Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

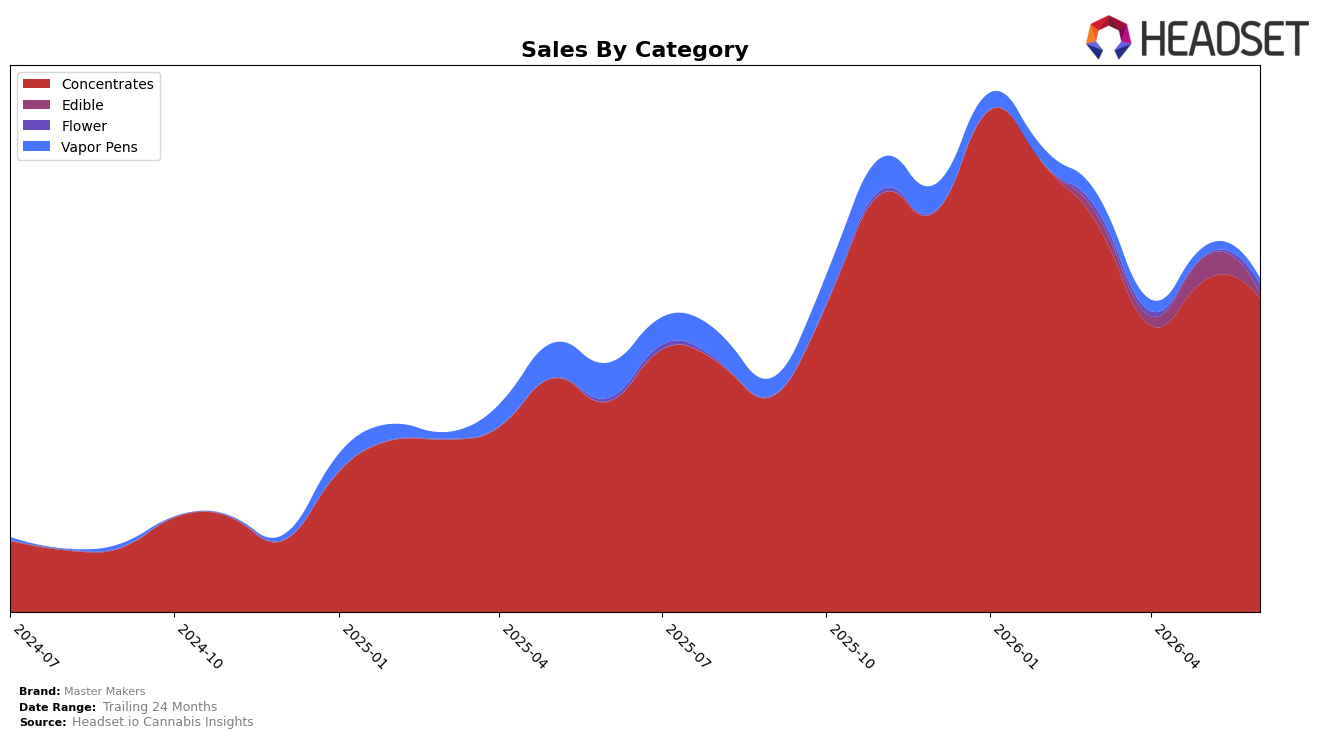

In June 2026, Master Makers concentrated 94.25% of sales in Concentrates, where sales grew 49.19% year over year but slipped 5.43% month over month, while average price across the brand fell 7.07% YoY. Flower expanded to a 2.55% share with a 186.48% YoY surge and an 840.17% MoM spike, whereas Vapor Pens contracted to 1.69% share with an 83.84% YoY decline and a 35.43% MoM drop; Edible held 1.51% share with a 78.44% MoM pullback. With Concentrates ranked 19 in California and the top-category focus intact, the pattern implies deliberate reinforcement of the core while testing secondary categories at small scale to offset category-specific volatility.

