Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

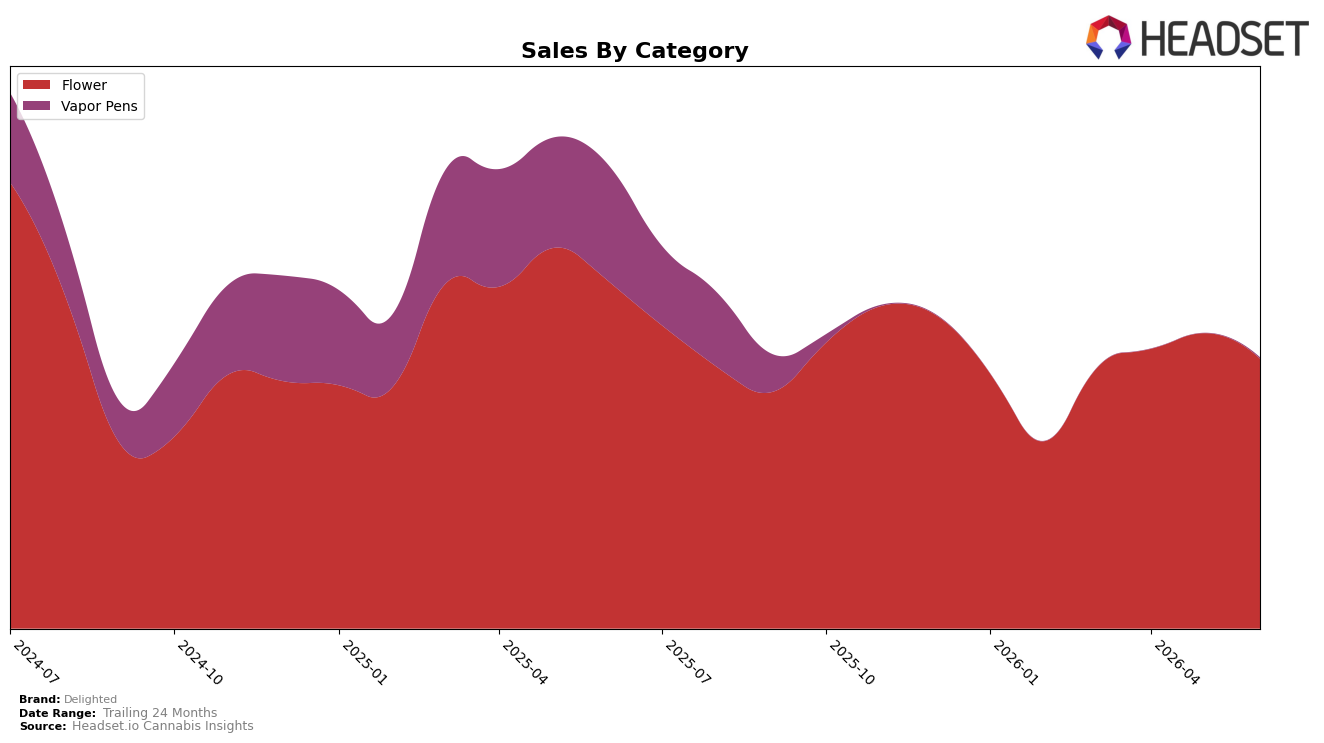

In June 2026, Delighted concentrated 99.60% of sales in Flower while Vapor Pens fell to 0.40% share, indicating a narrowed mix as Flower declined 22.39% year over year and 8.65% month over month. Vapor Pens posted a 99.07% year-over-year drop with no measurable month-over-month trend, and average price declined 13.63% year over year to $22.25, pulling category revenue density lower despite a 21st rank in Flower in California. The pattern implies Delighted is effectively a single-category player in June 2026, with exposure concentrated in a shrinking Flower base and minimal diversification to offset volatility.

