Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

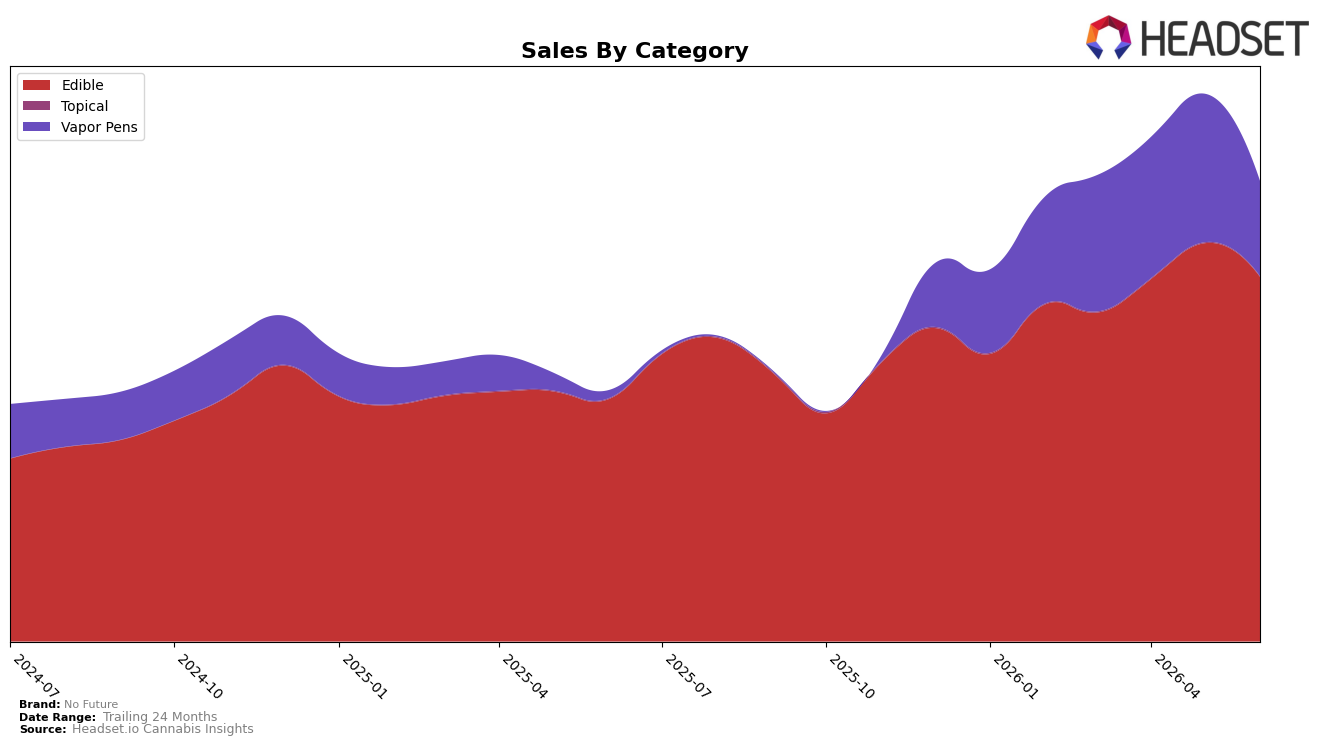

In June 2026, No Future concentrated 79.27% of sales in Edible with year-over-year growth of 50.63% but a month-over-month decline of 8.45%, while Vapor Pens expanded to 20.64% share on an 1109.19% year-over-year surge despite a 35.98% month-over-month pullback; Topical remained a negligible 0.09% share with a 23.03% year-over-year drop and a 33.84% month-over-month decline. Average price jumped 209.11% year over year to $9.47, with category-level pricing at $8.16 for Edible and $25.94 for Vapor Pens, and No Future held rank 2 in Edible in British Columbia; the mix shift and divergent MoM trends imply a portfolio balancing act where rapid Vapor Pens scale-up offsets Edible softness, but short-term MoM retrenchment flags volatility that could affect pricing power and rank.

The combination of 83.66% brand sales growth year over year alongside an 8.45% Edible MoM dip and a 35.98% Vapor Pens MoM decline suggests that recent gains rely on new-buyer or channel expansion cohorts rather than steady repeat velocity, and the 79.27% Edible dependence versus 20.64% Vapor Pens concentration implies exposure if seasonal or promotional cycles tighten. Holding rank 2 in Edible while Vapor Pens posts four-digit year-over-year growth signals a positioning pivot toward a two-pillar model where Edible anchors traffic and Vapor Pens supplies incremental basket value; however, the simultaneous MoM declines across both pillars indicate execution risk in monthly cadence, meaning sustaining rank and share will likely hinge on stabilizing Vapor Pens replenishment while protecting Edible price-value as the $9.47 average price resets consumer expectations.

