average price rose 17.24% YoY to $23.33 even as Pre-Roll pricing sat lower at $15.60 and Vapor Pens averaged $37.83, and Pre-Roll ranked 28th in British Columbia within its category. The combination of triple-digit Vapor Pens expansion and concurrent MoM pullbacks in Pre-Roll and Flower implies the mix is rotating toward higher-priced inhalables, with category momentum increasingly dependent on maintaining pen velocity rather than Pre-Roll rank stability alone.

With overall brand sales up 60.03% YoY alongside a 570.07% YoY jump in Vapor Pens and a 13.73% YoY gain in Pre-Roll, Good Buds is shifting from a Pre-Roll-led profile toward a two-pillar inhalables stance where pens carry incremental growth. The -10.00% MoM in Pre-Roll and -9.36% MoM in Flower, offset by a 2.34% MoM rise in Vapor Pens and a 17.24% YoY price increase, indicates pricing power is being reinforced by premium-leaning categories, positioning Good Buds to trade consumers up while accepting some volume volatility in Flower and Pre-Roll.

Competitive Landscape

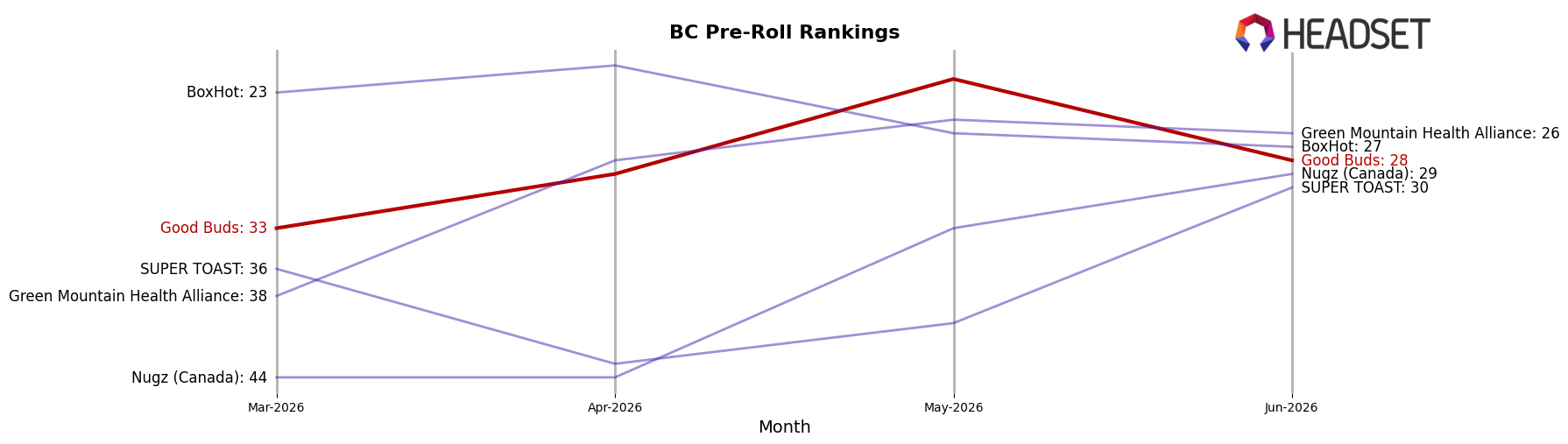

Good Buds sits at rank #28 in BC Pre-Roll in June 2026, improving 2 positions from #30 year over year and up 5 spots from #33 three months ago, while peaking at #22 in May 2026; meanwhile, General Admission held #1 year over year but its sales fell 18.9%, and Back Forty / Back 40 Cannabis surged from #22 to #3 on 263.3% YoY sales growth, indicating that Good Buds’ gradual rank gains are occurring amid volatile top-tier shifts and imply a pathway to mid-20s share if it sustains quarterly momentum.

Notable Products

The steepest decline came from Timewarp Pre-Roll (1g), which fell 49.3% month over month to rank 1, while BC Organic - Gluerangutan Pre-Roll (1g) dropped 43.7% at rank 4, signaling sharp pullbacks in single-pack pre-rolls. In contrast, Mango Cake Live Resin Cartridge (1g) rose 6.2% at rank 10 and Mango Cake Cured Resin Disposable (1g) grew 3.7% at rank 6, as Mango Cake Pre-Roll 7-Pack (3.5g) inched up 3.1% at rank 3. With six of the top ten positioned in Pre-Roll and multiple single-pack SKUs declining more than 20% while multi-pack and vapor SKUs are flat-to-up, the mix implies a pivot away from single-stick value toward larger pack counts and inhalable derivatives for July 2026 planning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.