With a 41.57% brand sales decline year over year alongside a 22.39% Flower contraction and a 13.63% price reduction, Delighted’s value-led pricing has not translated into volume defense at the 21st rank in California Flower. The 0.40% share contribution from Vapor Pens and a 99.07% year-over-year plunge in that segment limit cross-category traffic capture, while an 8.65% month-over-month Flower dip compounds positioning risk against peers migrating mix to adjacent inhalables; the implication is that Delighted’s current stance optimizes for simplicity but trades away resilience, making incremental share recovery contingent on either stabilizing Flower velocities or reintroducing a viable second pillar.

Competitive Landscape

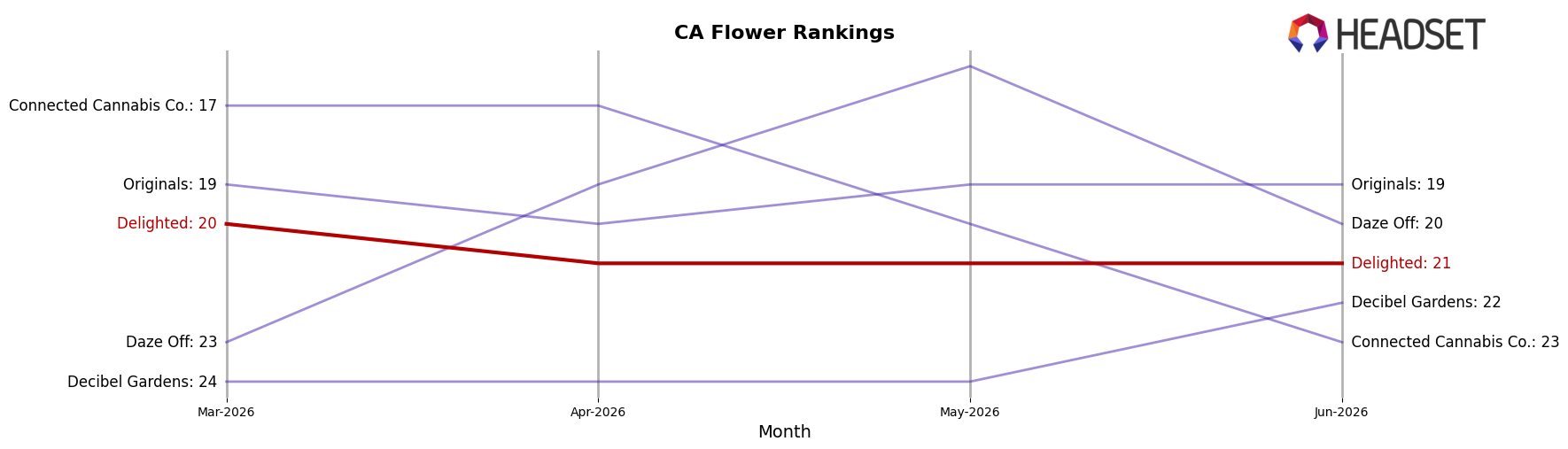

Delighted sits at rank #21 in California Flower in June 2026 after sliding 4 positions year over year from #17, and dipping 1 spot since March 2026 from #20, while its peak of #17 in June 2025 marks a 4-rank retreat from last year’s high. In contrast, STIIIZY advanced from #2 to #1 alongside a 62.5% year-over-year sales increase, and CAM climbed from #3 to #2 with 56.2% growth, whereas CannaBiotix (CBX) fell from #1 to #3 despite a 2.4% lift. The combination of a 4-position year-over-year slippage and a 1-position three-month drift implies Delighted’s trajectory is tilting toward mid-pack erosion unless rank stability is recovered against faster-rising leaders.

Notable Products

Blue Lobster (3.5g) posted the sharpest movement in June 2026 with a 61.6% month-over-month gain and climbed into rank 4, while Zowah Diesel (3.5g) fell 21.5% and sat at rank 6. Runtz (3.5g) held rank 1 with a 26.1% increase as Traffic Stopper (3.5g) stayed close at rank 2 with a 16.6% lift, indicating the top tier is widening its lead over mid-pack SKUs that slipped by 11.5% to 21.5%. Four of the top ten are Runtz-family or closely named variants, and Flower accounts for all top-10 slots, pointing to a concentration strategy that favors a few fast-moving 3.5g strains over breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.