Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Mari's is stocked at 144 licensed dispensaries across Washington, with the deepest coverage in Tacoma, Spokane, Seattle, Bellingham, and Olympia. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

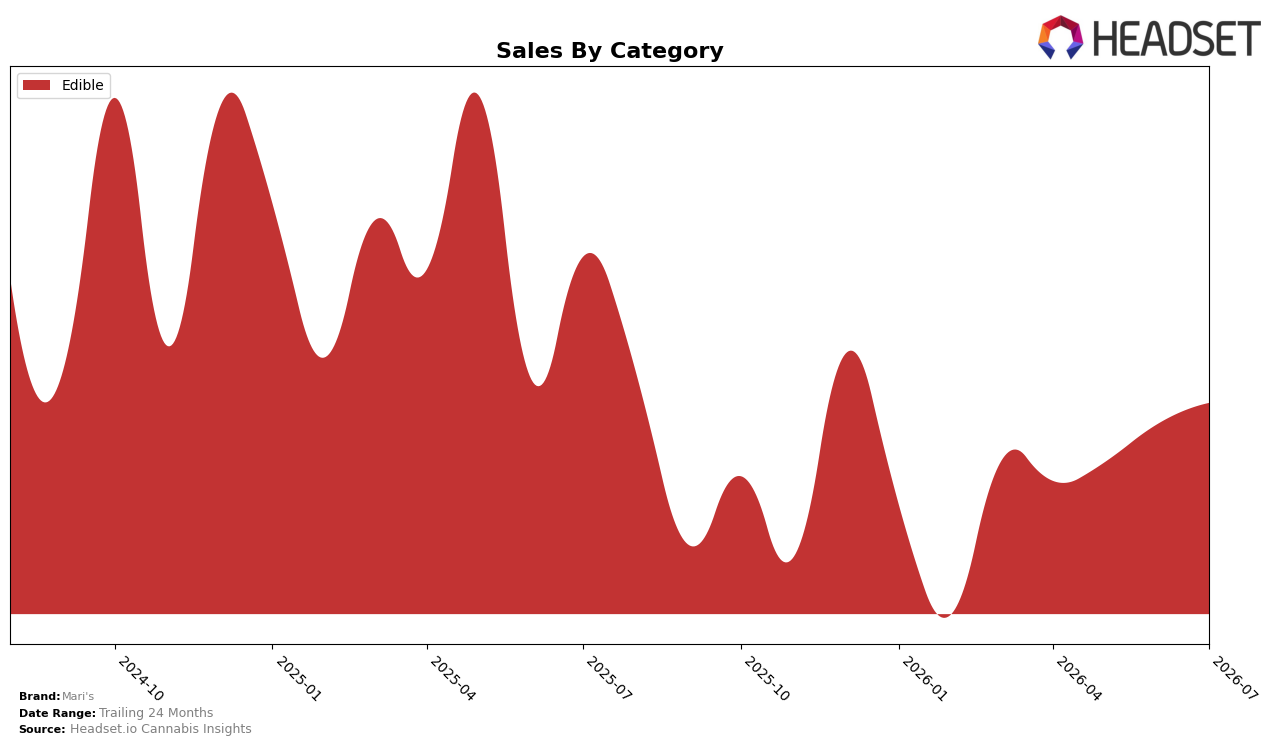

Edible held 100.0% of Mari's mix in July 2026, with category sales up 1.21% month over month but down 7.63% year over year, while average price slipped 0.87% YoY and effectively held flat MoM within rounding. The combination of a 1.21% MoM volume-led uptick against a 7.63% YoY decline indicates the brand is stabilizing sequentially within a single-category footprint, but still digesting a multi-quarter reset; given this concentration and the July 2026 MoM lift, the pattern implies short-term momentum is reliant on incremental Edible velocity rather than price expansion.

In Washington, Mari's ranked 19 in Edible for July 2026, and the 7.63% YoY sales contraction alongside a 0.87% YoY average price decrease suggests share pressure has been driven more by unit throughput than by pricing power. With Edible at 100.0% of sales and only a 1.21% MoM sales gain, maintaining rank 19 depends on recapturing unit share within Edible rather than cross-category diversification, implying that merchandising depth and SKU-level rotation in Washington will be more impactful than further price moves in the near term.

