May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

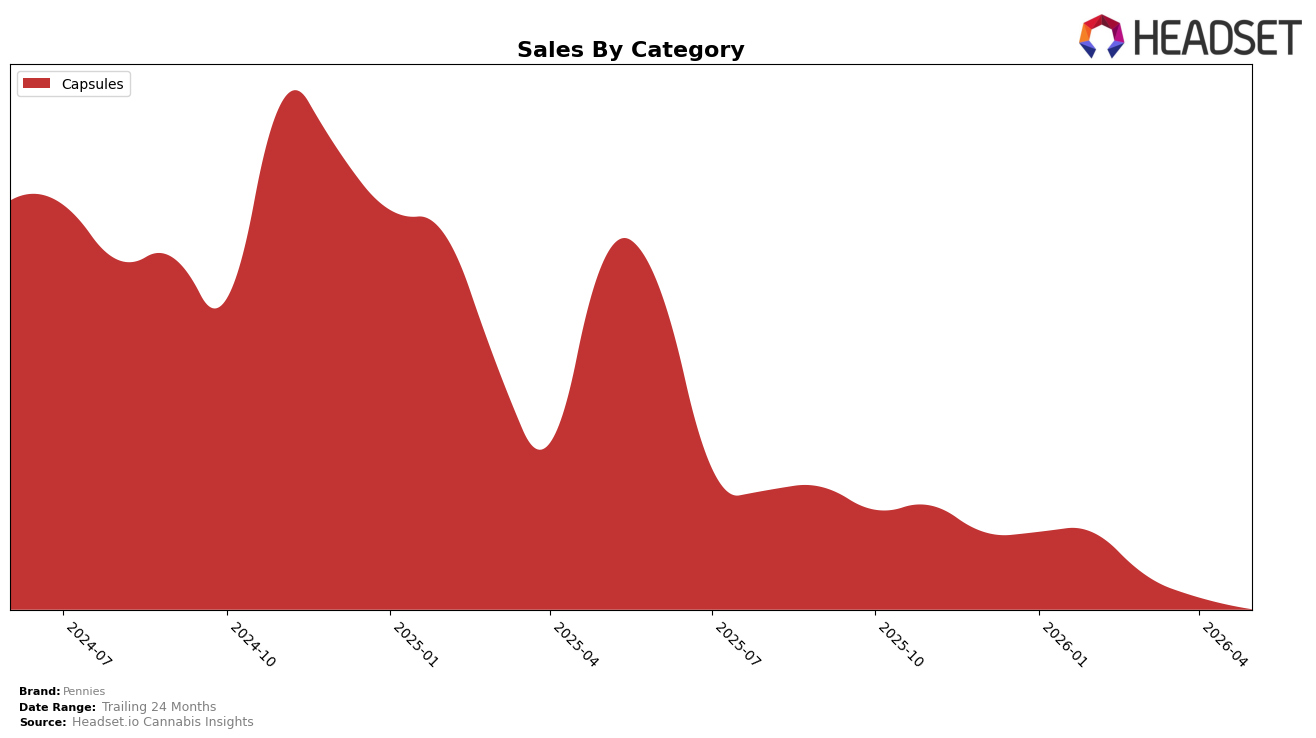

In May 2026, Pennies operated as a single-category brand with Capsules at 100.0% category mix share, paired with a year-over-year sales change of -89.28% and a month-over-month change of -22.02%. Average price moved down 14.79% YoY to $11.71, while the Capsules category itself carried the full portfolio weight at 100.0% share and the same -89.28% YoY trajectory, indicating concentrated exposure without cross-category offsets. With no rank reported for Capsules in Ontario, the combination of a full reliance on one category and double-digit price compression implies that demand elasticity did not convert into volume recovery, and the one-channel footprint amplified volatility rather than cushioning it.

