Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

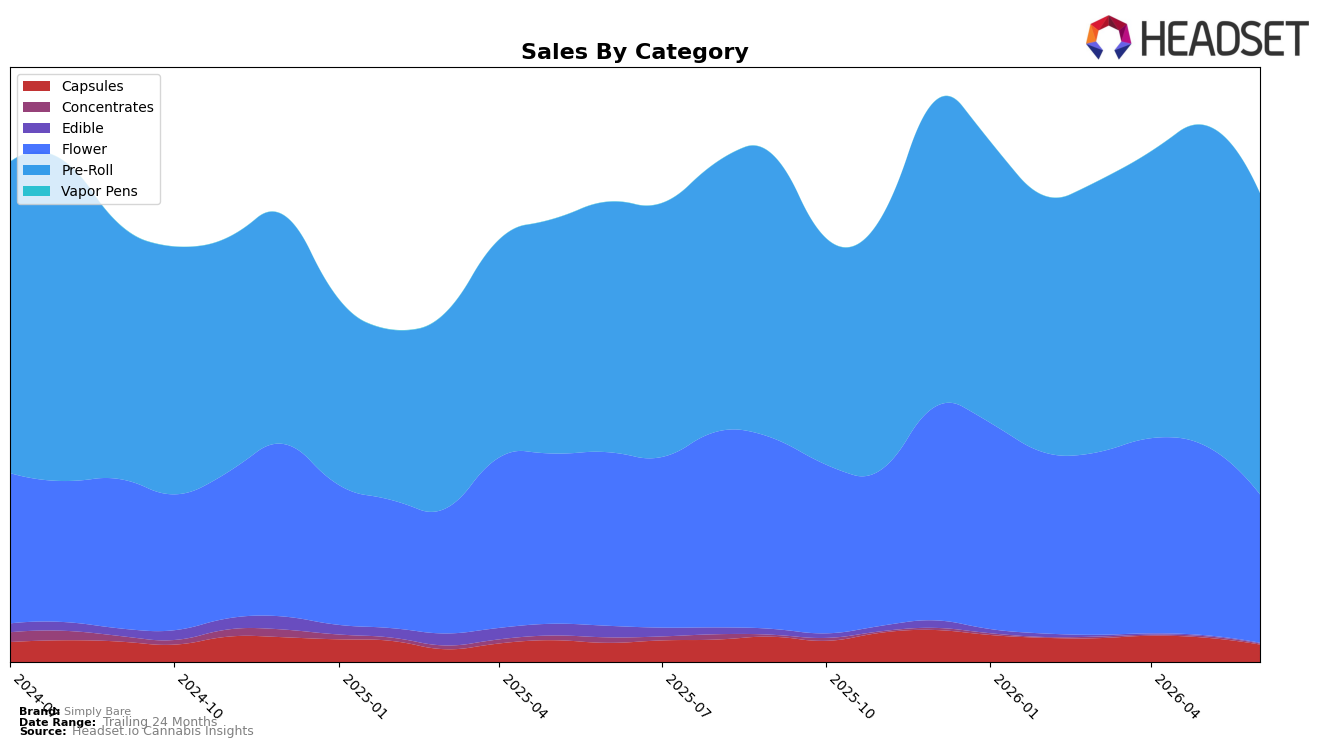

In June 2026, Simply Bare’s mix tilted further toward Pre-Roll at 64.35% share with year-over-year growth of 20.26% but a month-over-month decline of 5.96%, while Flower held 31.67% share with a 14.55% YoY contraction and a sharper 21.83% MoM drop; Capsules contributed 3.73% share, down 8.93% YoY and 28.50% MoM. Long-tail categories contracted steeply, with Concentrates at 0.15% share falling 86.70% YoY and 39.04% MoM, and Edible at 0.10% share down 95.76% YoY and 28.33% MoM; combined with an 11.44% YoY decline in average price to $20.44, these shifts indicate volume concentration in lower-priced Pre-Roll while premium segments retreat. The pattern implies Simply Bare is consolidating around Pre-Roll scale in ON while ceding breadth in Flower and micro-categories, prioritizing share defense in a value-leaning basket over diversification.

The category pivot raises positioning trade-offs: Pre-Roll growth of 20.26% YoY alongside a 5.96% MoM dip suggests momentum exists but is sensitive to monthly price or assortment moves, whereas Flower’s 14.55% YoY and 21.83% MoM declines risk eroding premium perception if left unaddressed. With total brand sales up 1.85% YoY but down 3.95% over 24 months, and Capsules shrinking 28.50% MoM while Concentrates fell 39.04% MoM, the brand is increasingly defined by one high-volume format rather than a balanced portfolio. The implication is a volume-led, price-flexed stance anchored in Pre-Roll that can support near-term share but may compress elasticity headroom in premium Flower unless assortment and pricing are recalibrated to rebalance mix quality.

