Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Muncheas is stocked at 38 licensed dispensaries across Massachusetts, with the deepest coverage in Boston, Fall River, Haverhill, Lowell, and Middleborough. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

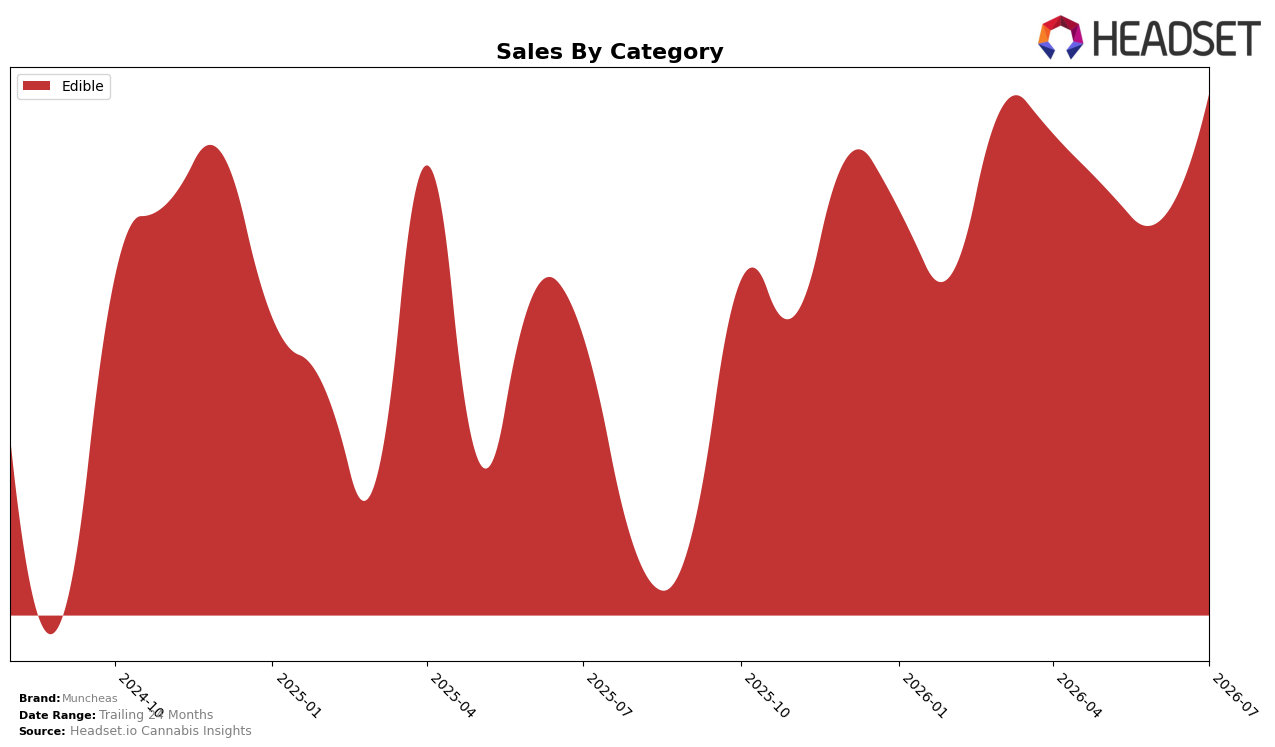

Muncheas operated as a single-category brand in July 2026, with Edible accounting for 100.0% of sales and posting a 28.1% year-over-year increase alongside a 13.2% month-over-month gain, while average price fell 30.0% year-over-year to $7.04. Within the Massachusetts Edible landscape, the brand sat at rank 24, indicating volume gains are being driven by unit expansion rather than mix shifts, and the pricing compression suggests a trade-down or pack-size strategy that prioritizes velocity over margin.

