Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

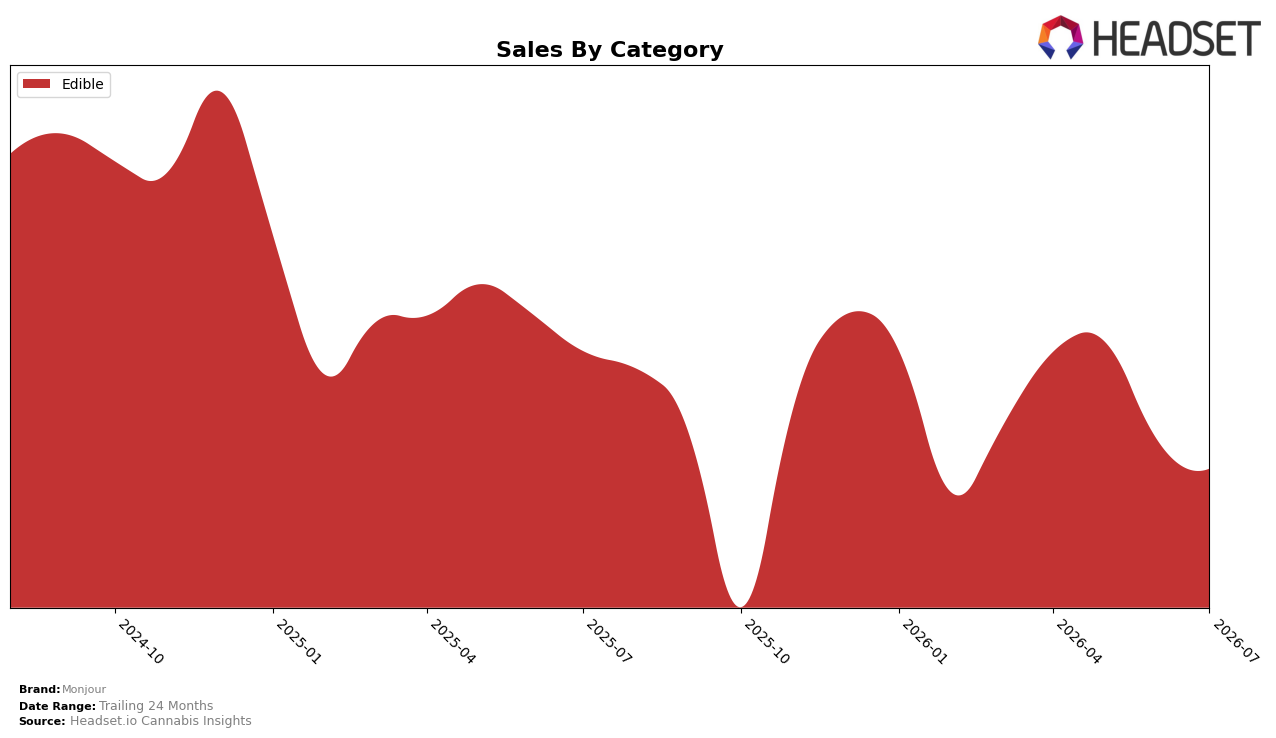

Monjour operated as a single-category brand in July 2026, with Edible accounting for 100.0% of sales and holding a rank of 7 in Edible in British Columbia. Within this mono-focus, year-over-year sales declined 11.1% while month-over-month sales slipped 2.8%, even as average price rose 12.6%, indicating mix and pricing are moving in opposite directions. The top market was ON, and the Edible concentration suggests limited cross-category buffering; the thesis is that a pure Edible mix magnifies sensitivity to price-led elasticity and seasonal MoM softness.

The combination of a 12.6% average price increase with a 11.1% year-over-year sales decline and a 2.8% month-over-month dip implies Monjour is trading margin per unit for volume within Edibles rather than expanding total demand. With a 24-month sales change of -23.9% alongside a stable 100.0% Edible share, the positioning tilts toward defending an Edible niche rather than diversifying into adjacent formats that could offset elasticity pressure. The thesis is that maintaining a single-category stance while prices rise requires sharper pack-size or subsegment targeting within Edibles to protect rank 7 momentum and reduce exposure to seasonal troughs.

