Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Heavy Hitters is stocked at 947 licensed dispensaries across California, New York, and New Jersey, 647 of them in California, with the deepest coverage in Los Angeles, Sacramento, San Francisco, San Diego, and San Jose. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

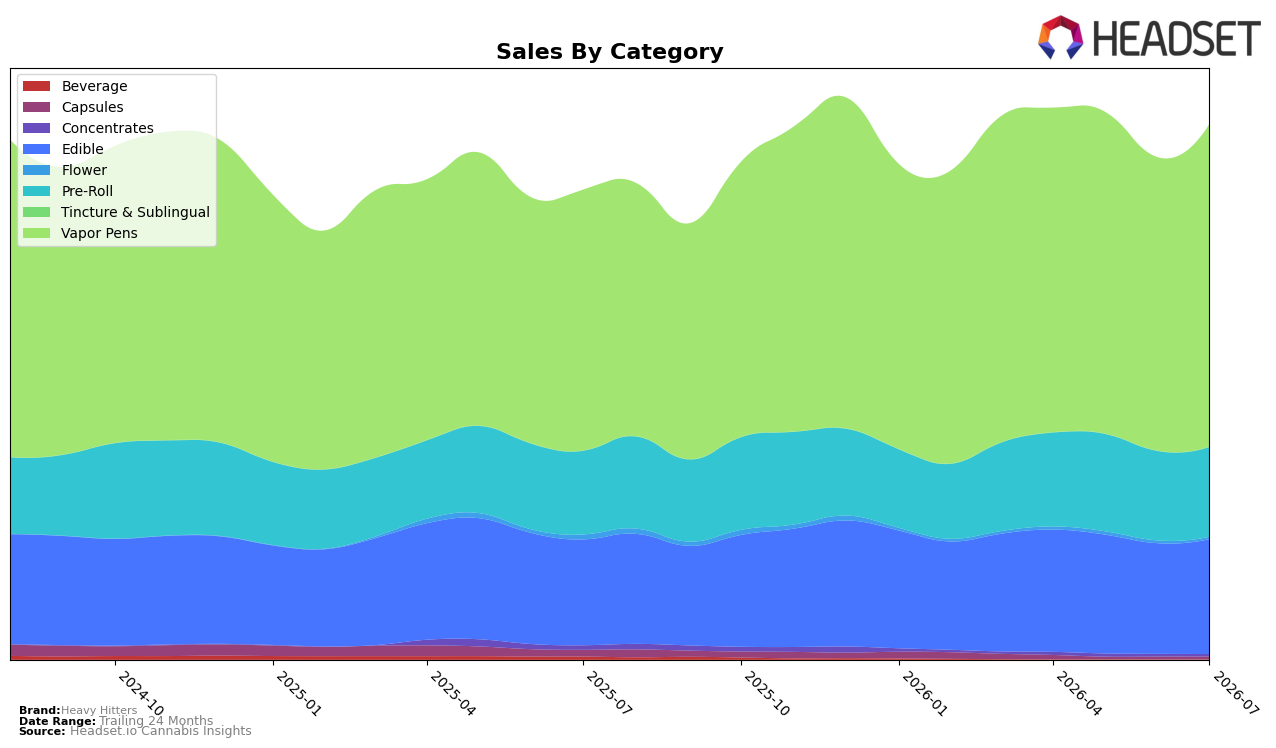

In July 2026, Heavy Hitters concentrated 60.45% of sales in Vapor Pens with year-over-year growth of 23.78% and month-over-month growth of 10.00%, while Edible held 21.48% share with 8.60% YoY and 3.88% MoM, and Pre-Roll accounted for 16.78% with 7.33% YoY and 0.45% MoM. Long-tail categories contracted sharply on a YoY basis—Beverage at -97.38% YoY and Concentrates at -48.92% YoY—despite mixed MoM signals such as Tincture & Sublingual at 101.88% MoM and Capsules at 5.76% MoM; Flower declined both YoY (-56.40%) and MoM (-17.70%). The pattern implies an intentional tilt toward inhalable formats where Vapor Pens rank 6th in California, using Edible and Pre-Roll as secondary pillars while de-emphasizing categories with steep YoY erosion.