Competitive Landscape

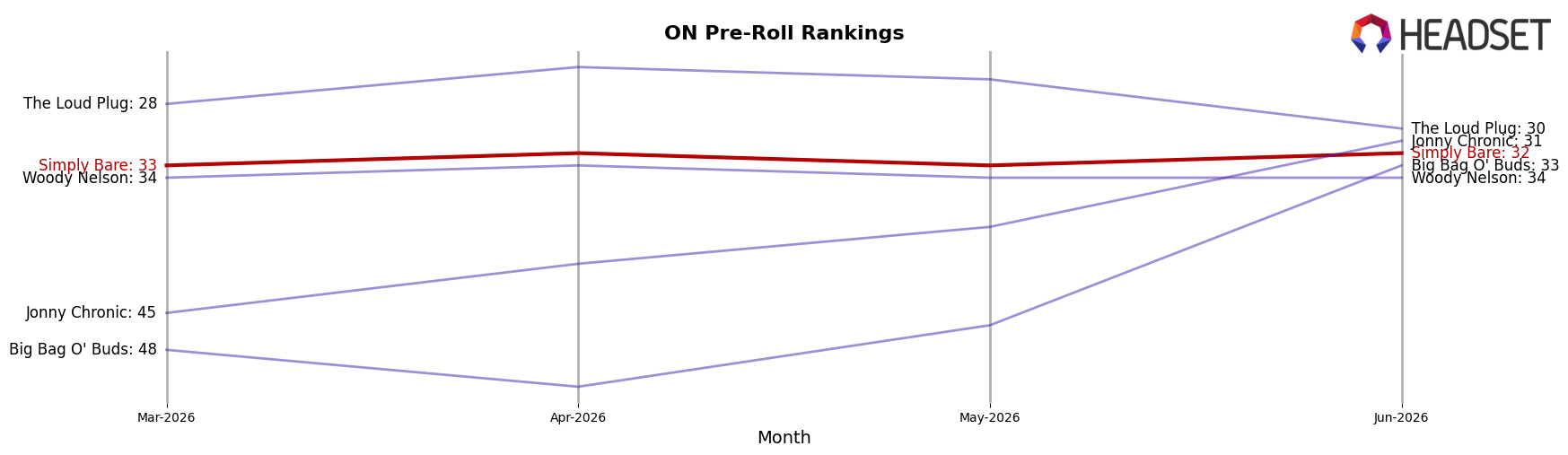

Simply Bare ranks #32 in ON Pre-Roll in June 2026, improving 1 place from #33 year over year, while also edging up 1 rank from March 2026’s #33; by contrast, Back Forty / Back 40 Cannabis climbed from #3 to #1 with a 74.6% YoY sales increase and Jeeter slid from #2 to #4 with a 48.5% YoY decline, reshuffling the top tier ahead of the #32 position. Against its own history, Simply Bare is still below its #29 peak from November 2025 and has moved just 1 rank over 12 months, whereas General Admission fell from #1 to #2 alongside a 17.9% YoY sales contraction and Thumbs Up Brand rose from #8 to #3 with 53.6% YoY growth, indicating that Simply Bare’s marginal rank gain amid volatile top-5 churn points to stable but capped momentum unless product or distribution changes re-accelerate share.

Notable Products

BC Organic - Tangerine Sunrise Pre-Roll (0.5g) posted the standout move in June 2026 with a +180.5% month-over-month surge to rank 2, while the top-ranked BC Organic Fruit Loopz Pre-Roll (0.5g) fell -16.8% and the Fruit Loopz Pre-Roll 5-Pack (1.5g) at rank 3 declined -28.1%. Four of the top ten are Fruit Loopz family SKUs across single, 5-pack, and 10-pack formats, yet only the single-pack leader sits at rank 1 as the 5-pack contracted and the 10-pack’s rank 10 position suggests volume is spreading across formats rather than concentrating. The mixed shifts within Pre-Roll—ranging from -17.2% on BC Organic - Fire OG Rosin Infused Pre-Roll (0.5g) at rank 7 to +18.6% on BC Organic Pink Drip Pre-Roll (0.5g) at rank 8—imply shoppers are trading into faster-turn singles while larger packs give back share. The pattern points to a pivot toward single-serving novelty and flavor-led SKUs, indicating Simply Bare’s commercial direction is tilting from bulk multipacks toward high-velocity singles anchored by breakout strains like Tangerine Sunrise.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.