The shift toward a single-category focus and a 22.02% MoM drop alongside a 14.79% YoY price decline suggests Pennies is competing on price without sufficient differentiation to stabilize unit throughput, as a 100.0% category mix leaves no diversification to buffer cyclical swings. Given an -89.28% YoY sales contraction concentrated entirely in Capsules and an absent rank signal in Ontario, the brand’s positioning has migrated from a multi-pronged portfolio to a niche bet where pricing levers have limited impact, implying a need to either reintroduce mix breadth or reposition Capsules on attributes other than discounting to restore share velocity.

Competitive Landscape

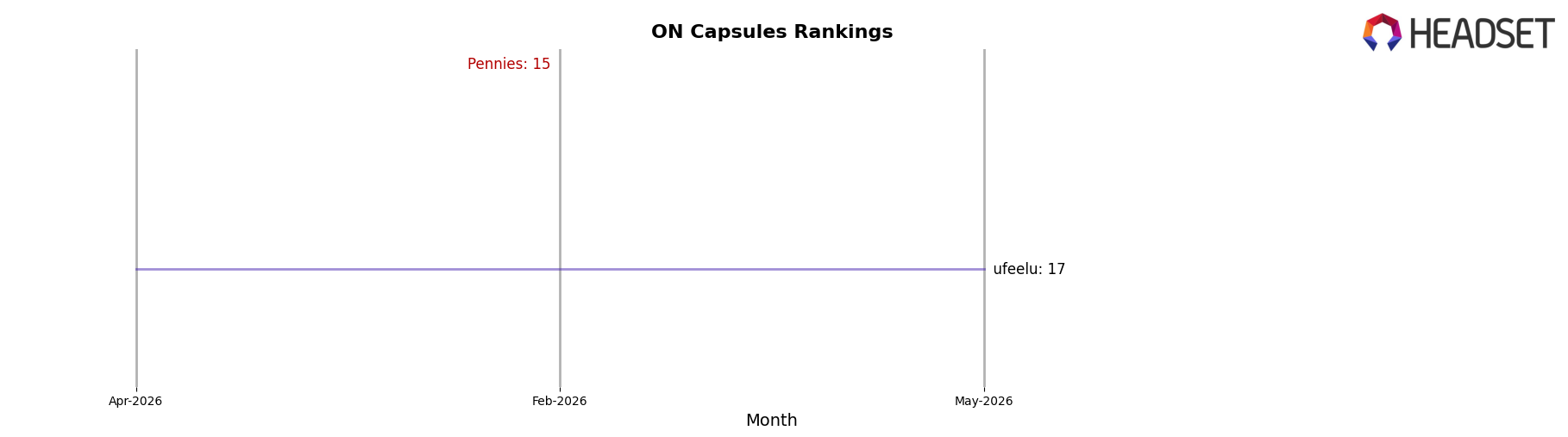

Pennies sits at #21 in ON Capsules in May 2026, down 10 places year over year from #11, and 6 places below its February 2026 position of #15; compared with its peak of #11 in June 2025, the brand has slid 10 ranks while category leaders moved differently, as Aspire held #1 from last year to #1 now and Glacial Gold climbed from #4 to #2 with a 39.1% YoY sales change. Against that backdrop, Redecan stayed flat at #3 despite a 36.7% YoY sales decline and Tweed fell from #2 to #5 with a 47.4% YoY drop, indicating Pennies’ rank erosion is not purely category-wide pressure but a brand-specific loss of relative momentum that, if unaddressed, implies further mid-pack drift rather than a return to its June 2025 peak.

Notable Products

THC Softgels 5-Pack (50mg) led the downturn in May 2026 with a -45.6% month-over-month decline while holding rank 1, indicating volume outpaced by prior months despite a top placement; by contrast, THC Plus Softgels 20-Pack (200mg) rose +17.7% MoM at rank 2, narrowing the gap in placement but not enough to offset the category swing. With both top-2 SKUs in Capsules, the concentration suggests Pennies’s reliance on format-specific demand magnifies volatility, implying the brand’s commercial direction leans on capsule-led penetration that may require mix diversification to stabilize performance.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.