Where to Buy

Yada Yada is stocked at 169 licensed dispensaries across California, with the deepest coverage in Sacramento, San Diego, La Mesa, Los Angeles, and Stockton. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

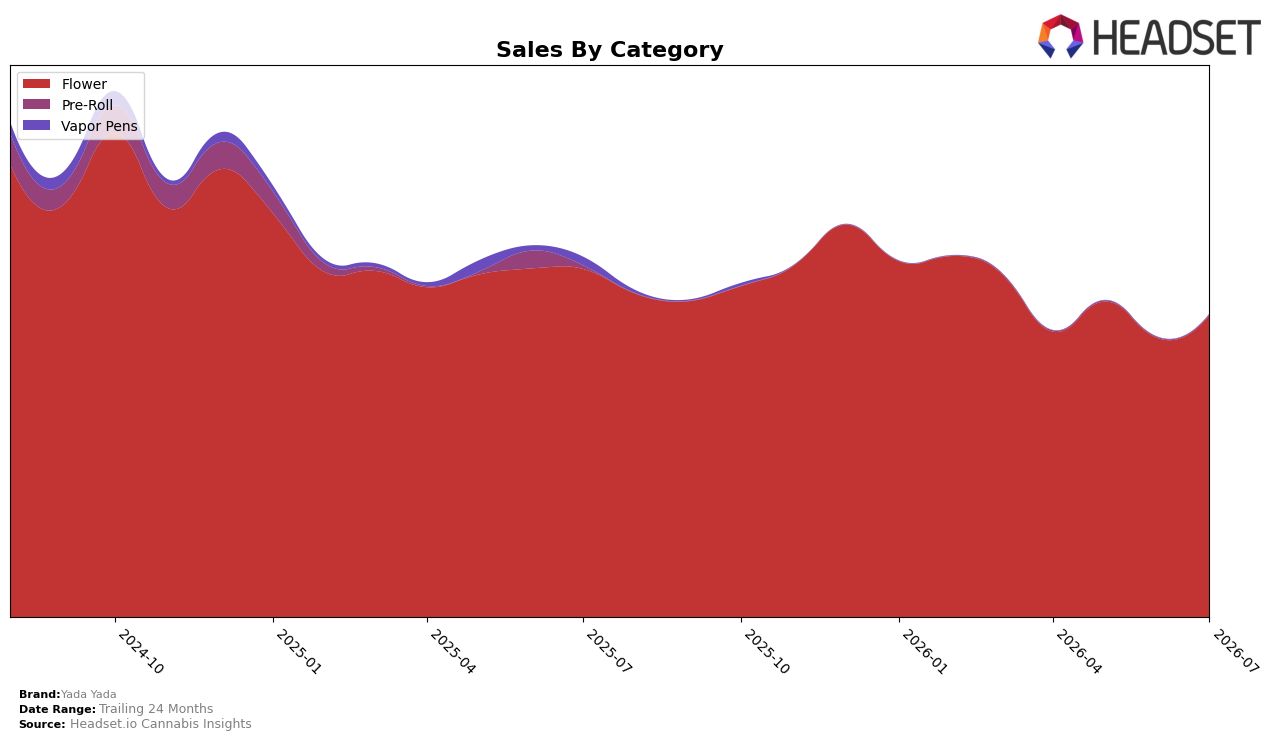

Yada Yada concentrated 99.81% of July 2026 sales in Flower with a 28th rank in Flower in California, while Pre-Roll held just 0.19% share; within that mix, Flower declined 13.22% YoY but grew 8.33% MoM, and Pre-Roll fell 82.61% YoY yet rose 17.14% MoM. Against a brand-level sales decline of 15.81% YoY and a 2.79% YoY drop in average price to $17.39, the heavy Flower reliance made category-level swings disproportionately impact totals; the pattern implies reliance on Flower volatility is driving aggregate contraction despite short-term MoM lift.

