Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Happy Cabbage Farms is stocked at 274 licensed dispensaries across Oregon and Washington, 243 of them in Oregon, with the deepest coverage in Portland, Salem, Eugene, Bend, and Medford. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

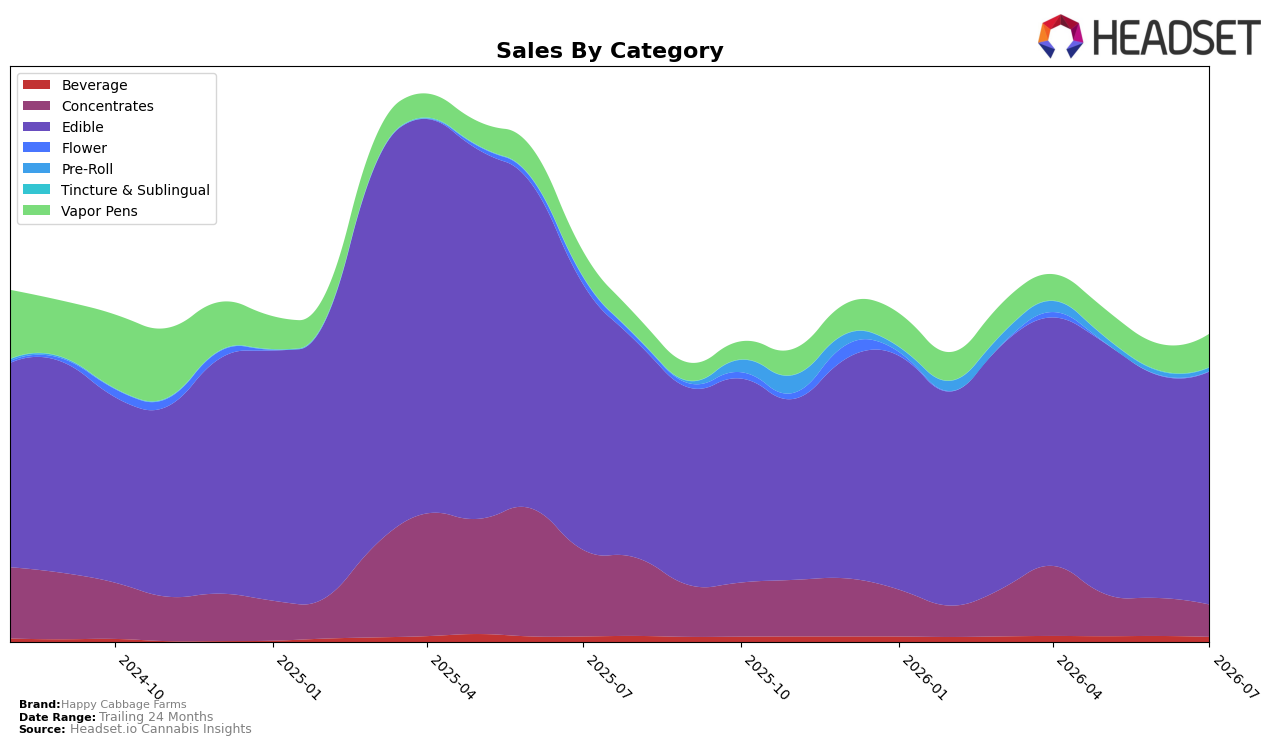

Happy Cabbage Farms concentrated 75.97% of July 2026 sales in Edible, where year-over-year sales fell 12.33% but month-over-month grew 4.55%, while Vapor Pens expanded to 10.81% share with a 33.42% YoY increase and a 26.07% MoM jump. Concentrates contracted to 10.44% share with a 62.94% YoY decline and a 15.06% MoM drop, and Beverage slipped to 1.71% share with a 6.77% YoY decline and a 14.20% MoM decrease; meanwhile, Pre-Roll held 1.08% share with a 10.28% MoM decline and no YoY baseline. With brand-wide sales down 21.20% YoY alongside a 25.41% YoY price decrease, the mix is pivoting toward lower-priced Edible and fast-rising Vapor Pens, implying a deliberate reweighting that offsets Concentrates attrition and stabilizes volume despite overall pressure.

