Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

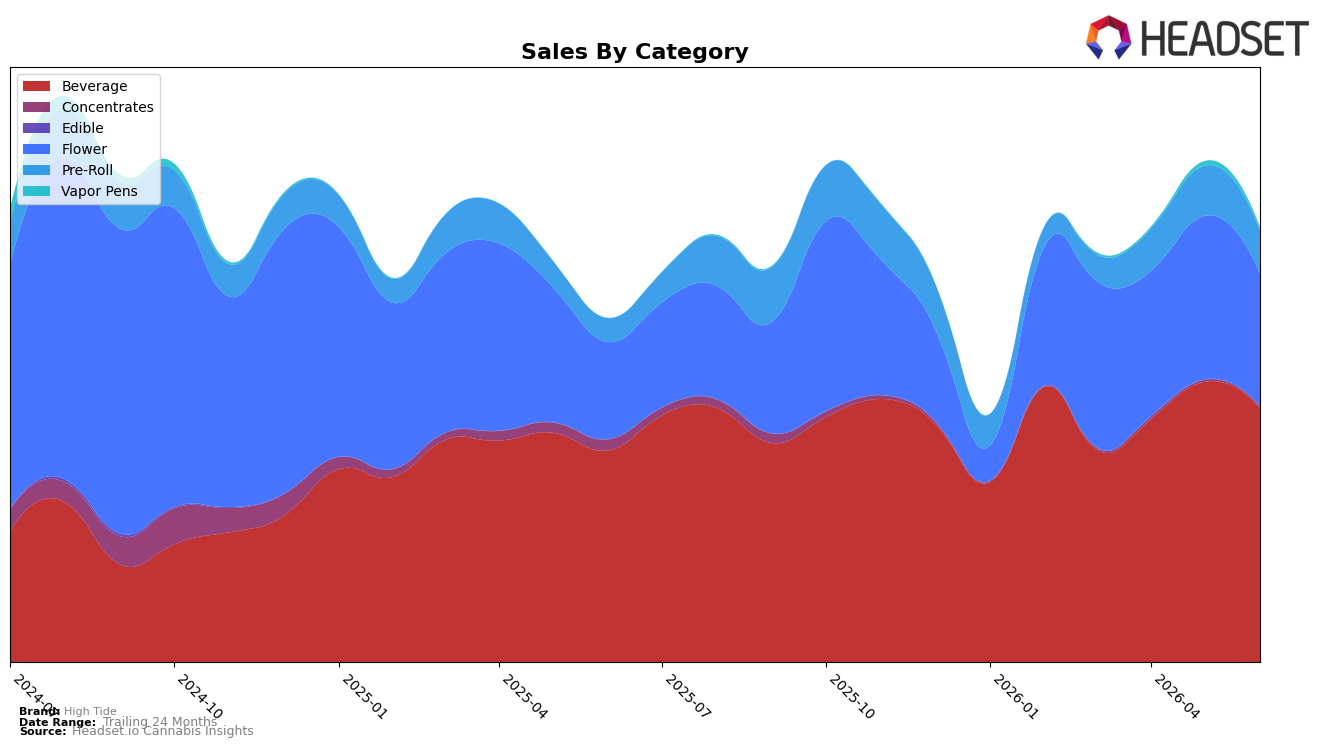

In June 2026, High Tide concentrated 58.51% of sales in Beverage with 19.90% year-over-year growth but a 9.46% month-over-month decline, while Flower held 30.51% share with 36.70% YoY growth and a 19.01% MoM pullback. Pre-Roll reached 9.80% share on 79.16% YoY growth yet fell 15.05% MoM, and Concentrates contracted to 0.38% share with an 84.85% YoY decline and a 6.98% MoM dip. The aggregate picture is a portfolio leaning on Beverage scale and Flower momentum but exposed to intra-month volatility, implying reliance on repeatable lower-price unit velocity rather than sustained basket expansion.

With Beverage as the top category and an average price of $3.09 against a brand-wide average price rising 6.95% YoY, mix is tilting toward lower price points even as Flower carries a higher ticket at $25.78, indicating a barbell that lifts traffic but compresses mix-driven revenue per unit. The Beverage-led share coupled with a rank of 4 in Arizona Beverage suggests competitive proximity to the top tier, yet the double-digit MoM declines in Beverage (9.46%) and Flower (19.01%) point to sensitivity to promotional or seasonal cycles; the positioning implication is to defend Beverage share while converting part of Flower and Pre-Roll’s 36.70% and 79.16% YoY gains into steadier month-to-month baselines to stabilize rank and margin.

Competitive Landscape

High Tide is ranked #4 in AZ Beverage in June 2026, down 1 place from #3 year over year, and it has held #4 for the past three months while peaking at #3 in February 2026; this contrasts with Keef Cola holding #1 with a 7.7% YoY sales increase and Uncle Arnie's climbing from #5 to #3 alongside a 391.8% YoY sales surge. Compared with Sip Elixirs steadying at #2 despite a 3.4% YoY sales decline and Major sitting at #5 with no reported YoY metrics, High Tide’s 1-rank YoY slippage and zero rank change since March 2026 indicate a stall below the top three, implying near-term share defense matters more than upside unless momentum shifts from incumbents above.

Notable Products

CBD/THC 1:1 Raspberry Lemon THC Seltzer (10mg CBD, 10mg THC, 12oz, 355ml) posted a 142.6% month-over-month surge to rank 3 in June 2026, while Unicorn Factory (3.5g) fell 13.2% to rank 10. Peach Mango Seltzer Beverage (10mg THC, 12oz) grew 19.5% and held rank 1, whereas CBD/CBC/THC 1:1:1 Pomegranate Blueberry Seltzer (10mg CBD, 10mg CBC, 10mg THC, 12oz, 355ml) slipped 12.4% at rank 8. With eight of the top ten SKUs in Beverage, the mix indicates High Tide is tilting toward flavored seltzers over inhalables as the growth engine.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.