Market Insights Snapshot

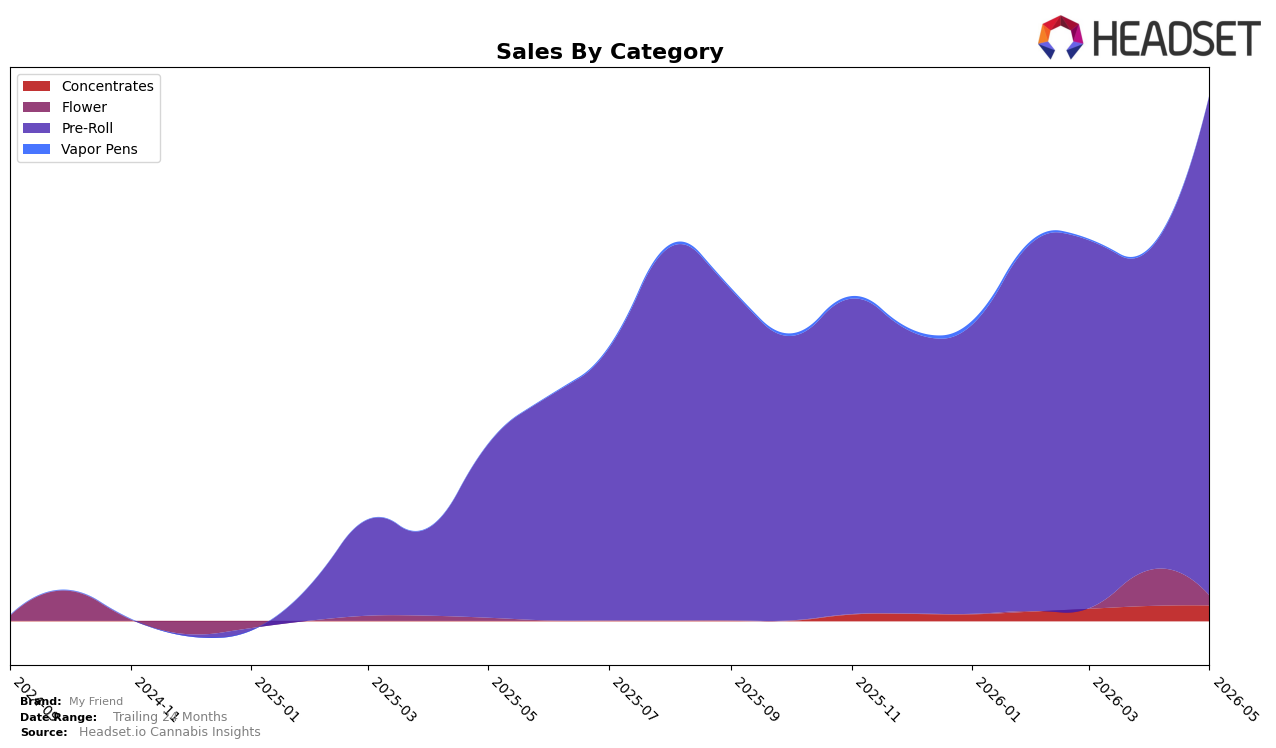

My Friend concentrated 95.23% of May 2026 sales in Pre-Roll, up 55.96% month over month and 188.68% year over year, while the smaller Flower slice at 1.82% swung sharply with a -73.13% MoM drop against a 257.60% YoY rise. Concentrates held 2.94% share with a 3.25% MoM uptick, and overall brand sales grew 198.23% YoY alongside a 15.30% YoY decrease in average price to $1.71, with Pre-Roll pricing at $1.63. The mix indicates over-reliance on Pre-Roll for momentum and price-led volume, with volatility in Flower suggesting tactical rather than structural gains.

Positioning is anchored in value-led Pre-Roll scale, as evidenced by a 95.23% category share and a May 2026 rank of 21 in Michigan Pre-Roll, but the -73.13% MoM contraction in Flower against a 257.60% YoY lift signals episodic wins rather than sustained penetration. With Concentrates at 2.94% share and only 3.25% MoM growth versus Pre-Roll’s 55.96% MoM surge, the current stance prioritizes depth in one category over breadth, implying that maintaining rank will depend on holding the Pre-Roll price-to-volume equation while selectively stabilizing secondary categories.

