Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

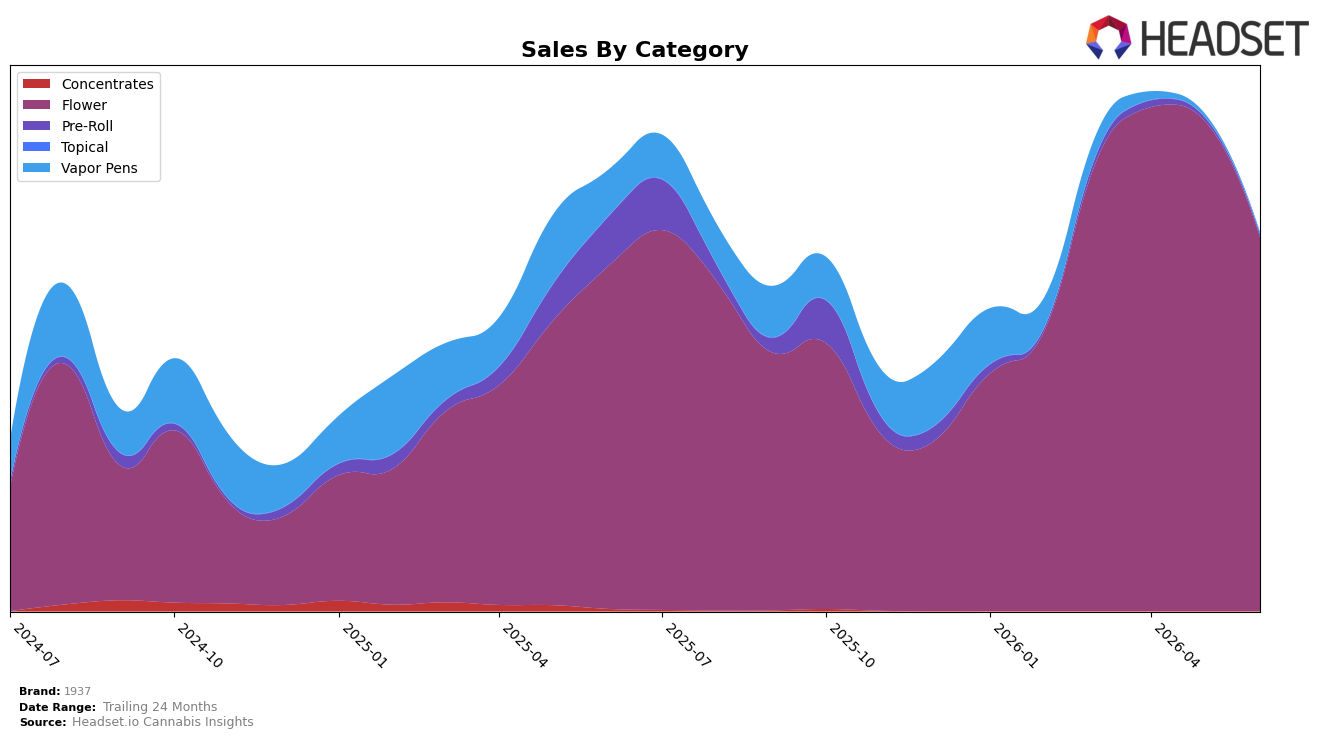

1937 is concentrated in Flower at 99.02% share with a June 2026 YoY sales change of 9.11% and a MoM decline of 23.75%, while Pre-Roll holds 0.59% share with YoY at -95.45% and MoM at -28.33%, and Vapor Pens sits at 0.39% share with YoY at -96.83% and MoM at -51.64%. Average price rose 10.20% YoY to $32.14 as Flower’s average price sits at $32.45, indicating mix inflation alongside a steep MoM pullback in smaller categories; together with a category rank of 16 in Flower in New York, this pattern implies a narrowed portfolio that is leaning into higher-priced Flower while rapidly exiting ancillary segments.

