Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Originals is stocked at 236 licensed dispensaries across California and Massachusetts, 189 of them in California, with the deepest coverage in Los Angeles, Santa Ana, Corona, Long Beach, and San Bernardino. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

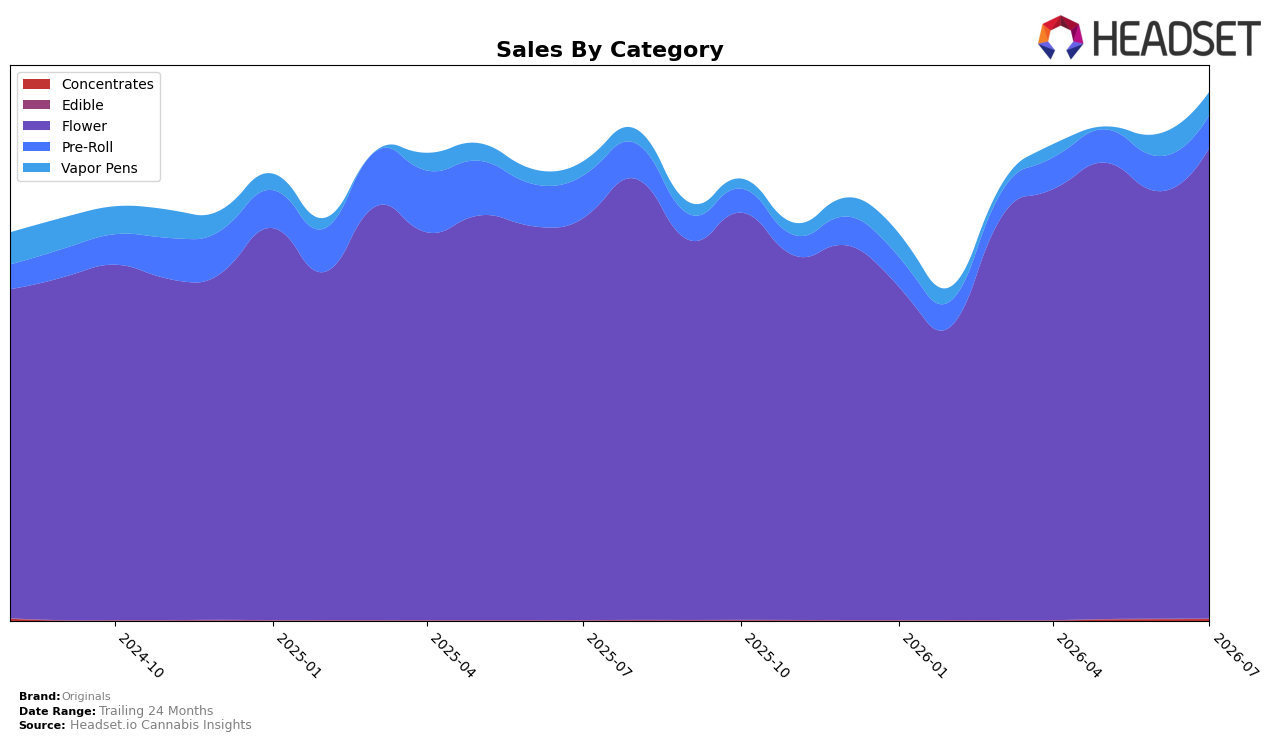

Originals concentrated 89.24% of July 2026 sales in Flower with year-over-year growth of 17.18% and month-over-month growth of 10.17%, while Pre-Roll slipped to 6.09% share with a -23.89% YoY decline and -7.38% MoM decline; Vapor Pens rose to 4.36% share on 67.14% YoY and 5.69% MoM growth, and Concentrates held 0.30% share with 10.85% MoM growth. Against an overall brand sales increase of 15.25% YoY and a -30.27% YoY drop in average price to $18.52, the mix implies that Flower volume expansion is carrying topline despite price compression, while Pre-Roll contraction and a small but rapidly growing Vapor Pens base are redistributing marginal share within the portfolio.

With Flower anchoring at 89.24% share and Originals ranked 19 in Flower in California, the 10.17% MoM growth there indicates the brand’s positioning remains volume-led in a price-sensitive segment, whereas the -7.38% MoM in Pre-Roll signals weaker repeat or assortment pull. The 67.14% YoY surge in Vapor Pens alongside only 4.36% share suggests a nascent entry point where incremental investment could diversify revenue without materially diluting Flower momentum, and the 10.85% MoM growth in Concentrates at 0.30% share indicates tests that can be scaled selectively if retention metrics improve.

