Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

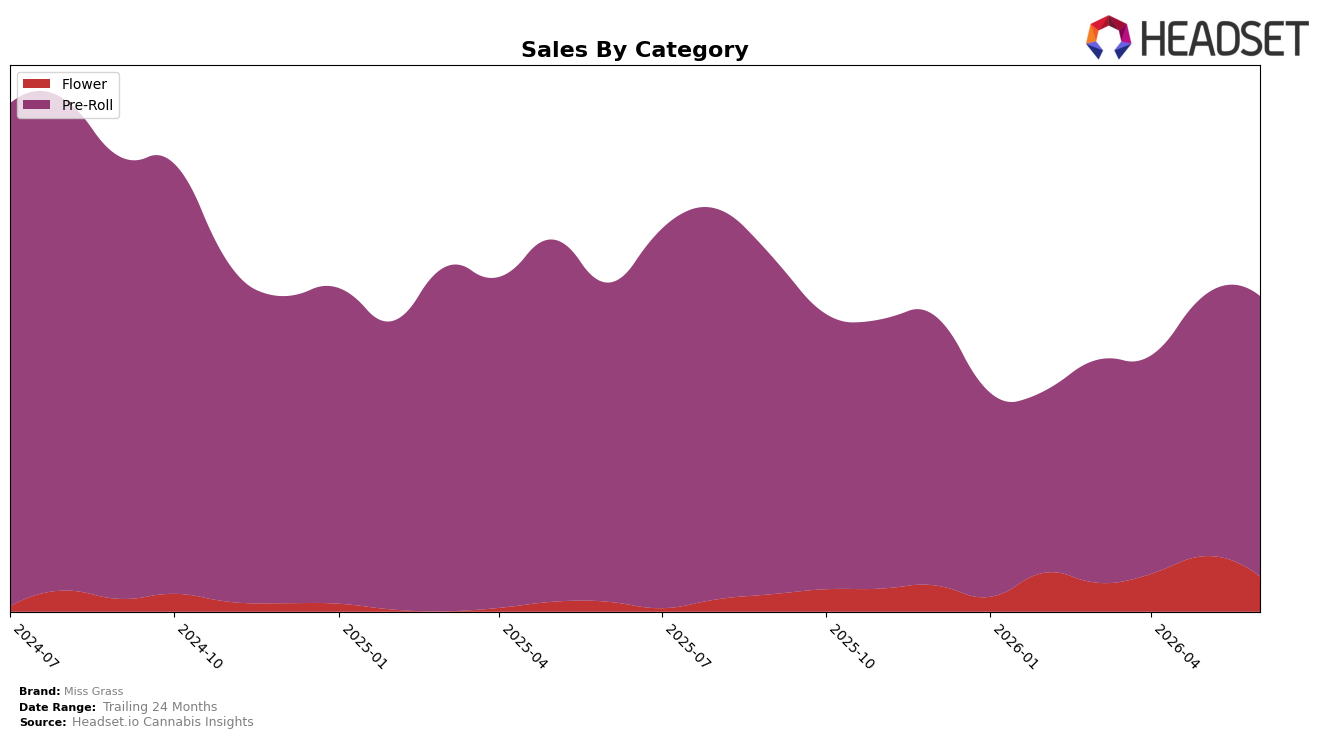

In June 2026, Miss Grass concentrated 87.85% of sales in Pre-Roll, while Flower accounted for 12.15%; Pre-Roll rose 7.38% month over month but fell 11.96% year over year, whereas Flower declined 34.07% month over month after a 179.32% year-over-year surge. The brand’s average price slipped 2.06% year over year to $25.58, with Pre-Roll priced at $24.21 and Flower at $43.43, and total brand sales contracted 3.97% year over year alongside a 24-month decline of 26.36%. The pattern implies a Pre-Roll-led model that is stabilizing month over month yet carrying year-over-year drag, while Flower’s smaller but volatile slice is driving mix risk rather than consistent expansion.

With Pre-Roll at 87.85% share and a category rank of 4 in Pre-Roll in Connecticut, June 2026 mix dynamics suggest reliance on one category for visibility even as the month-over-month Pre-Roll uptick outpaces the Flower retrenchment. The combination of a 7.38% Pre-Roll month-over-month lift against a 34.07% Flower month-over-month drop indicates that incremental gains are being sourced from core SKUs rather than cross-category trade-up, and the 179.32% year-over-year Flower jump coupled with an 11.96% Pre-Roll year-over-year decline implies that diversification potential exists but is not yet dependable for sustained share shift. The takeaway is that maintaining rank and near-term momentum likely depends on reinforcing Pre-Roll depth while selectively curating Flower to reduce volatility, rather than pursuing broad mix expansion.