Competitive Landscape

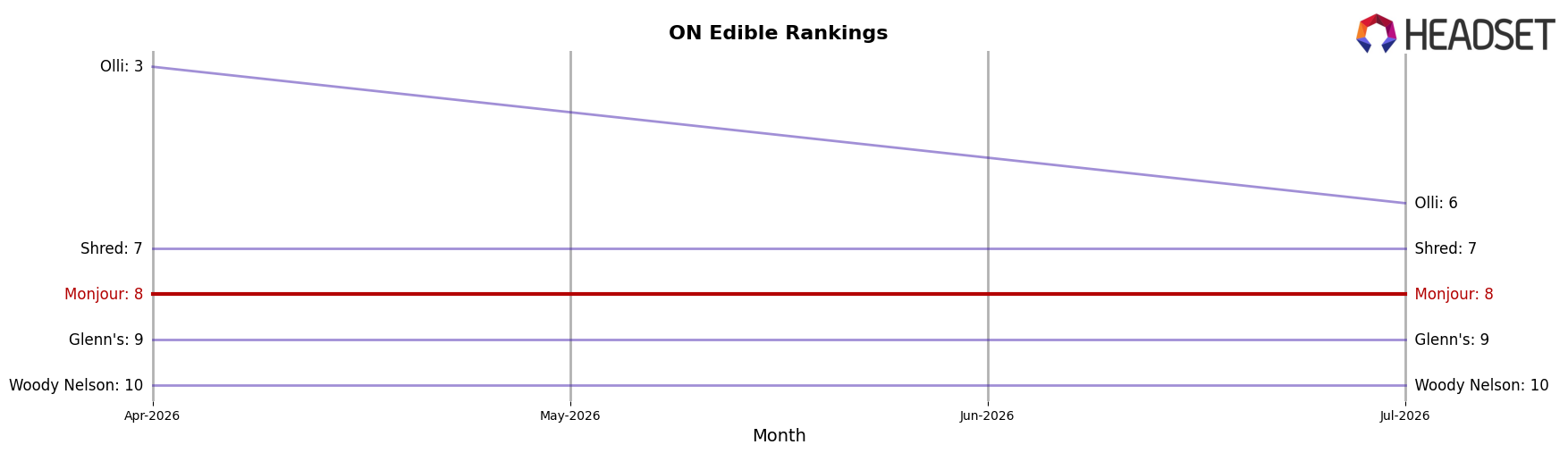

Monjour sits at rank #8 in ON Edible in July 2026, down 2 positions year over year from #6, and unchanged versus three months ago at #8; this stability below its January 2025 peak of #5 contrasts with competitors’ upward moves, as Wyld climbed from #4 to #3 while growing sales 13.7% year over year and No Future advanced from #5 to #4 with a 58.3% year-over-year increase. At the top end, Spinach held #1 with an 11.3% year-over-year sales gain, while mid-pack disruption is sharper as Fly North jumped from #15 to #5 on 611.5% year-over-year growth; taken together, Monjour’s 2-position year-over-year slide and flat 3-month rank signal share pressure from faster-rising rivals and imply a need to defend shelf presence as mobility accelerates above it.

Notable Products

CBD Orchard Medley Gummies 30-Pack (900mg CBD) posted the steepest decline at -27.7% MoM while dropping to rank 5, and CBD Me Time Mango Gummies 30-Pack (1500mg CBD) fell -18.1% MoM at rank 6; meanwhile, CBD Berry Good Day Gummies 5-Pack (100mg CBD) plunged -36.3% MoM at rank 8, indicating small-pack CBD formats are losing velocity despite occupying three ranks in the lower half. CBN:CBD:THC 8:3:1 Bedtime Blueberry Lemon Gummies 4-Pack (80mg CBD, 30mg CBN, 10mg THC) held rank 1 with +4.1% MoM and a $306,017 tally, while CBD Berry Good Day Gummy 30-Pack (600mg CBD) rose +5.8% MoM at rank 2; with all top-10 entries in Edibles and multiple CBD-only SKUs declining, the mix tilts toward multi-cannabinoid nighttime solutions over daytime CBD staples.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.