Competitive Landscape

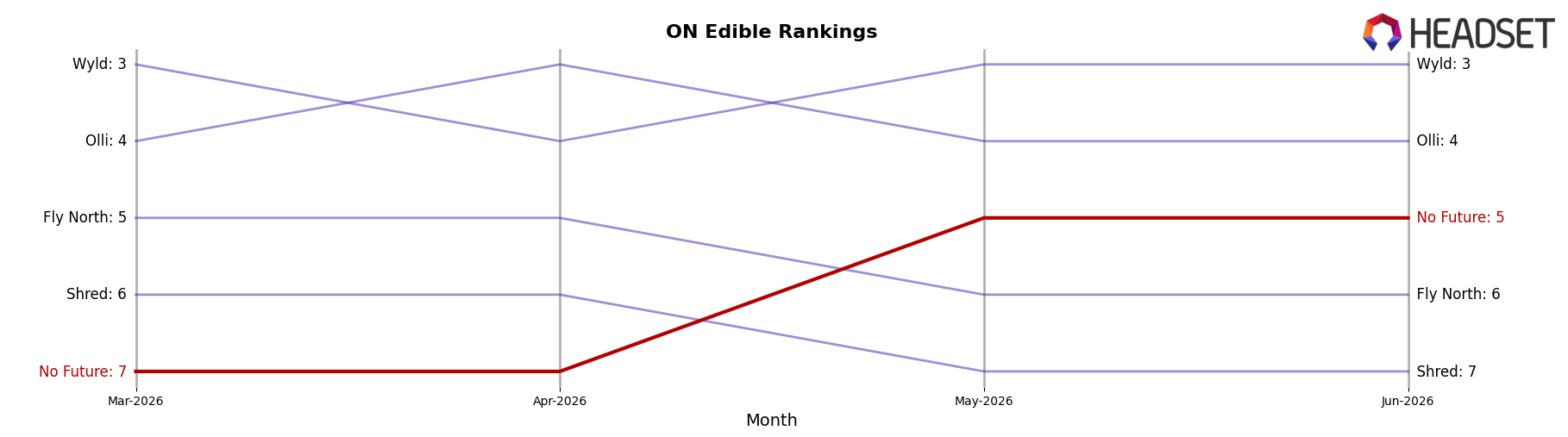

No Future sits at rank #5 in ON Edible in June 2026, unchanged YoY at #5, but it has moved up 2 positions since March 2026 (#7 to #5) while still trailing its peak of #4 from October 2025; meanwhile, Wyld climbed from #4 to #3 YoY and Olli advanced from #7 to #4, indicating lateral pressure from brands gaining 1–3 ranks as category momentum consolidates above No Future. With Spinach holding #1 YoY and in June 2026 and Gron / Grön steady at #2, the corridor between ranks #2–#5 is tightening as Olli’s triple-digit YoY sales growth (+120.7%) and Wyld’s +21.9% expansion convert into rank share, implying No Future’s stable YoY rank masks increasing risk of being boxed out of its October 2025 peak lane unless it converts its 2-position spring recovery into sustained share capture.

Notable Products

The Green One Indica Gummy (10mg) posted the steepest move in June 2026 at -29.9% MoM while holding rank 8, compared with The Blue One Sativa Bonbon Gummy (10mg) at -10.1% MoM in rank 1 and The Purple One Sativa Bonbon Gummy (10mg) at -10.1% MoM in rank 2. Across the top ten, 100% of SKUs are Edibles, and the concentration in color-themed 10mg gummies at ranks 1, 2, 6, 8, and 10 implies a narrow flavor-led lineup despite only one SKU showing MoM growth above +10%. The 10x The Madness Ratiod - CBD/CBG/THC 1:2:1 Tropic Boost Gummies 10-Pack (100mg CBD, 200mg CBG, 100mg THC) rose +12.3% MoM at rank 7 while Ratioed - CBD/CBN/THC 2:1:1 Moon Berry Gummies 10-Pack (200mg CBD, 100mg CBN, 100mg THC) was roughly flat at +0.9% in rank 5, suggesting ratioed functional formats are gaining traction relative to single-compound or simple 10mg SKUs. This mix points to a pivot opportunity toward higher-complexity, multi-cannabinoid packs to offset double-digit declines in flagship 10mg gummies and stabilize the top ranks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.