Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

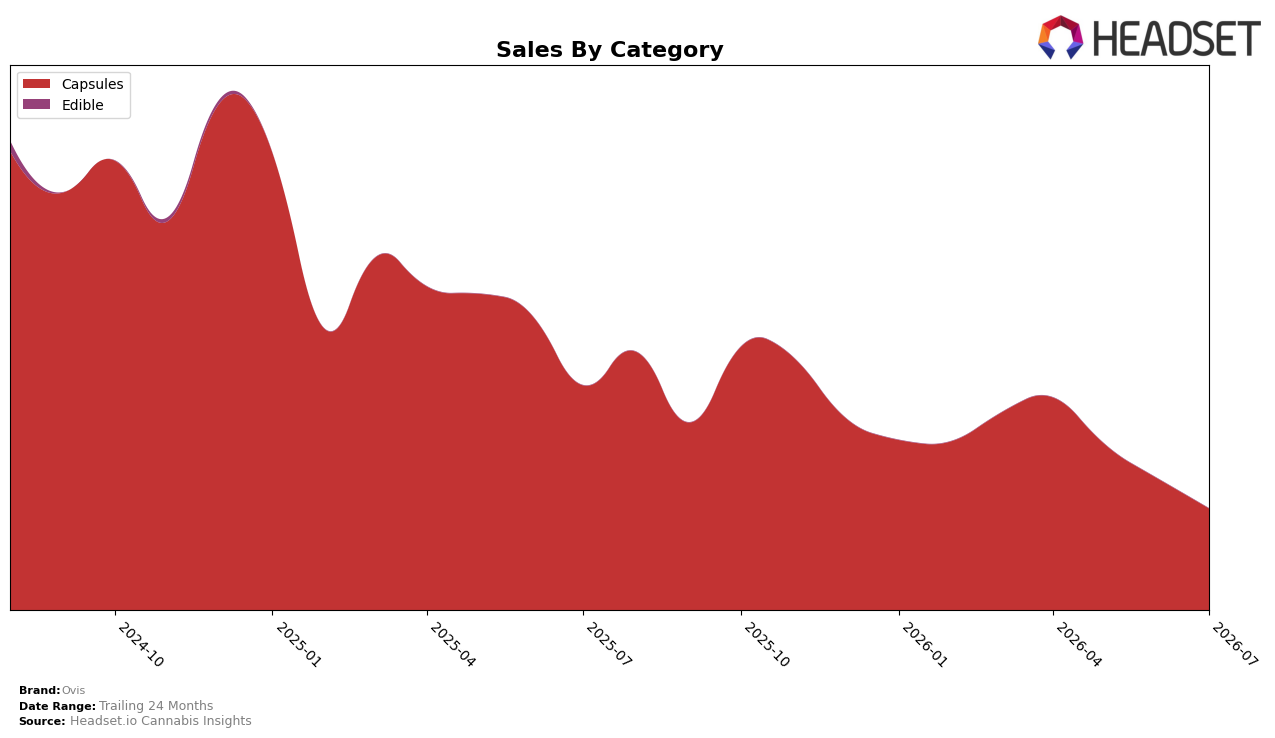

In July 2026, Ovis concentrated 100.0% of sales in Capsules, with year-over-year sales down 54.9% and month-over-month down 22.9%. Average price rose 9.0% YoY to $18.05, while share breadth across categories contracted to a single line, implying price mix did not offset volume losses. With no rank reported for Capsules in Alberta, the category-only footprint and double-digit MoM decline signal a contraction phase rather than seasonal volatility.

The shift to a 100.0% Capsules mix alongside a 54.9% YoY decline and a 22.9% MoM slide suggests Ovis is overexposed to a shrinking niche where demand elasticity may be biting despite a 9.0% price increase. The absence of a rank in Alberta and a 71.2% 24-month sales decline indicate positioning drift toward a long-tail presence, where maintaining a single-category focus concentrates risk and reduces optionality for recovery.

Competitive Landscape

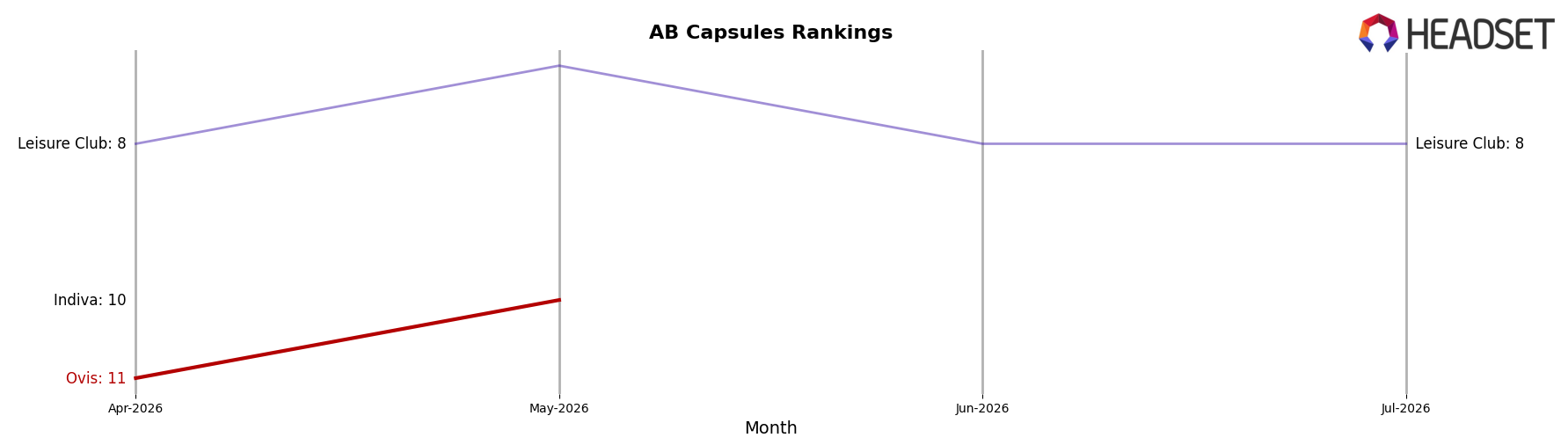

Ovis sits at #11 in AB Capsules for July 2026, down 1 position year over year from #10, and flat versus three months ago at #11, indicating a stall below its peak of #7 from April 2025; meanwhile, Tweed held #1 year over year at #1 despite a -3.34% sales change, and Glacial Gold stayed at #2 with a -23.03% sales change, while Emprise Canada climbed from #4 to #3 and Stigma Grow fell from #3 to #5 alongside a -74.37% sales change; this pattern implies Ovis’s rank trajectory has plateaued in the lower tier, with competitor churn above it creating openings that require conversion to regain a top-10 position.

Notable Products

THC Softgel 30-Pack (300mg) posted the largest month-over-month gain at 111.6%, yet it only reached rank 5 while THC Softgel 15-Pack (150mg) fell 34.5% and still held rank 1. CBD Softgels 30-Pack (1500mg CBD) climbed 90.5% but stayed at rank 5 alongside the THC Softgel 30-Pack (300mg), and Blue THC Softgel 50-Pack (125mg) slid 13.0% at rank 3. With all top ten positions occupied by Capsules and two rank-5 SKUs surging on volume despite lower ladder positions, the mix points to price-pack experimentation expanding unit throughput while leadership consolidates around fewer, higher-velocity capsule formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.