The combination of a 28.1% year-over-year sales rise and a 13.2% month-over-month bump at a 30.0% year-over-year price decline implies that Muncheas is leaning into price-accessible Edibles to capture share, positioning itself as a scale player rather than a premium niche. Holding the number 24 rank in Massachusetts Edibles with 100.0% category concentration points to a focus on depth within a single aisle; this concentration increases exposure to Edible-specific price cycles but also concentrates marketing and distribution advantages where unit throughput is already accelerating.

Competitive Landscape

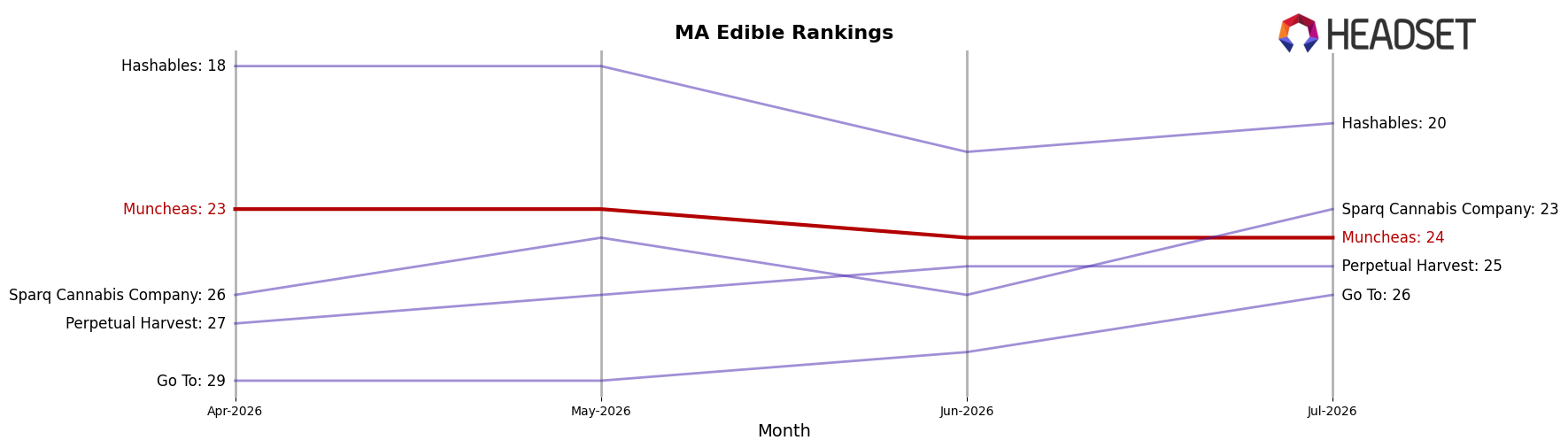

Muncheas ranks #24 in MA Edible in July 2026, sliding 1 position year over year from #23 and also down 1 spot from April 2026 when it was #23; versus its peak at #20 in October 2025, the brand sits 4 ranks lower while the category’s leaders moved upward, as Camino climbed from #2 to #1 and Wyld advanced from #5 to #3 alongside a 29.7% YoY sales lift, indicating Muncheas is losing relative share as faster-rising competitors consolidate top-5 positions and the current trajectory points to further mid-pack drift without a reversal in rank momentum.

Notable Products

Red Raspberry Fruit Gems Gummies 20-Pack (100mg) delivered the standout movement in July 2026 with a 199.9% month-over-month surge into rank 9, while Cran-Grape Fruit Gems Gummies 20-Pack (100mg) fell 62.1% to rank 10, signaling volatility at the tail of the top ten. Tropical Fruit Gems Gummies 20-Pack (100mg) jumped 121.7% to rank 2 as Green Apple Fruit Gems Gummies 20-Pack (100mg) slipped 8.1% at rank 3, indicating flavor rotation rather than broad demand erosion. With all ten top SKUs in the Edible category and the Strawberry Fruit Gems Gummies 20-Pack (100mg) holding rank 1 on $16,383 in sales, the mix points toward a deepening commitment to gummies where rapid flavor-specific swings can be used to tactically refresh shelf momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.