Where to Buy

OHHO is stocked at 56 licensed dispensaries across New York, with the deepest coverage in New York, Syracuse, Buffalo, Flushing, and Rochester. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

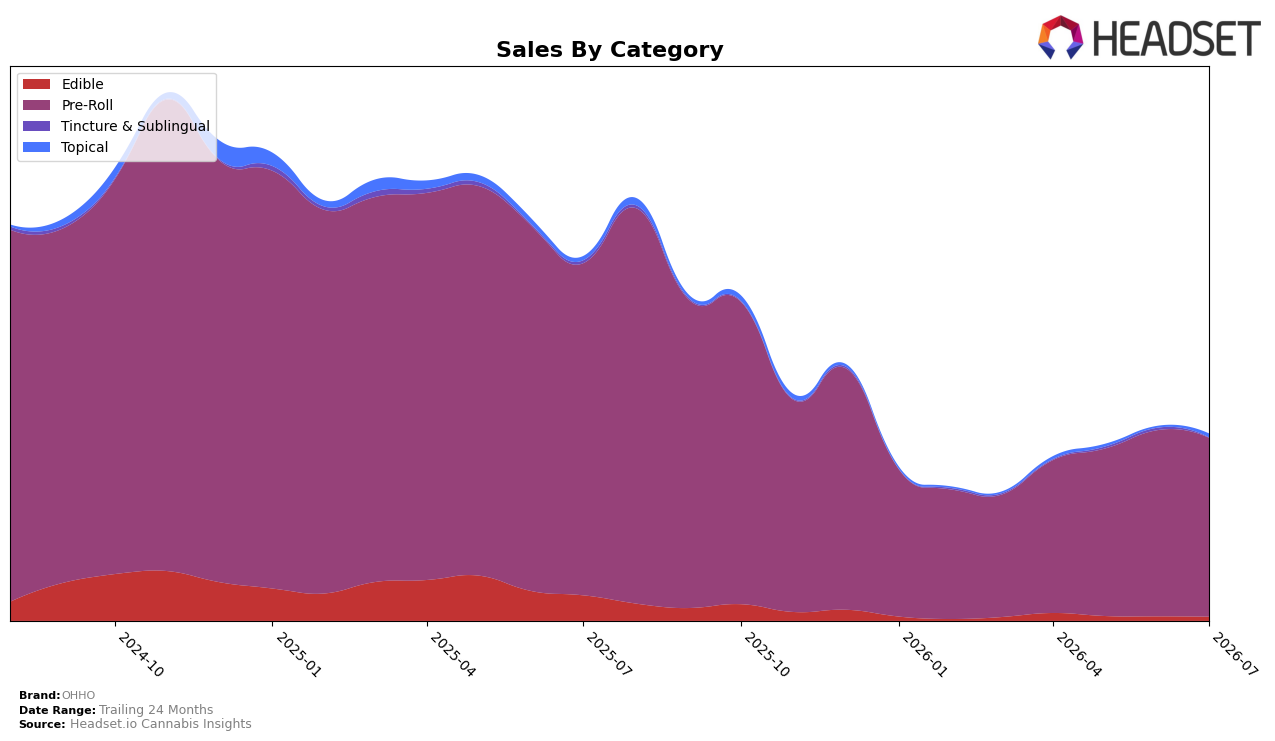

Market Insights Snapshot

OHHO concentrated 96.10% of July 2026 sales in Pre-Roll, where year-over-year sales fell 46.19% and month-over-month declined 3.96%, while Edible held 2.03% share with an 85.05% YoY drop and an 8.64% MoM decline. Topical expanded to 1.87% share on a 139.64% MoM surge despite an 8.82% YoY decrease, and the average price across the brand fell 8.56% YoY to $16.01 as Pre-Roll pricing sat at $15.69 versus Edible at $22.09. With Pre-Roll ranked 91 in New York and accounting for nearly all volume, the pattern implies overexposure to a contracting core and early diversification via Topical that is not yet large enough to offset the category’s YoY drag.