Competitive Landscape

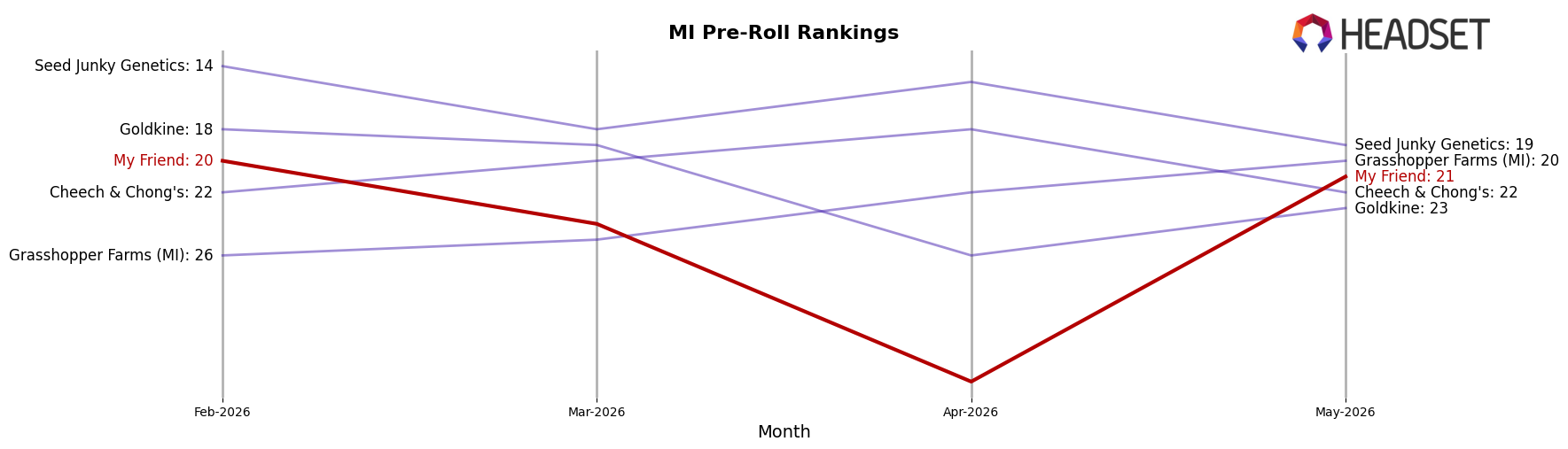

My Friend sits at rank #21 in May 2026, a 41-place climb from #62 year over year, while slipping 1 spot from #20 in February 2026 to #21 currently; the brand also fell 1 position from #20 three months ago to #21, indicating recent consolidation after a sharper annual rise. In contrast, Jeeter held at #1 year over year with a -26.4% YoY sales change, and Mitten Extracts improved rank from #5 to #4 alongside a +35.3% YoY sales change, positioning those leaders differently on momentum versus stability. The pattern implies My Friend’s rank trajectory is transitioning from rapid recovery to a plateau near the top-20, suggesting market share gains have slowed and future movement will depend on displacing peers clustered around ranks #15–#25.

Notable Products

Blumosa Pre-Roll (1g) set the tone with a 127.99% month-over-month surge to rank 1 in May 2026, overtaking Super Boof Pre-Roll (1g) despite Super Boof’s 47.79% gain at rank 2. With GMO Pre-Roll (1g) up 12.37% at rank 6 and eight other top-10 spots occupied by the same format, ten of the top ten are Pre-Roll SKUs, indicating a concentrated pull toward a single category that reduces portfolio diversification risk only if pricing power holds. The dollar lead sits with Super Boof Pre-Roll (1g) at $26,267 while Blumosa Pre-Roll (1g) holds the higher rank, implying that velocity rather than ticket size is dictating shelf position. The pattern points to My Friend leaning into rapid-turn Pre-Roll winners, suggesting near-term share capture will hinge on sustaining outsized MoM gains in a narrow product lane.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.