Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Nebula is stocked at 48 licensed dispensaries across Minnesota, Oklahoma, and 3 other states, 25 of them in Minnesota, with the deepest coverage in Minneapolis, Saint Paul, Luverne, Andover, and Anoka. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

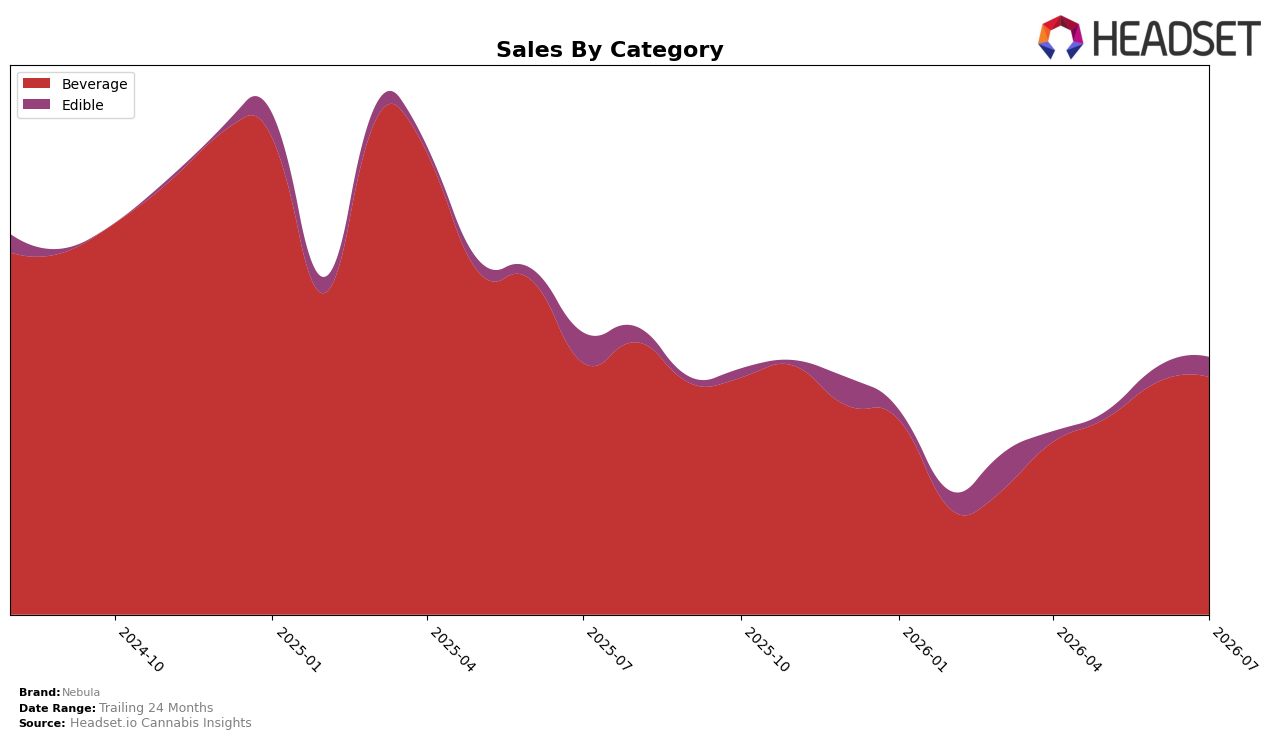

Nebula’s July 2026 mix is concentrated in Beverage at 92.30% share with a year-over-year decline of 5.66% alongside a month-over-month increase of 2.15%, while Edible holds 7.70% share with a year-over-year decline of 34.39% and a month-over-month rise of 30.44%. Average price fell 11.70% year over year to $11.18 as Beverage price points sit at 10.59 and Edible at 34.42, and Nebula ranked 7 in Beverage in Arizona; together, the softer Beverage decline versus Edible and a sequential Beverage uptick indicate near-term stability anchored in Beverage with selective Edible recovery that does not yet offset broader year-over-year contraction.

The shift toward a 92.30% Beverage reliance with a 2.15% month-over-month lift, contrasted with a 34.39% year-over-year Edible drop and a 30.44% month-over-month rebound, implies Nebula’s positioning is skewed to defending Beverage rank 7 in Arizona while testing price-sensitive Edible pockets. The 11.70% year-over-year price decrease alongside a 5.66% Beverage sales decline suggests price-led elasticity is stronger in Beverage than Edible, and the widening category gap points to prioritizing Beverage depth over breadth, with Edible serving as a tactical, higher-ticket but volatile adjunct.