The divergence between a broad 24‑month sales contraction of 40.04% and July 2026 MoM gains concentrated in Flower (8.33% MoM) and a small Pre-Roll base (17.14% MoM on 0.19% share) indicates mix fragility rather than durable diversification; holding the 28th position in California Flower while pricing slid 2.79% YoY implies price-led defense instead of assortment-led expansion. This pattern implies that maintaining rank will depend on stabilizing Flower while selectively scaling Pre-Roll from a low base to dilute category risk without eroding price further.

Competitive Landscape

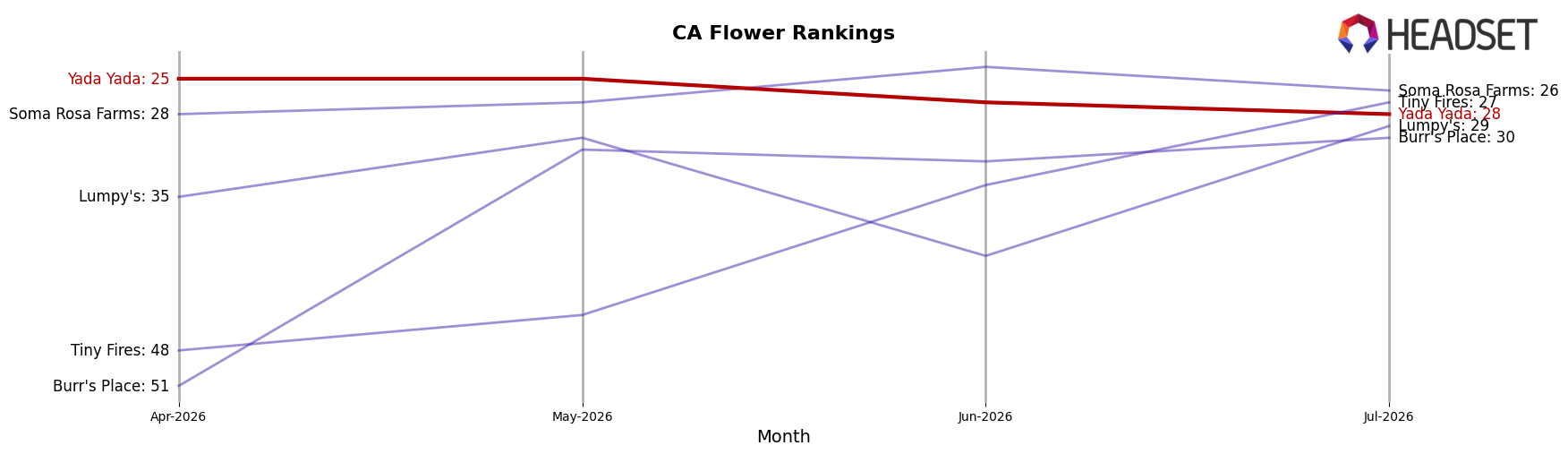

Yada Yada sits at #28 in CA Flower in July 2026, down 6 spots year over year from #22 and 3 spots since April 2026 when it was #25, after peaking at #19 in February 2026. In contrast, STIIIZY climbed from #2 to #1 with 59.7% YoY sales growth while CAM rose from #4 to #3 on 52.2% YoY growth, indicating category leaders are consolidating share as Yada Yada loses rank positions; the pattern implies Yada Yada’s trajectory is drifting from mid-tier toward lower-tier unless rank stabilization reverses the 6-position YoY decline.

Notable Products

GovernMint Oasis Smalls (20g) posted the steepest decline in July 2026 with -28.2% MoM while dropping to rank 5, and GMO Shake (14g) fell -36.4% MoM at rank 9, indicating a pullback in value-oriented formats. In contrast, Black Amber Pre-Ground (14g) rose +15.2% MoM to hold rank 1 and Glitter Bomb Pre-Ground (14g) climbed +37.8% MoM at rank 2, showing momentum concentrated at the very top. With eight of the top ten being Flower SKUs and pre-ground variants occupying two of the top three spots, the mix implies Yada Yada is tilting toward convenience-led Flower while de-emphasizing lower-yield shake and certain Smalls despite one mid-tier item still clearing $52,754.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.