Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Phat Panda is stocked at 289 licensed dispensaries across Washington, Massachusetts, and 2 other states, 231 of them in Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Vancouver, and Bellingham. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

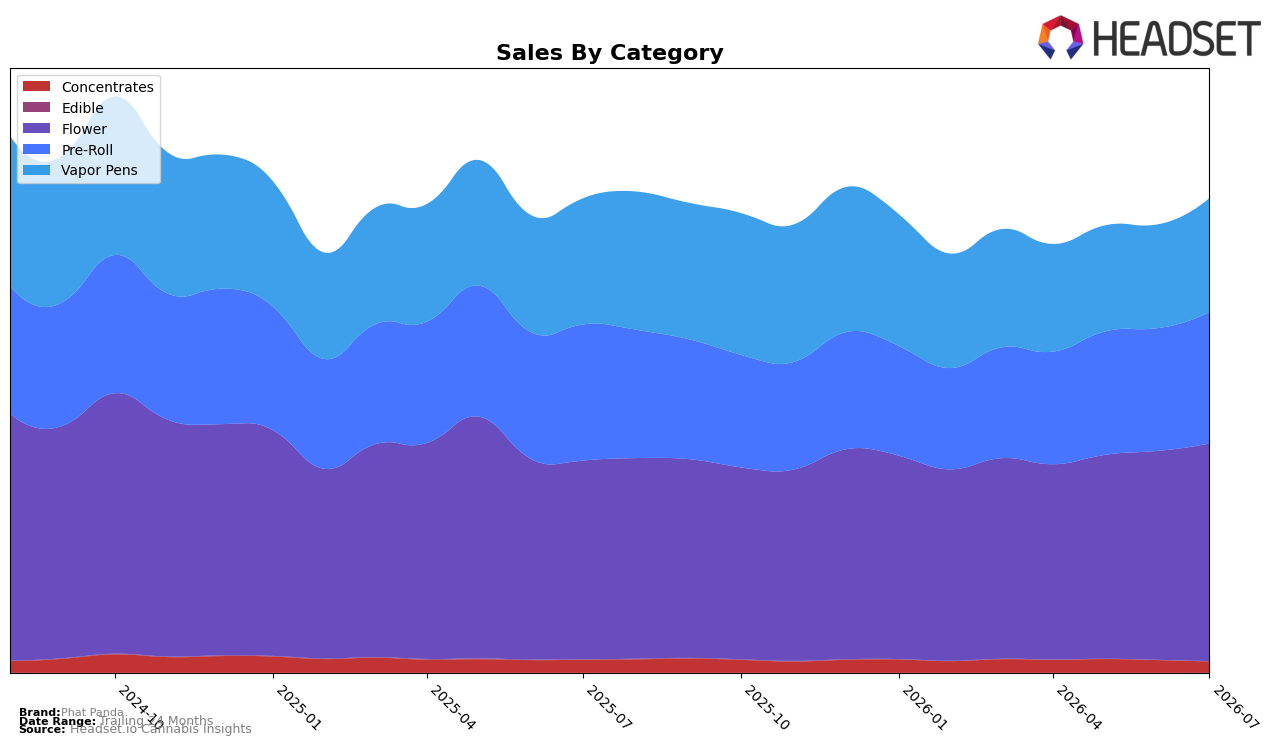

Phat Panda’s July 2026 category mix tilts toward Flower at 45.88% share with year-over-year growth of 9.52% and month-over-month growth of 4.14%, while Vapor Pens hold 24.04% share but decline year-over-year by 9.59% despite a 9.93% month-over-month lift; Pre-Roll sits at 27.68% share, down 3.53% year-over-year but up 7.03% month-over-month. Concentrates account for 2.37% share with a 13.11% year-over-year drop and an 11.02% month-over-month decline, and Edible is 0.04% share with a 45.21% year-over-year contraction countered by a 121.94% month-over-month spike. With Flower ranked 1 in Washington, these mixed trajectories imply the brand’s overall 3.56% year-over-year sales gain is anchored by Flower’s stability and near-term recovery in Pre-Roll and Vapor Pens rather than breadth across smaller formats.

The combination of a 4.47% year-over-year decline in average price alongside month-over-month volume gains in Vapor Pens (9.93%) and Pre-Roll (7.03%) suggests Phat Panda is leaning into price-accessible formats while defending premium-equity in Flower with a 9.52% year-over-year rise and rank 1 positioning in Washington. Concurrent contraction in Concentrates (down 13.11% year-over-year and 11.02% month-over-month) and ultra-niche Edible share (0.04% despite a 121.94% month-over-month rebound) indicates a focused portfolio where leadership in Flower and tactical pricing in inhalables drive share retention, implying the brand’s positioning prioritizes scale and velocity in core inhalables over diversification into small, volatile categories.

Competitive Landscape

Phat Panda holds rank #1 in Washington Flower in July 2026, unchanged YoY from rank #1, while maintaining rank #1 over the last three months; in contrast, Legends sits at #2 with a -22.9% YoY sales decline from its #2 position, and Lifted Cannabis Co advanced from #8 to #3 on +13.1% YoY sales as Sweetwater Farms jumped from #14 to #5 on +48.2% YoY sales; the pattern implies Phat Panda’s steady #1 rank amid upward mobility from #8→#3 and #14→#5 contenders signals durability at the top but narrowing separation if challenger momentum persists.

Notable Products

Bangers - Granddaddy Purple Pre-Roll 2-Pack (1g) posted the standout movement in July 2026 with a +36.5% month-over-month rise to rank 5, while OG Chem Pre-Roll (1g) held rank 1 with a smaller +7.4% gain that suggests leadership is stable but not accelerating. Platinum - Trophy Wife Pre-Roll (1g) slipped -4.2% at rank 2 as Bangers - Golden Pineapple Pre-Roll 2-Pack (1g) advanced +15.6% at rank 3, indicating momentum shifting toward value-oriented two-packs over single sticks. With eight of the top ten in Pre-Roll and the lone Flower entry, Platinum - Golden Pineapple (3.5g), up +8.0% at rank 10 on $109,546, the mix concentrates consumer spend in Pre-Roll formats while Flower holds a supporting role. The pattern implies Phat Panda is tilting assortment and promotions toward multi-pack Pre-Rolls to defend share at the top while using selective Flower SKUs to anchor price perception.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.