Competitive Landscape

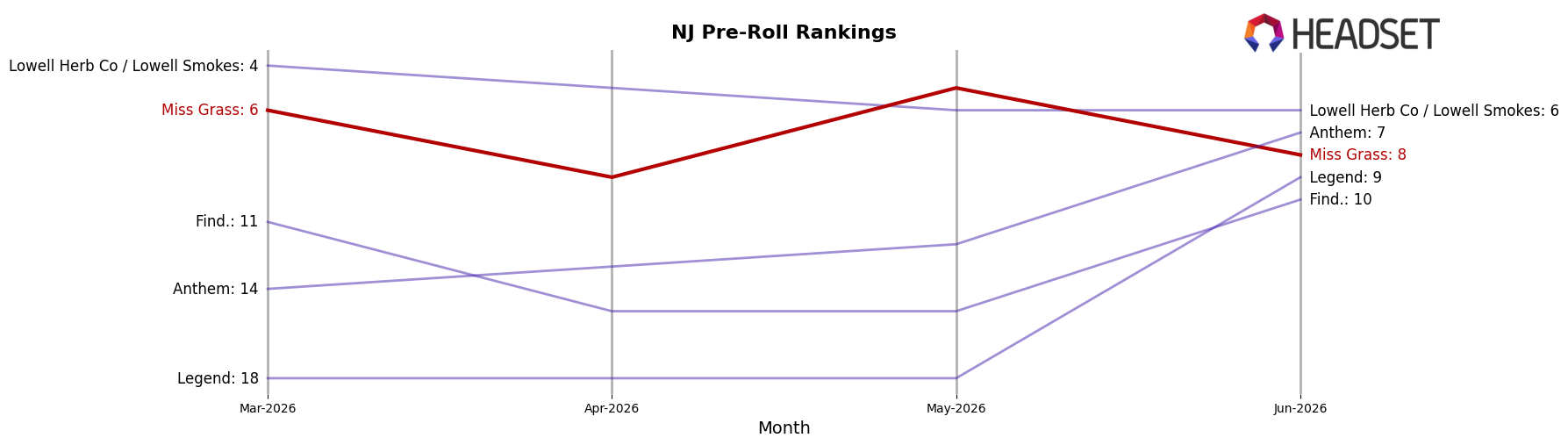

Miss Grass sits at rank 8 in June 2026, unchanged year over year at 8, after slipping 2 positions since March 2026 when it was 6; this follows a peak at rank 1 in September 2024, marking a multi-quarter comedown in placement. In contrast, RYTHM holds rank 1 after moving up from 2 year over year while posting a -2.4% sales change, and Ozone climbed from rank 9 to 2 with +155.7% sales growth, indicating share is consolidating at the top. Meanwhile, Garden Greens slipped from rank 1 to 3 alongside a -45.0% sales decline, whereas Full Tilt Labs jumped from rank 38 to 5 with +656.6% sales growth, reinforcing that upward mobility is still possible but increasingly concentrated among a few movers. The pattern implies Miss Grass’s flat year-over-year rank at 8 and 2-place drop since March 2026 signal entrenchment in the second tier while faster-moving rivals reallocate demand at the top.

Notable Products

All Times Minis Pre-Roll 5-Pack (2g) posted the steepest decline in June 2026 at -37.7% and sat at rank 5, while All Times - Hybrid Blend Pre-Roll 5-Pack (2g) dropped -17.0% to rank 2. In contrast, Fast Times - Gelato x Gelonade Diamond Infused Pre-Roll 5-Pack (2g) climbed +55.6% to rank 3, narrowing the gap behind rank 1 despite Fast Times - Joels Lemonade x Drip Station Mini Pre-Roll 5-Pack (2g) slipping -5.0% at the top.

Pre-Rolls account for ten of the top ten SKUs, indicating full category concentration, and the mix skews toward Fast Times variants moving up the ranks while All Times variants lose share. This pattern implies a pivot toward higher-energy or infused propositions capturing momentum over legacy All Times blends, suggesting future assortment weight and promo spend should tilt toward Fast Times to defend the number 1–3 tier and recover the mid-pack.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.