With Vapor Pens expanding share and growth outpacing Edible and Pre-Roll on both a 23.78% YoY and 10.00% MoM basis, the brand’s positioning centers on premium-priced inhalables, reinforced by a $50.40 average price in Vapor Pens versus $17.31 in Edible and $27.98 in Pre-Roll. The simultaneous collapse in Beverage (-97.38% YoY) and sizable YoY pullbacks in Flower (-56.40%) and Concentrates (-48.92%) signal resource reallocation away from lower-yield or fragmented niches, even as selective bets like Tincture & Sublingual’s 101.88% MoM spike test micro-opportunities. This mix suggests Heavy Hitters is optimizing for depth where it already holds rank 6 in California Vapor Pens while maintaining breadth through Edible at 21.48% share and Pre-Roll at 16.78% share to buffer volatility across inhalable-led demand cycles.

Competitive Landscape

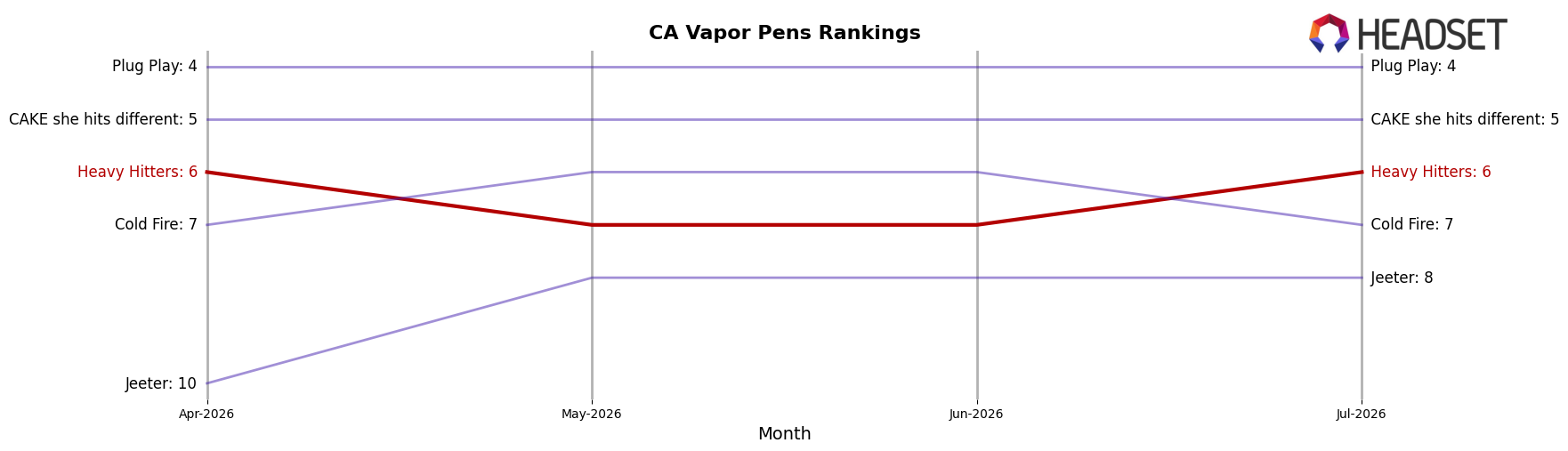

Heavy Hitters sits at rank #6 in California Vapor Pens in July 2026, a 1-place rise from #7 year over year and flat versus April 2026 at #6, while still trailing its peak at #5 from September 2024; meanwhile, Jetty Extracts climbed from #4 to #3 with a 41.7% YoY sales increase and Plug Play slipped from #3 to #4 on an 8.5% YoY decline, indicating that Heavy Hitters’ incremental rank gain amid mixed competitor trajectories implies a stable mid-tier position that will require displacement of #5 to reopen an upward path.

Notable Products

Light On - THC/THC-V 2:1 Green Crack Gummies 5-Pack (100mg THC, 50mg THCV) posted the standout move in July 2026 with +103.6% month over month to rank 2, while Lights Out - THC/CBN 1:1 Midnight Cherry Gummies 5-Pack (100mg THC, 100mg CBN) slipped 7.97% but still held rank 1. Blue Dream Distillate Cartridge (1g) climbed 21.3% to rank 3, and five of the top ten are Edible SKUs, signaling a tilt toward functional gummies over hardware. The edible tier added mid-teens gains from Atomic Apple x Big Apple Ultra Potent Gummies (+13.5%, rank 4) and Holy Grape x God's Gift Ulta Gummies (+13.1%, rank 7), while Sour Watermelon Fast Acting Diamond Infused Gummies grew 3.8% at rank 8 and the Pineapple Express Distillate Cartridge entered the list at rank 8 with $194,219. The pattern implies Heavy Hitters is consolidating leadership around specialty formulations that drive repeatable Edible velocity, using a few high-visibility Vapor Pens as traffic anchors rather than growth engines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.