Competitive Landscape

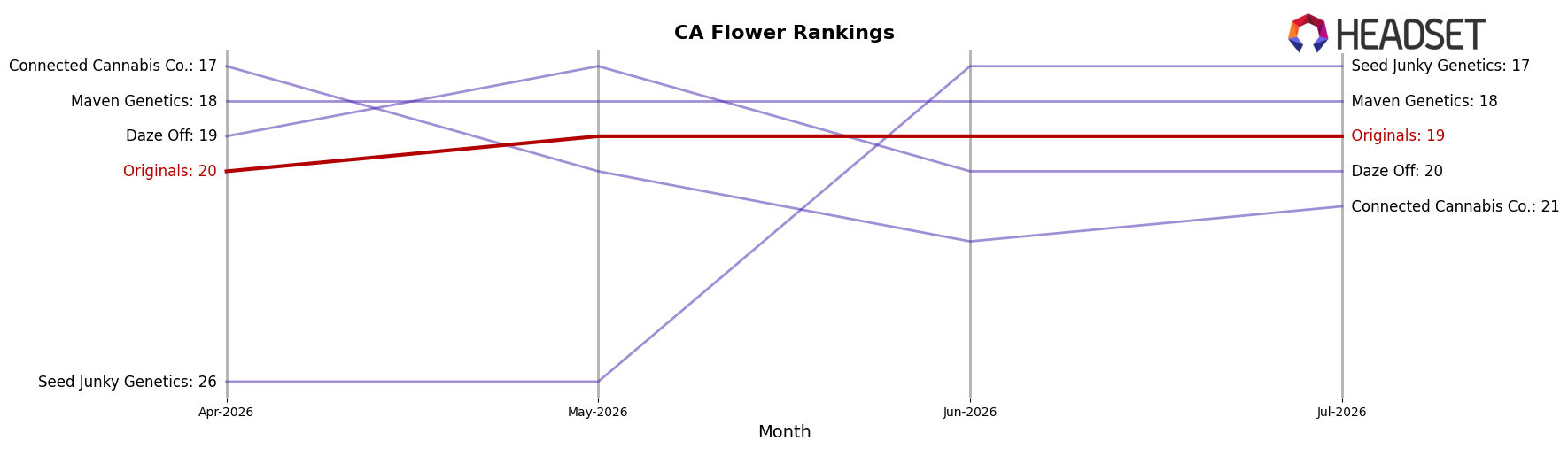

Originals sits at rank #19 in CA Flower in July 2026, improving 2 positions from #21 year over year, while moving 1 spot from #20 over the last three months; this coincides with a peak rank of #19 in July 2026 and a market context where STIIIZY advanced from #2 to #1 and CAM climbed from #4 to #3 as Claybourne Co. slipped from #3 to #5 with a -1.37% sales change. Originals’ modest rank gain of +2 YoY contrasts with STIIIZY posting +59.66% YoY sales and CannaBiotix (CBX) dropping from #1 to #2 despite +7.01% YoY sales, implying Originals’ trajectory is upward but pace-limited relative to leaders and will likely require either share capture from mid-pack brands or accelerated velocity to hold a top-20 foothold.

Notable Products

Oaksterdam (14g) posted the steepest movement in July 2026 with a -11.0% month-over-month decline at rank 10, while Gelato (3.5g) jumped 37.8% to hold rank 3; this split implies premium ounces are softening as select eighths gain traction. SFV OG (3.5g) held rank 1 with no reported month-over-month rate, and King Louis (3.5g) rose 16.4% at rank 2, while Flower accounted for all top-10 SKUs, concentrating demand into a single category with both eighths in the top 3 and multiple 14g formats in ranks 6–10. Originals OG (14g) at rank 6 and SFV OG (14g) at rank 8 contrasted the decline of Oaksterdam (14g), indicating format performance is now strain-specific rather than size-led, despite Oaksterdam (14g) still clearing $105,919. The pattern points to a mix shift toward a few momentum eighths anchoring the leaderboard while only select 14g strains maintain velocity, guiding assortment toward depth in top eighth strains and tighter curation of ounce formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.