May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

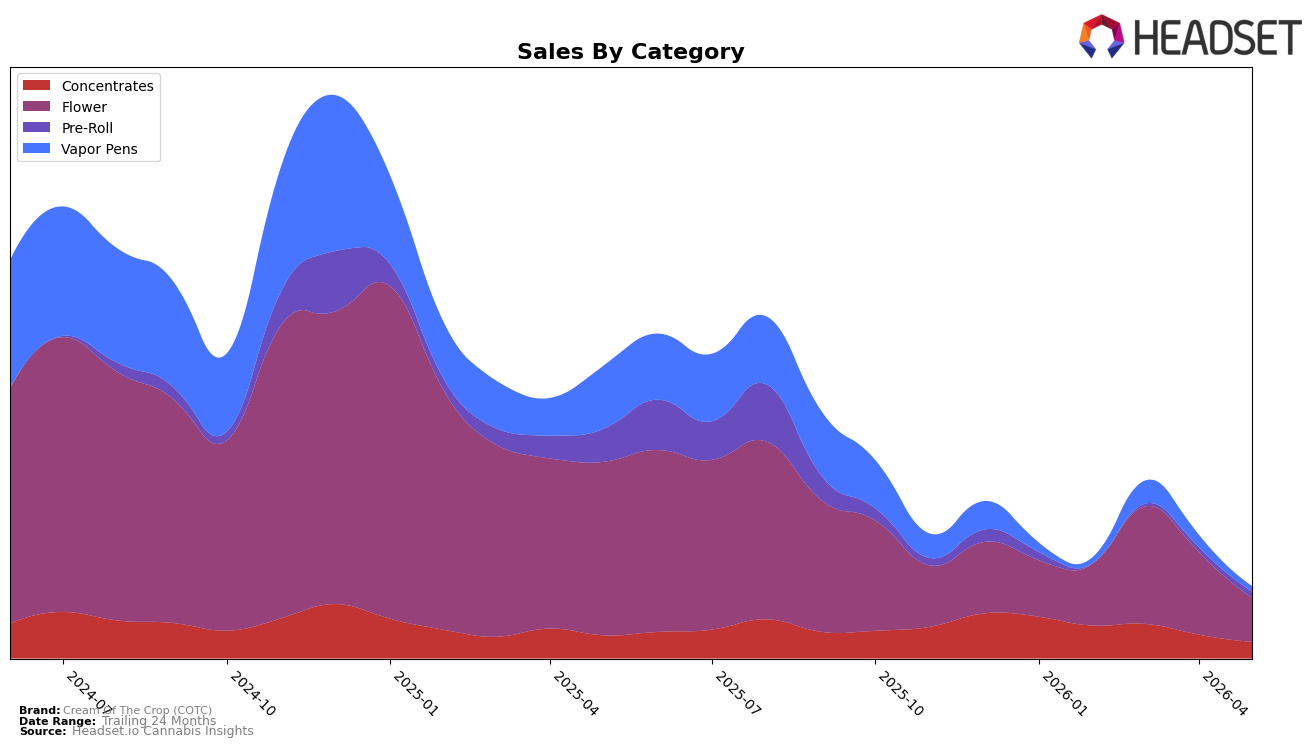

Cream Of The Crop (COTC) concentrated 47.01% of May 2026 sales in Flower, while Concentrates held 23.83% and Vapor Pens and Pre-Roll split 14.32% and 14.84%, respectively; within this mix, Flower fell 41.14% month over month and 70.02% year over year, and Vapor Pens declined 29.38% MoM and 77.36% YoY. Offsetting those drops, Pre-Roll expanded 8.52% MoM despite a 60.54% YoY contraction, and Concentrates contracted 20.36% MoM alongside an 18.77% YoY decline; the brand’s average price decreased 9.67% YoY, and Flower’s average price sat at $43.64. This pattern implies a pivot away from historically core segments toward a more balanced, lower-price-mix where Pre-Roll stabilizes share as Flower volatility accelerates.

Positioning in California Flower sits at rank 97, while brand-level sales declined 65.15% YoY and 74.92% over 24 months, indicating diminished visibility in the largest category as Pre-Roll gains short-term traction. With Vapor Pens down 29.38% MoM yet still 14.32% of mix and Concentrates down 20.36% MoM at 23.83% share, the near-term strategy skews toward defending presence in mid-priced formats (avg. prices of $21.87 for Pre-Roll and $20.85 for Concentrates) while de-emphasizing premium Flower at $43.64; this implies the brand’s defensible lane is value-leaning inhalables that can recapture velocity faster than top-shelf Flower.

Competitive Landscape

Cream Of The Crop (COTC) sits at rank #97 in CA Flower for May 2026, sliding 52 positions year over year from #45 and dropping 22 spots since February 2026 from #75, while its historical peak of #22 in January 2025 underscores the scale of retracement; in contrast, CAM climbed from #4 to #1 and STIIIZY rose from #2 to #2 with 39.7% YoY sales growth, signaling that COTC’s downward rank momentum is occurring as leaders consolidate share rather than during broad category softness, implying that without a corrective shift in velocity or distribution the brand’s trajectory points to continued share erosion against top-5 incumbents.

Notable Products

High Note (3.5g) posted the steepest movement in May 2026 with a -53.1% month-over-month decline while holding rank 5, and Nuclear Slurpee (3.5g) fell -45.5% at rank 4, indicating acute pressure within Flower even as Grape Kush (3.5g) stayed at rank 1 with a -32.3% slide. Three Flower SKUs occupy five of the top seven ranks, but each recorded double-digit declines ranging from -32.3% to -53.1%, suggesting volume is concentrating at the top while velocity erodes. In contrast, You're My Boy Blue Badder (1g) in Concentrates entered at rank 3 with $8,276 and Pink Sharpies Badder (1g) landed at rank 2 with an unreported prior base, while Donny Burger Badder (1g) slid -26.5% to rank 9, pointing to a mixed but comparatively steadier Concentrates profile than Flower. The pattern implies Cream Of The Crop (COTC) is pivoting from a Flower-led lineup toward a broader mix where Concentrates and new formats sustain rank positions despite Flower contraction.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.