Competitive Landscape

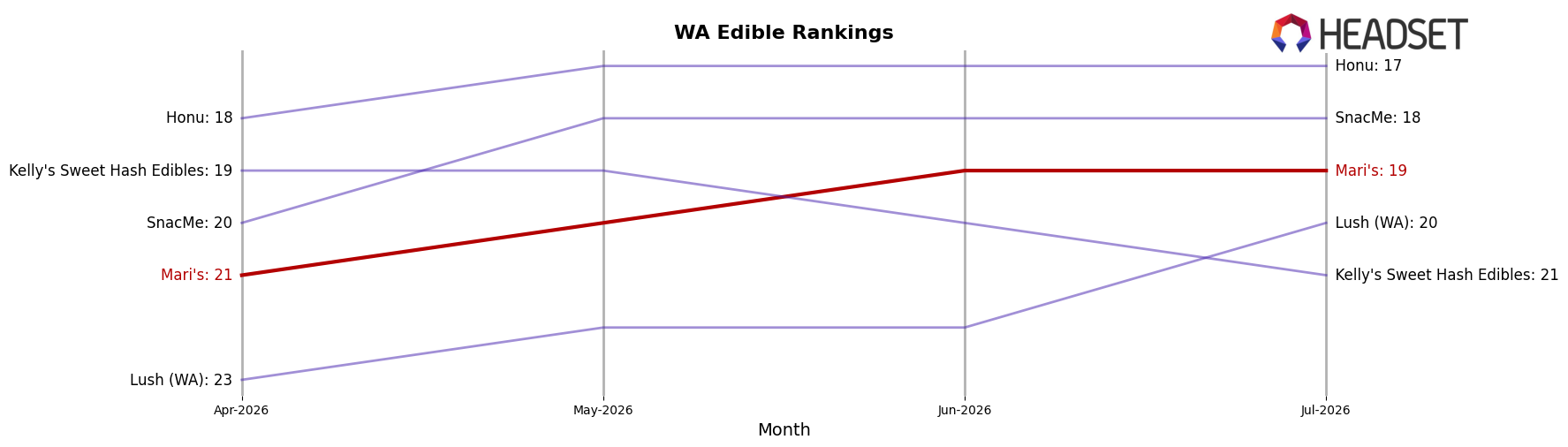

Mari's is ranked #19 in WA Edible in July 2026, with a 0-position year-over-year rank change and a 2-rank improvement versus April 2026 from #21 to #19; the brand’s peak at #16 in September 2024 sits 3 positions above current standing, while the flat year-over-year rank indicates neither category outperformance nor slippage relative to peers. Among competitors, Wyld held #1 year-over-year and remains #1 with 7.99% YoY sales growth, whereas Craft Elixirs moved down from #4 to #5 alongside an 8.01% YoY sales decline; in contrast, Journeyman climbed from #5 to #4 with 6.47% YoY growth. The mix of a 2-rank quarter-on-quarter lift and a 0-position year-over-year change implies Mari's is stabilizing off a late-2024 high but needs incremental share gains to reverse a two-year drift from the #16 peak.

Notable Products

The steepest movement in July 2026 was the Sativa Move Mints 10-Pack (100mg) dropping 15.20% to rank 10, while Indica Retire Mints 10-Pack (100mg) also contracted 12.38% at rank 7, indicating stress in smaller pack sizes as larger 20- and 40-packs gained ground. At the top, Sativa Peppermint Move Mints 20-Pack (100mg) held rank 1 despite a 4.90% dip, whereas Sativa Strawberry Move Mints 40-Pack (100mg) climbed 15.53% at rank 3, and the CBN/CBD/THC 1:1:1 Peppermint Pillow Mint 20-Pack (100mg CBN, 100mg CBD, 100mg THC) surged 24.98% at rank 4. With all top-10 SKUs in Edible and four of the top ten clustered in Sativa Move Mints variants, the mix points to a tilt toward higher-count functional mints over legacy 10-packs, implying pack-size uptrade and cannabinoid-formulation breadth are setting the commercial direction.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.