Holding rank 8 in Edible in Oregon in July 2026 while Edible MoM rose 4.55% and Concentrates MoM fell 15.06% indicates that category leadership is anchored in Edible even as high-ticket Concentrates recede. The 33.42% YoY and 26.07% MoM gains in Vapor Pens, coupled with an average price of 37.68 versus 7.63 in Edible, suggest margin mix recovery potential if Vapor Pens scale above their current 10.81% share, while Beverage’s 14.20% MoM decline and Pre-Roll’s 10.28% MoM dip limit diversification. Net effect: sustaining Edible share while accelerating Vapor Pens can counter the 62.94% YoY collapse in Concentrates and reposition the brand toward a two-pillar portfolio that trades near-term price cuts for category breadth.

Competitive Landscape

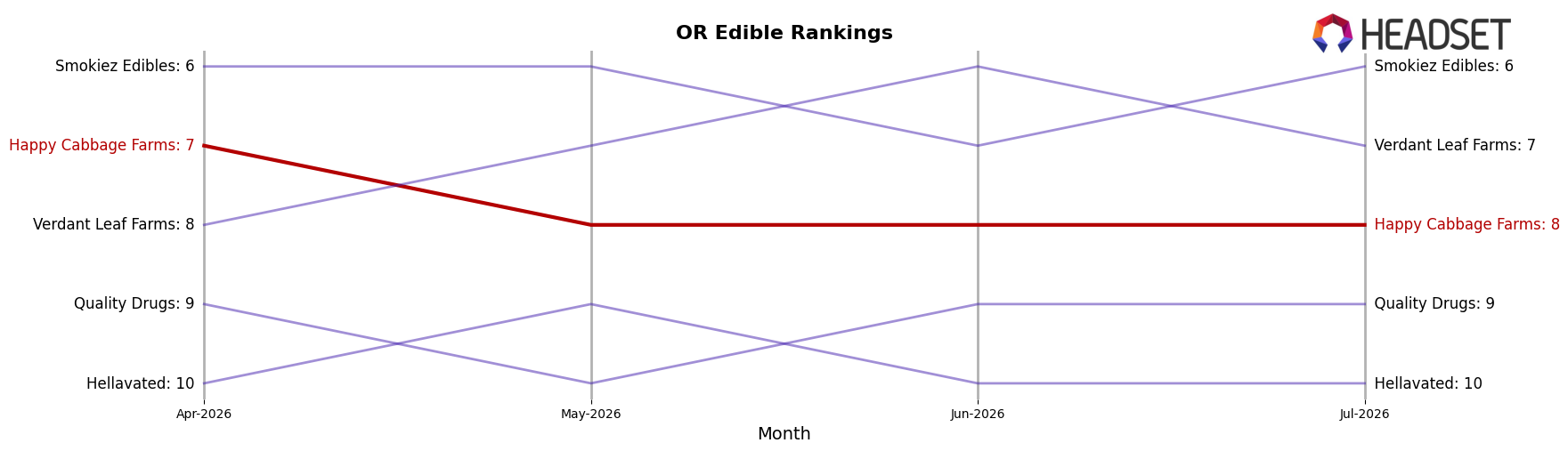

Happy Cabbage Farms sits at rank #8 in OR Edible for July 2026, slipping 1 position from #7 year over year, while holding flat versus April 2026 where it also peaked at #7; this -1 rank delta contrasts with Wyld holding #1 with a 2.5% YoY sales lift and Mule Extracts steady at #5 alongside a 7.5% YoY increase. Meanwhile, Gron / Grön remained #2 despite a -0.1% YoY sales change and Drops held #3 with a -5.3% YoY decline, indicating that lateral rank stability can coexist with both positive and negative sales trajectories; the pattern implies Happy Cabbage Farms’ slight rank erosion amid mixed competitor growth narrows its path to regain a top-7 position without a step-change in velocity.

Notable Products

Blox - CBD/THC 1:1 Strawberry Serenity Solventless Rosin Gummies 10-Pack (100mg CBD, 100mg THC) posted the steepest decline in July 2026 at -14.3% and slid to rank 6, while Pina Colada Solventless Hash Gummy (100mg) dropped -12.6% at rank 9; by contrast, Indica Marionberry Solventless Ice Hash Gummy (100mg) jumped +38.0% to rank 7 and Mango Solventless Hash Gummy (100mg) rose +16.0% at rank 8. The category remains concentrated in Edibles with the top 10 entirely within the format, and the leader Blox - Green Apple Solventless Hash Gummy (100mg) grew +13.4% at rank 1 as Blox - Cherry Limeade Solventless Rosin Gummy (100mg) advanced +14.9% at rank 2. This mix of mid-pack volatility alongside incremental gains at ranks 1–2 implies Happy Cabbage Farms is consolidating share in core fruit-forward SKUs while trimming reliance on wellness 1:1 variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.