The shift toward a 99% Flower mix alongside Pre-Roll and Vapor Pens collapsing more than 95% YoY, combined with a 23.75% MoM contraction in Flower versus a 51.64% MoM drop in Vapor Pens, implies deliberate pruning that prioritizes share stability over breadth. With overall brand sales down 14.17% YoY but up 129.35% versus 24 months, and rank at 16 in Flower in New York, the trajectory suggests a scale-and-focus posture in a single category where price can carry margin, trading off diversification for defensibility in core Flower.

Competitive Landscape

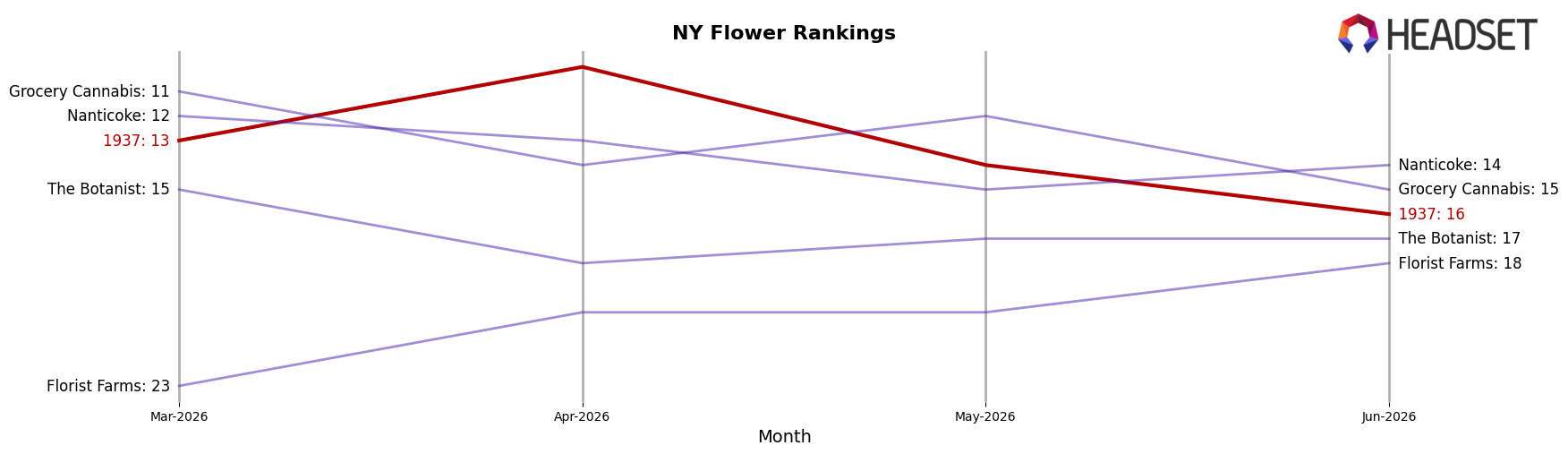

1937 sits at rank #16 in NY Flower for June 2026, down 2 positions year over year from #18 to #16 but slipping 3 spots since March 2026 from #13 to #16, while its peak at #10 in April 2026 marks a 6-rank fall into June; in contrast, Find. climbed from #3 to #1 as sales grew 35.6% year over year and RYTHM advanced from #10 to #5 on 40.6% YoY growth, whereas Dank. By Definition slipped from #1 to #3 with sales down 50.7%; taken together, 1937’s drop from #10 in April 2026 to #16 in June 2026 while competitors gain rank on double-digit sales growth implies share is being ceded to faster-rising leaders rather than cyclic volatility.

Notable Products

Blockberry Shake (7g) set the tone in June 2026 with a +24.8% month-over-month gain to rank 1, while the next nine SKUs lacked reported MoM movement despite holding ranks 2 through 10. With 10 of the top 10 positioned in Flower and two shake SKUs inside the top 10 (including rank 1 and rank 9), the mix tilts toward value-sized formats capturing volume at the expense of smaller pack differentiation. The $49,703 result at rank 1 alongside rank 3 and rank 5 holding without disclosed growth signals concentration risk: leadership is tied to one accelerating SKU while the broader lineup leans static. This pattern implies 1937 is consolidating around Flower scale plays, prioritizing high-turn Flower and shake formats over breadth expansion.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.