Competitive Landscape

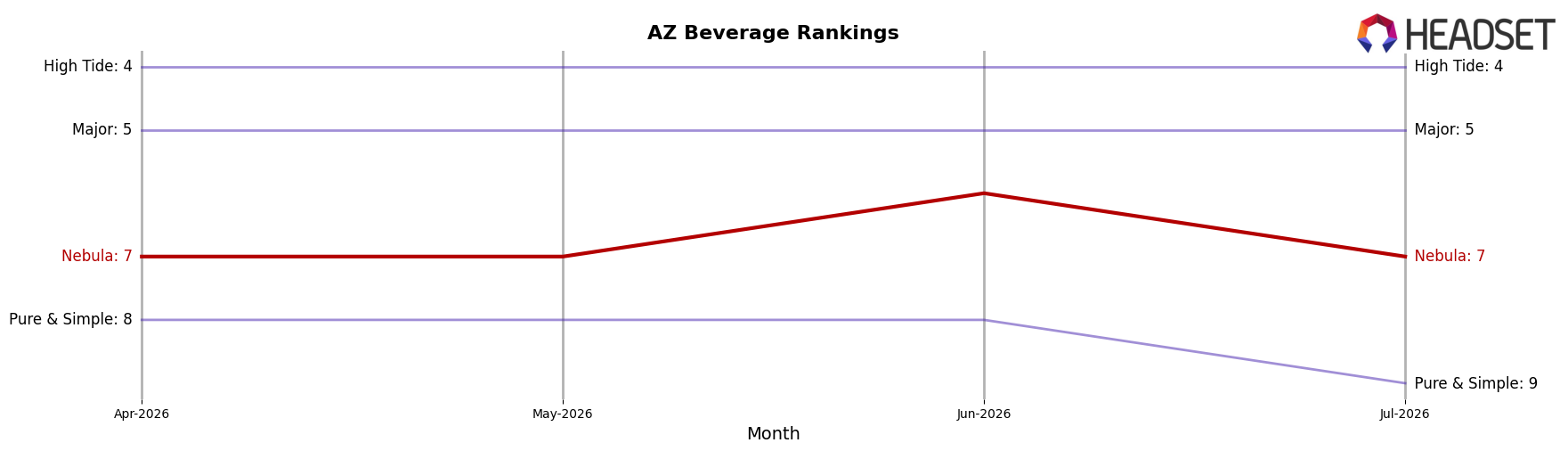

Nebula sits at #7 in AZ Beverage for July 2026, slipping 2 ranks year over year from #5 while holding flat versus April 2026 at #7; that two-position YoY drop contrasts with Uncle Arnie's climbing from #4 to #3 alongside a 223.4% YoY sales increase, and diverges from Sip Elixirs holding #2 despite a -6.0% YoY sales change. Compared with Keef Cola entrenched at #1 with +16.9% YoY growth while Nebula remains 4 ranks below its September 2024 peak of #3, the pattern indicates Nebula’s rank trajectory is stabilizing mid-pack rather than rebounding toward prior peak, implying share defense priorities over climb initiatives.

Notable Products

CBD/THC 1:1 Hybrid Tiger's Blood Syrup (100mg CBD,100mg THC) posted the largest month-over-month surge at 64.7% and climbed into rank 8, outpacing Blue Razz Nectar Syrup (100mg) which rose 57.4% to hold rank 1. In contrast, Wild Strawberry Nectar Syrup (100mg) fell 33.1% while Tigerblood Nectar Syrup (1000mg) declined 14.8%, and Nectar - Pure Unflavored Syrup (100mg, 1oz) dropped 24.4%, signaling volatility at both flavor and potency extremes. With four of the top five ranks occupied by 100mg Beverage SKUs and only one 1000mg SKU remaining in the top 10, July 2026 demand consolidated around standard-dose syrups despite mixed results among unflavored and strawberry variants. The product mix implies Nebula is tilting toward flavor-led, 100mg formats with selective traction for 1:1 hybrids, suggesting near-term emphasis on mainstream dosage and flavor rotation over high-potency niche offerings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.