Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

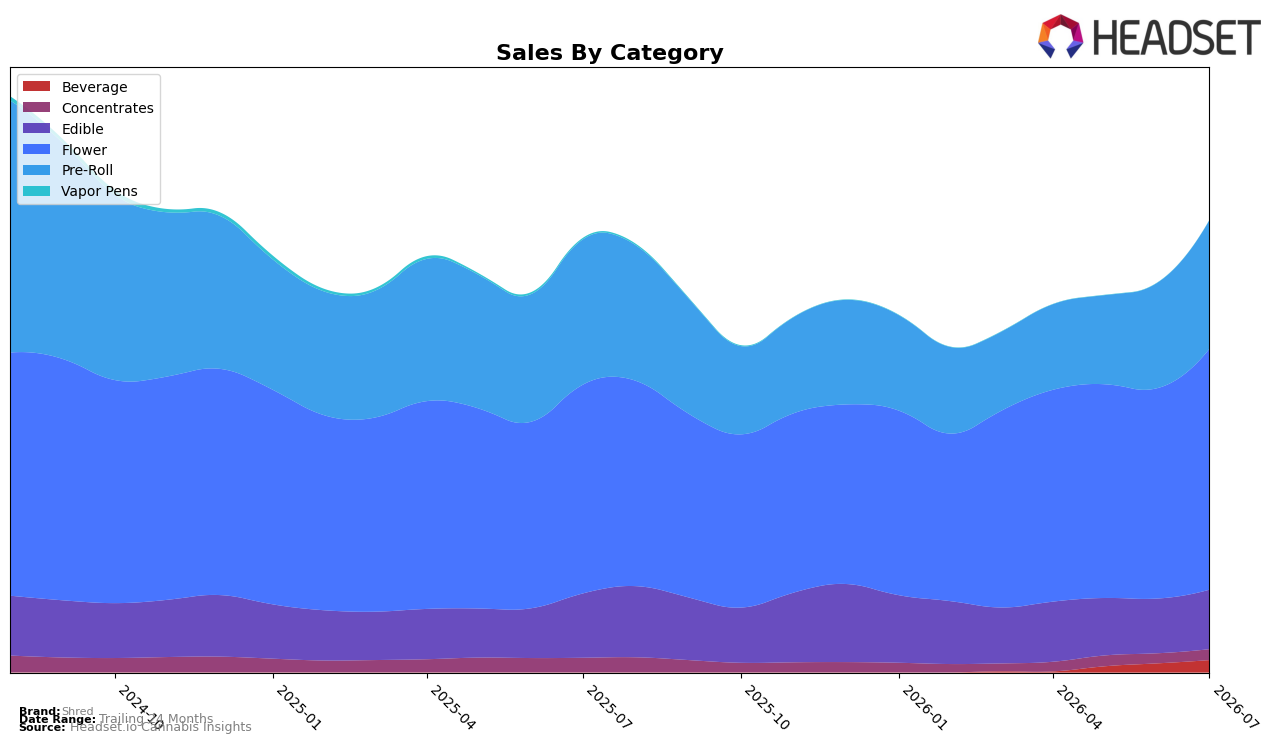

Shred’s July 2026 category mix tilted further toward Flower at 53.32% share, with Flower sales up 15.40% year over year and 14.46% month over month, while Pre-Roll held 28.46% share but declined 11.48% YoY despite a 21.85% MoM rebound. Edible contributed 13.13% share with a 7.63% YoY decline and an 8.75% MoM uptick, and Beverage, though only 2.72% share, accelerated 35.55% MoM as Vapor Pens collapsed to 0.00% share on a 99.57% YoY and 90.59% MoM drop. With an 18.91% YoY increase in average price alongside total brand sales up 4.13% YoY, the mix suggests volume softness outside Flower and Pre-Roll’s YoY drag, implying growth is concentrated in higher-priced Flower while peripheral categories either stabilize or contract.

