Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

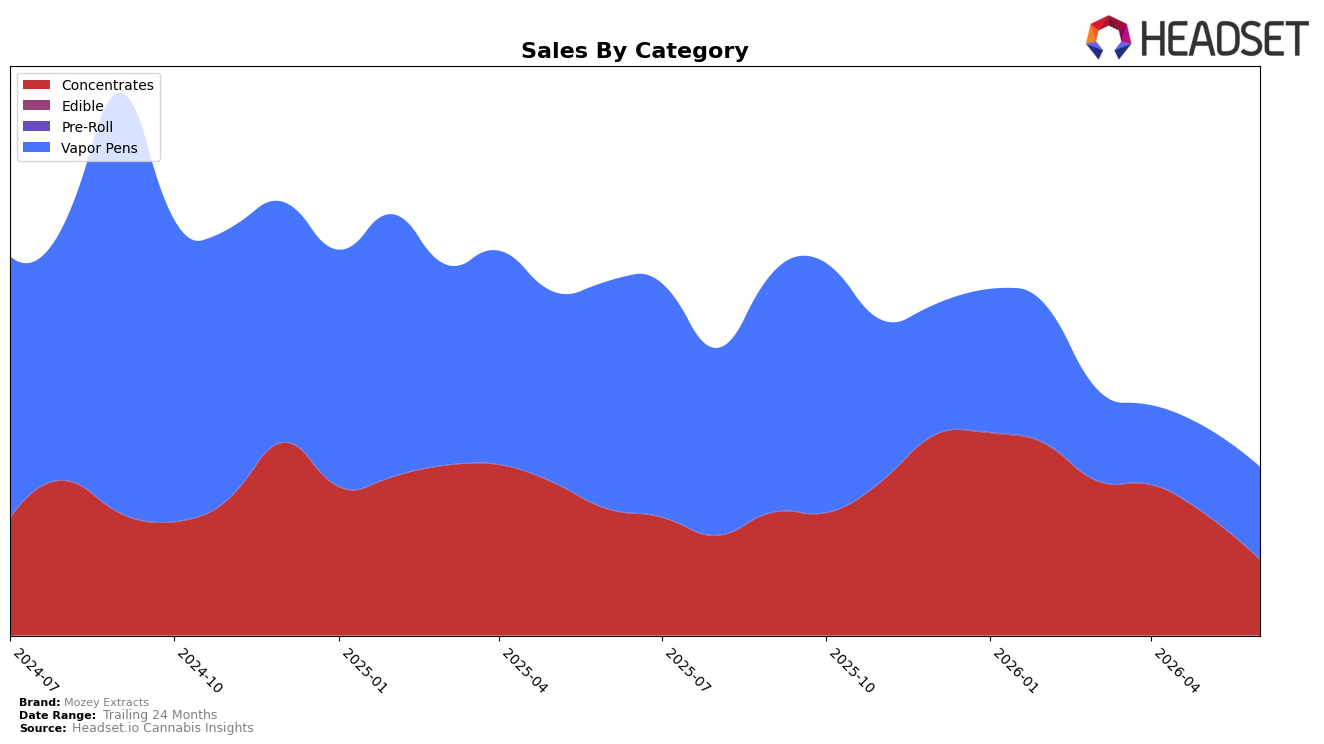

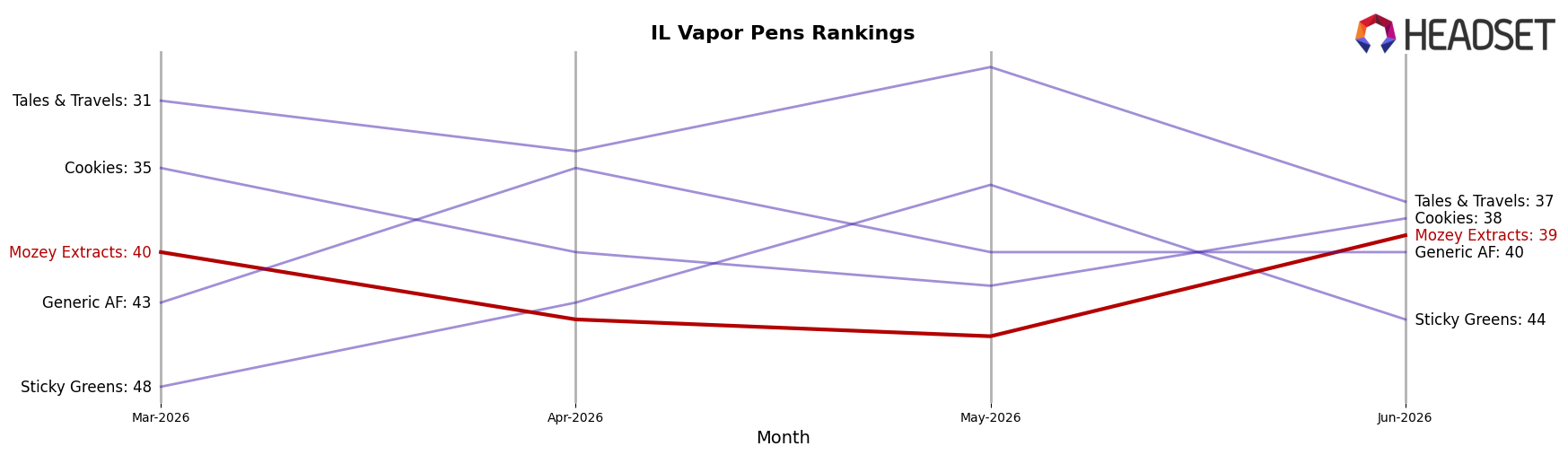

Mozey Extracts concentrated 54.86% of June 2026 sales in Vapor Pens and 45.03% in Concentrates, with Pre-Roll at 0.11%, indicating a two-category portfolio that now skews slightly toward Vapor Pens. Year over year, Vapor Pens declined 59.63% while Concentrates fell 40.03%, but month over month Vapor Pens rose 6.80% as Concentrates dropped 37.85%; Pre-Roll jumped 77.01% MoM off a minimal base. With overall brand sales down 52.60% year over year and average price up 42.29%, the pattern implies the mix is tilting toward a relatively higher-priced Vapor Pens core as a stabilizer while Concentrates is retrenching. In Illinois Vapor Pens, Mozey Extracts ranks 39, so the MoM Vapor Pens uptick paired with a double-digit MoM decline in Concentrates suggests category focus is consolidating where the brand still holds shelf presence.

The shift toward Vapor Pens at a 54.86% share alongside a 6.80% MoM lift, contrasted with a 37.85% MoM contraction in the 45.03% Concentrates share, implies resource and promotional weight should prioritize SKUs and price tiers that can defend or improve the rank 39 position. With brand sales down 52.60% YoY while average price rose 42.29% and Vapor Pens pricing at $25.85 versus Concentrates at $25.10, current pricing strategy risks volume erosion in weaker lanes, so tightening price-pack architecture in Concentrates while sustaining margin in Vapor Pens is the practical path. The minimal but 77.01% MoM growth in 0.11% Pre-Roll signals a test-and-learn niche rather than a scale driver, meaning portfolio breadth can remain narrow and execution should center on Vapor Pens velocity recovery and selective Concentrates retention.

