Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

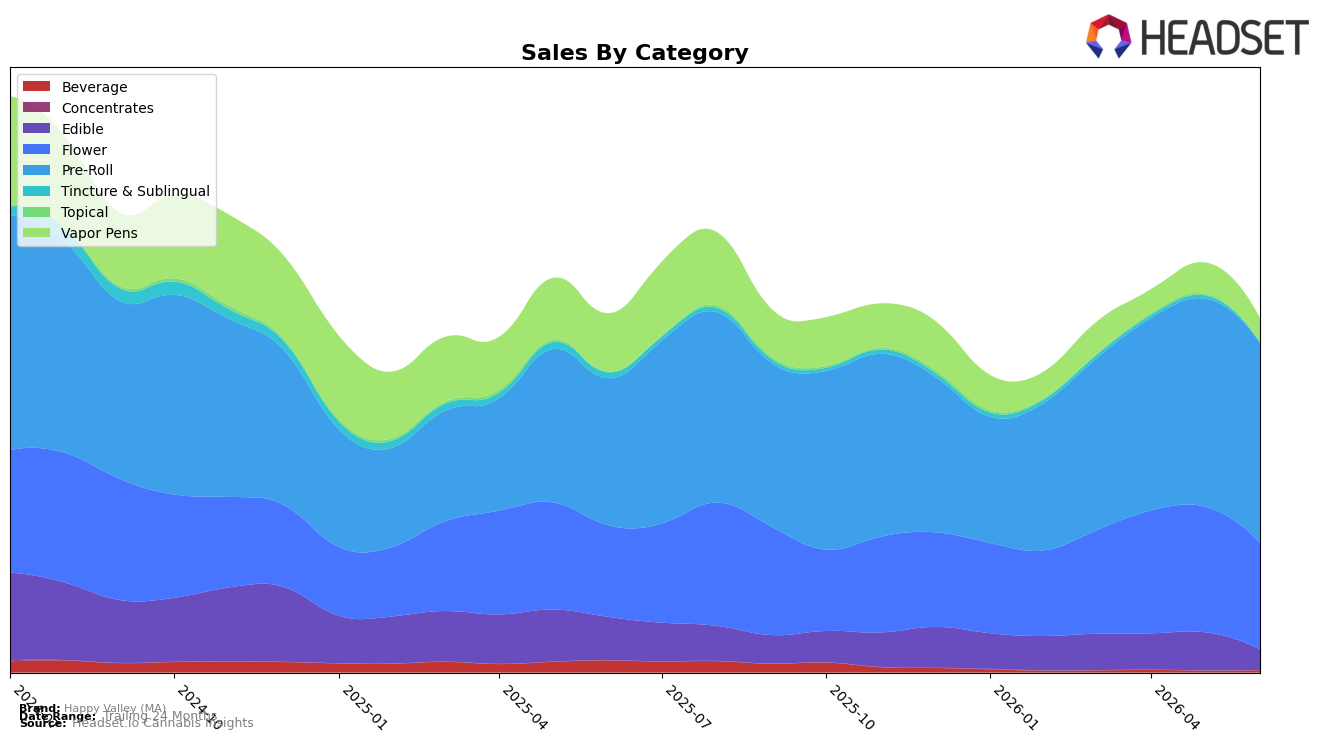

In June 2026, Happy Valley (MA) concentrated 56.55% of sales in Pre-Roll with year-over-year growth of 35.86% but a month-over-month decline of 3.93%, while Flower held 30.09% share with 16.30% YoY growth and a sharper 15.30% MoM decline. Vapor Pens contracted to 6.72% share with YoY down 59.09% and MoM down 23.59%, and Edible fell to 5.79% share with YoY down 52.60% and MoM down 46.13%. Smaller formats retreated: Topical slipped 73.13% MoM and 47.29% YoY, and Tincture & Sublingual plunged 88.93% MoM and 94.01% YoY, while Beverage is only 0.63% share despite a 23.67% MoM uptick and an 81.37% YoY decline. The pattern implies a pivot toward combustion-led volume where Pre-Roll and Flower gains offset collapses in ingestibles and wellness forms, concentrating revenue risk in two inhalable categories.

Average price declined 18.02% YoY to $16.08 alongside a Pre-Roll average price of $12.52 and Flower at $29.07, which, combined with Pre-Roll’s 56.55% share and Flower’s 30.09% share, shifts the mix toward lower ticket items even as Pre-Roll posts 35.86% YoY growth. With Vapor Pens down 59.09% YoY and Edible down 52.60% YoY while Beverage shows a 23.67% MoM rebound off an 81.37% YoY base, the assortment is thinning outside inhalables, and the brand’s rank of 7 in Massachusetts Pre-Roll suggests reliance on that lane. The implication is a price-led, value-leaning posture anchored in Pre-Roll scale that can win share in inhalables but may limit cross-format basket expansion unless the brand reins in the double-digit MoM declines in Flower and revives at least one ingestible format.

Competitive Landscape

Happy Valley (MA) sits at rank #7 in MA Pre-Roll for June 2026, improving 1 position year over year from #8, but holding flat versus March 2026 at #8 to #7 signals only a modest upward step while the category’s top tier is moving faster; Cali-Blaze vaulted from #32 to #2 and expanded sales by 472.5%, and Northern Grown advanced from #18 to #4 with 120.0% growth, whereas Jeeter held #1 to #1 with 17.2% growth and Nature's Heritage edged from #4 to #3 with 18.3% growth; given the brand’s peak at #4 in August 2024 and its current position at #7, the rank trajectory implies a loss of relative momentum against faster-rising rivals and a need to counter accelerating share consolidation at the top.

Notable Products

Banana Jealousy Pre-Roll (1g) posted the standout move in June 2026 with a 94.7% month-over-month gain and rose to rank 2, while Super Lemon Haze Pre-Roll (1g) fell 22.4% but still held rank 1. Super Lemon Haze (3.5g) declined 14.5% and sat at rank 6, and Donny Burger x Banana Jealousy Pre-Roll (1g) slipped 12.3% at rank 5. With eight of the top ten being Pre-Roll SKUs and Lime Wreck Haze Pre-Roll (1g) adding a 48.9% lift at rank 4, the mix points to a pivot toward single-gram pre-roll velocity over flower, even as one flagship flower SKU still contributes over $100,000.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.