The mix shift implies Master Makers is using a core-and-probe posture: maintaining a Concentrates anchor to preserve ranking at 19 while deploying opportunistic pushes in Flower after an 840.17% MoM jump and sustaining price accessibility with a 7.07% YoY average price decrease. Given Vapor Pens’ 83.84% YoY contraction and Edible’s 78.44% MoM retreat, reallocating merchandising and promotional weight from underperforming formats toward Flower and high-velocity Concentrates could defend share in June 2026 conditions and position the brand to trade customers across adjacent inhalable formats rather than dilute efforts in low-elasticity segments.

Competitive Landscape

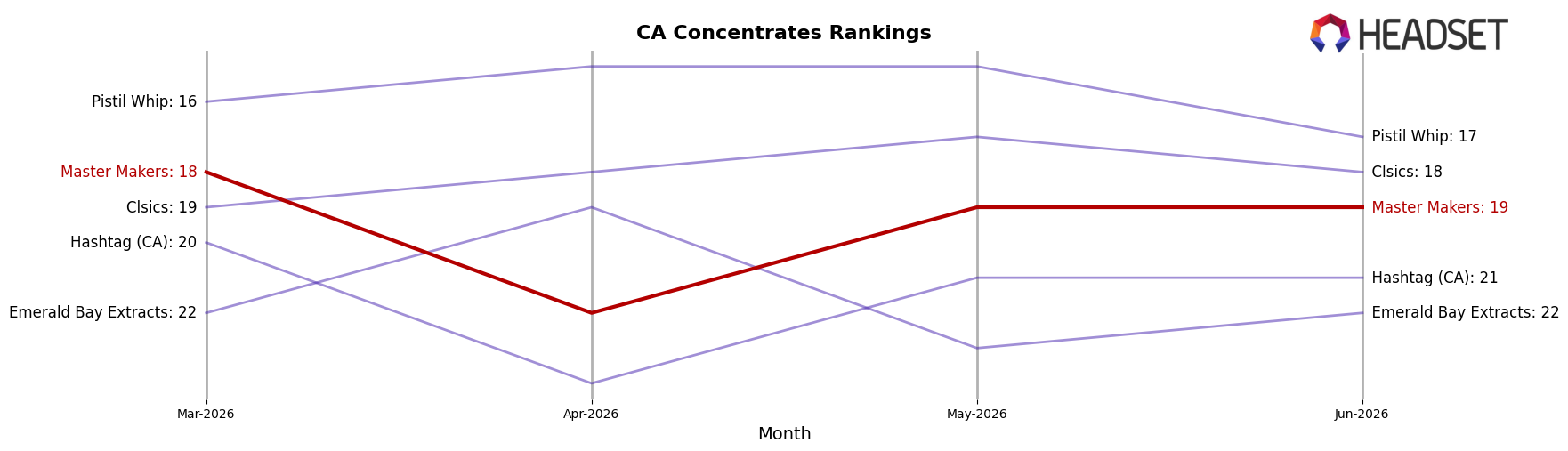

Master Makers sits at rank #19 in CA Concentrates in June 2026, improving 13 positions year over year from #32 while slipping 1 spot from March 2026’s #18; against that backdrop, Raw Garden held #1 both this year and last, and 710 Labs moved up from #4 to #3 with a 24.7% YoY sales lift, outpacing Master Makers’ climb in relative momentum. The brand’s peak at #14 in January 2026 followed by a retreat to #19 in June 2026 indicates rank volatility, while the top two positions remaining fixed at #1 and #2 for Raw Garden and STIIIZY constrains upward mobility; this trajectory implies Master Makers’ gains are coming from mid-tier reshuffling rather than breakthroughs into the top-10.

Notable Products

Wedding Cake Full Spectrum Live Rosin (1g) posted the standout movement in June 2026 with a +57.1% month-over-month climb to rank 2, while Hash Burger Cold Cure Live Rosin (1g) slid -22.5% at a shared rank 7, marking the steepest decline among the top SKUs. Whitethorn Rose Cold Cure Live Rosin (1g) held rank 1 with +26.4% MoM, and Egyptian Gold Cold Cure Full Spectrum Live Rosin (1g) softened -2.4% at rank 5, indicating gains are concentrated at the very top while mid-tier volatility persists. With all ten top products in Concentrates and three SKUs clustered in ranks 1–3, the mix points to a tighter focus on live rosin formats where momentum is consolidating in fewer flagship items rather than broad-based lift.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.