Competitive Landscape

Mozey Extracts sits at rank #39 in IL Vapor Pens in June 2026, slipping 12 positions from #27 year over year, after a modest 1-place improvement from #40 in March 2026; the brand’s prior peak was #19 in September 2024, marking a 20-rank descent from that high. In contrast, &Shine held #1 with a -12.7% year-over-year sales change while Select stayed #2 with a -6.8% decline, indicating that leaders preserved rank despite contraction, whereas Mozey Extracts’ double-digit rank drop suggests share ceding at the fringes of the top 40. The pattern implies Mozey Extracts is locked in a slow bleed—small quarter-to-quarter stability but a longer glide from its September 2024 peak—requiring gains of at least 10–15 ranks to reenter the competitive tier where modest declines still maintain position.

Notable Products

Beach Sand Bubble Hash (1g) led June 2026 with a 135.5% month-over-month surge and the number 1 rank, while Pineapple Diesel Distillate Cartridge (1g) posted a more modest 22.0% MoM gain at rank 7, pointing to momentum concentrated in value-forward concentrates rather than vapor pens. FX- THC/CBD/CBN 5:1:1 Banana Pajama Distillate Disposable (0.5g) fell 42.6% MoM at rank 6 and Apple Fritter Beach Sand Bubble Hash (1g) declined 36.6% at rank 9, suggesting volatility at the edges even as the flagship concentrate scaled to $17,098. Concentration is evident with four of the top ten in Concentrates and five in Vapor Pens, implying a barbell mix where a single breakout concentrate offsets mixed performance in pens. The pattern implies Mozey Extracts is tilting commercial focus toward scalable, lower-priced concentrate formats while selectively pruning underperforming vapor pen variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.