Positioning implications point to a Flower-led identity in Ontario, where rank in Flower is 1 and the category’s 14.46% MoM and 15.40% YoY gains can offset Pre-Roll’s 11.48% YoY decline and Concentrates’ 25.69% YoY slide. The 35.55% MoM lift in Beverage and 8.75% MoM rise in Edible provide optionality, but the collapse in Vapor Pens (−99.57% YoY; −90.59% MoM) concentrates assortment risk; therefore, the pattern implies Shred’s defensible position rests on sustaining Flower pricing power while using Beverage and Edible momentum to diversify away from single-category dependency.

Competitive Landscape

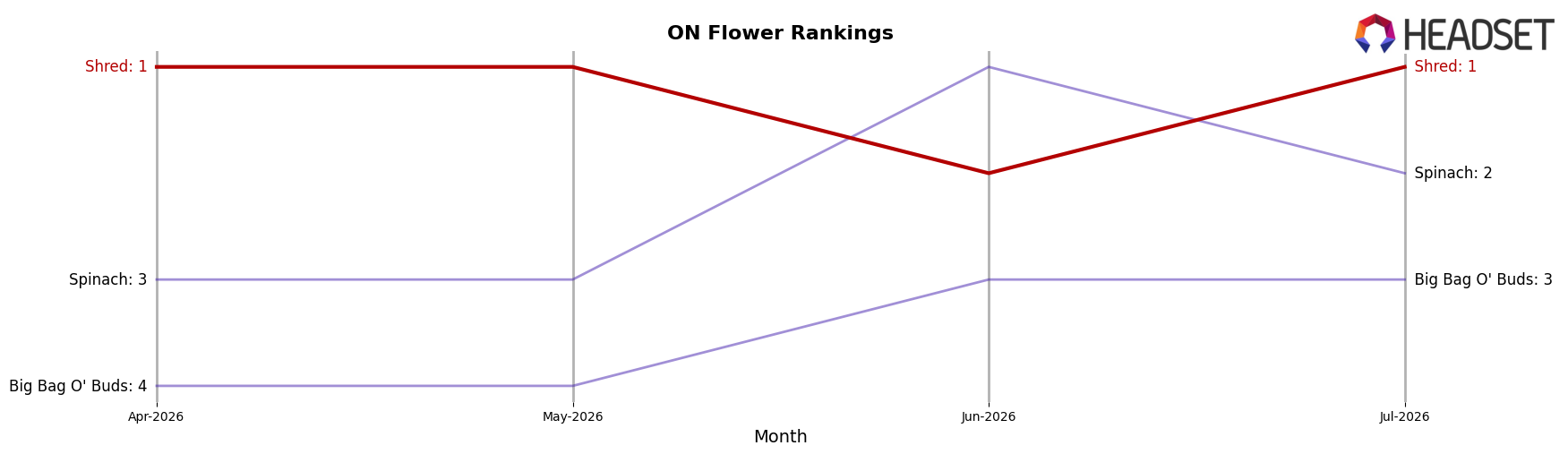

Shred sits at rank #1 in Ontario Flower in July 2026, up 1 position from #2 year over year, and unchanged from #1 three months ago, signaling a consolidation at the category peak; meanwhile, Spinach advanced from #4 to #2 with a 31.1% year-over-year sales increase, while Back Forty / Back 40 Cannabis slipped from #1 to #4 alongside a 5.4% sales decline, indicating that Shred’s upward rank change and maintained peak in July 2026 imply durable share defense against both upward and downward competitive movements.

Notable Products

The steepest decline under -10% did not occur, so the standout is the largest acceleration: Funk Master (7g) jumped +26.3% MoM to rank 8 while Dartz - Gnarberry Pre-Roll 10-Pack (4g) surged +36.4% MoM to rank 5, as Gnarberry (7g) also rose +12.4% at rank 2; four of the top ten are Flower SKUs, concentrating momentum in inhalables. Shred'ems - CBD/THC 4:1 Wild Berry Blaze Gummy 4-Pack (40mg CBD, 10mg THC) grew +11.2% at rank 1 while Shred'em Pop! - Crazy Cream Soda Gummies 4-Pack (10mg) added +9.8% at rank 3, but the absence of any >+50% MoM spikes contrasts with the steady Flower gains. The product mix points to Shred tilting its commercial direction toward Flower-led traffic drivers with complementary Edible anchors, implying assortment and promo weight are shifting to larger-format inhalables over novelty launches.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.