The mix shift—Pre-Roll down 46.19% YoY alongside a 3.96% MoM dip, versus Topical’s 139.64% MoM growth and only an 8.82% YoY decline—suggests OHHO’s near-term positioning benefits from leaning into niches less correlated with its core volatility. The 2.03% Edible share paired with an 85.05% YoY contraction and an 8.64% MoM decline indicates that Edible is currently a weak hedge, while the 8.56% YoY price decrease coinciding with a 31.31% 24-month sales contraction points to price-led defense that has not reversed share loss. This combination implies that defending rank 91 in New York will likely require rebalancing toward Topical’s faster MoM trajectory and selective Pre-Roll SKU rationalization to stabilize mix without deepening price compression.

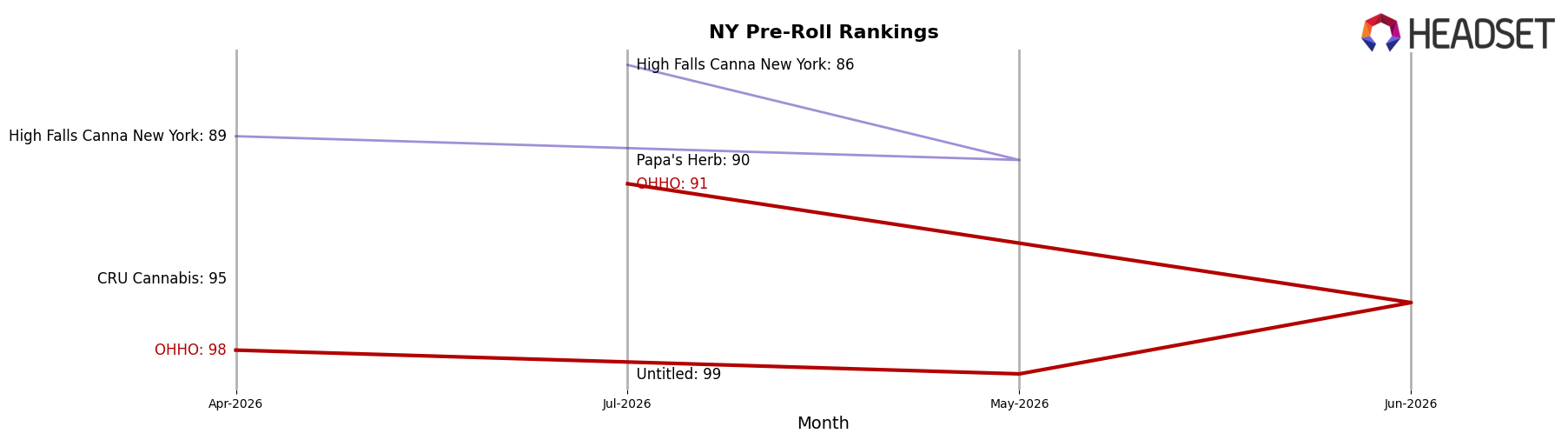

Competitive Landscape

OHHO ranks #91 in NY Pre-Roll in July 2026, down 36 positions from its peak of #36 in February 2025 and sliding 36 ranks since April 2026 when it sat at #55, while the year-over-year rank change from #55 to #91 marks a 65.5% deterioration in relative placement. Over the last three months OHHO moved from #98 to #91, a 7-rank improvement that still leaves it 88 positions behind category leader Ruby Farms at #1, and far outside the top 5 where Anthem climbed from #39 to #2 alongside a 877.2% year-over-year sales gain while Florist Farms held #4 with a 23.8% increase. The pattern of modest quarter-over-quarter recovery (+7 ranks) amid a year-over-year drop (-36 ranks) implies OHHO is stabilizing from a low base but ceding long-term share to faster-advancing competitors.

Notable Products

Durban Poison Pre-Roll 7-Pack (3.5g) posted the standout movement in July 2026 with a +96.4% month-over-month jump, climbing to rank 5, while Super Lemon Haze Pre-Roll 7-Pack (3.5g) fell -53.9% to rank 8. At the top, Super Lemon Haze Pre-Roll (0.5g) held rank 1 despite a -11.3% slide and OG Kush Pre-Roll (0.5g) dropped -14.8% at rank 4, indicating volatility within single sticks relative to multipacks. With nine of the top ten SKUs in the Pre-Roll category and a mix shift where a multipack surges as two single sticks retreat, the assortment is tilting toward value-oriented pack sizes that can buffer rank even when flagship singles soften.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.