Where to Buy

Punch Bowl is stocked at 115 licensed dispensaries across Oregon, with the deepest coverage in Portland, Eugene, Bend, Salem, and Beaverton. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

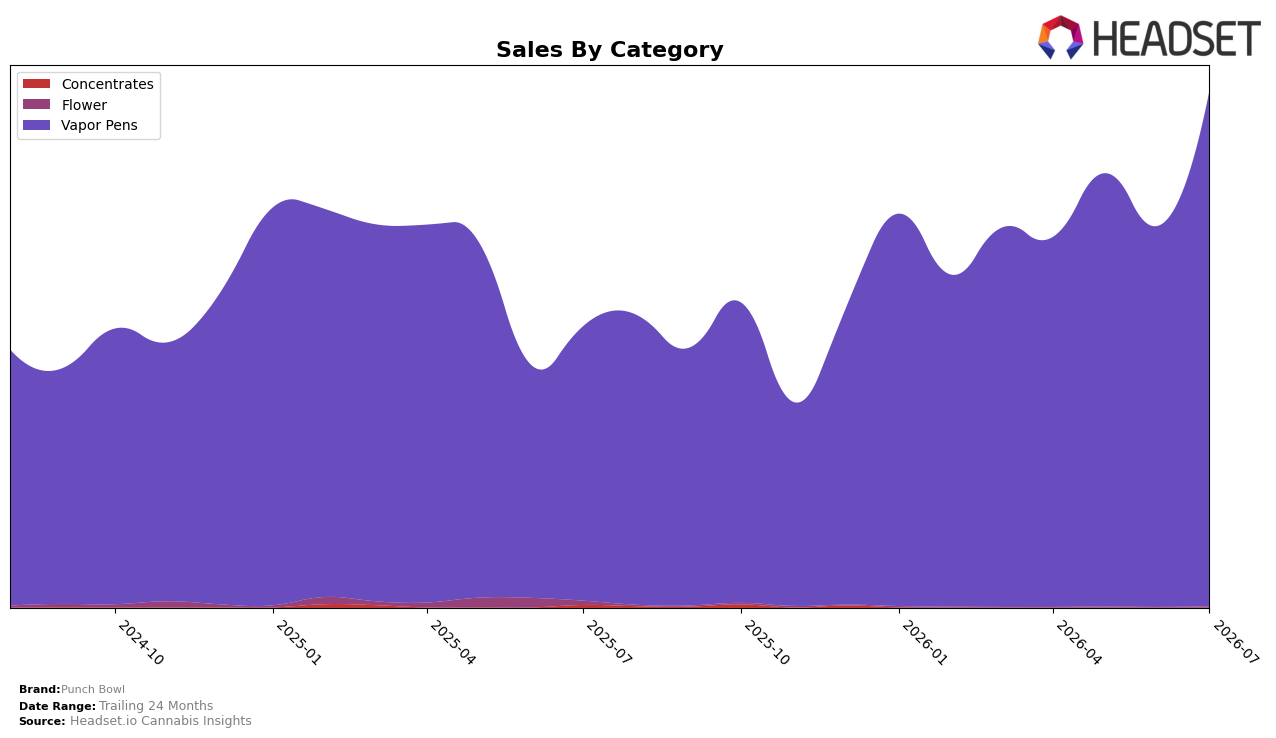

In July 2026, Vapor Pens accounted for 99.87% share while Flower held 0.13%, with Vapor Pens up 87.98% year over year and 35.34% month over month, versus Flower down 81.78% year over year and effectively flat month over month due to negligible base. Brand-wide sales rose 84.01% year over year alongside a 4.98% average price decline, indicating volume-led growth concentrated in Vapor Pens and a retrenchment from Flower; the implication is that Punch Bowl is consolidating around one category where scale and pricing elasticity are currently favorable.

With Vapor Pens at a 99.87% mix and ranked 19 in Oregon for Vapor Pens, the 35.34% month-over-month acceleration paired with a 4.98% price dip suggests a deliberate trade-off toward velocity over margin in July 2026. Given 84.01% year-over-year brand growth against an 81.78% Flower decline, the pattern implies Punch Bowl is prioritizing penetration and shelf throughput in Vapor Pens to climb from rank 19 while treating Flower as a minimal, possibly experimental SKU set rather than a growth vector.

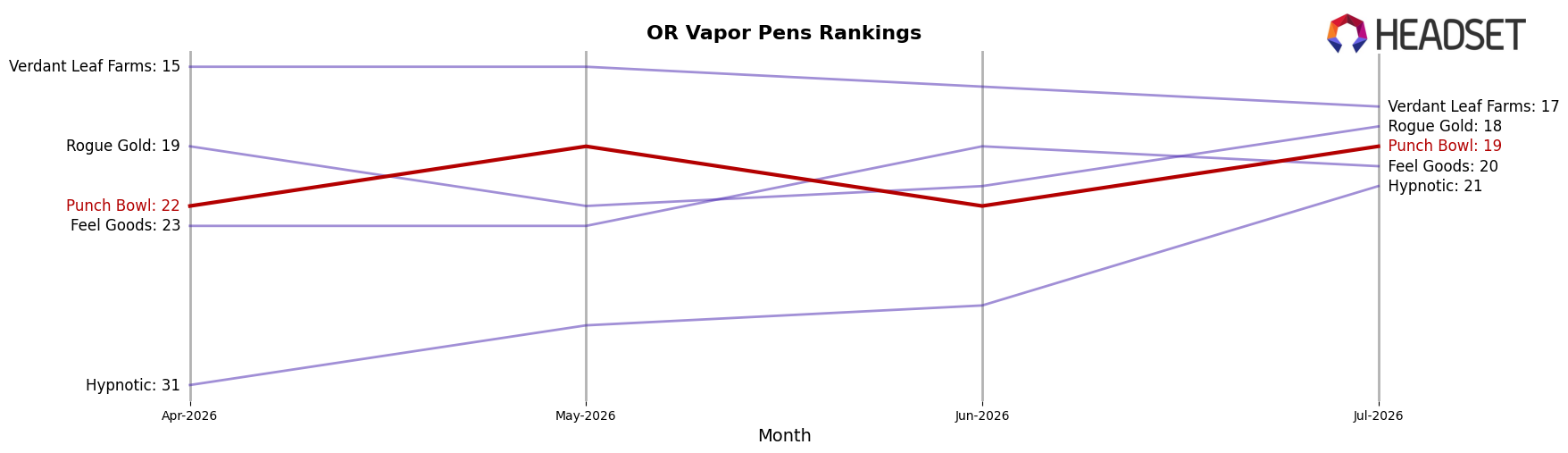

Competitive Landscape

Punch Bowl sits at rank #19 in Oregon Vapor Pens as of July 2026, a 9-place climb from #28 year over year and a 3-spot improvement from #22 three months prior, while also tying its peak at #19 in July 2026; meanwhile, Buddies moved up from #2 to #1 with 17.3% YoY sales growth and Entourage Cannabis / CBDiscovery slid from #1 to #2 with a 33.4% YoY sales decline, framing a ladder where mid-pack mobility like Punch Bowl’s +9 ranks coexists with top-tier volatility of 1–2 rank swaps. This pattern implies Punch Bowl’s upward trajectory is driven more by consistent incremental share gains than market churn, positioning it to convert a #22-to-#19 three-month climb into sustained top-15 contention if similar rank velocity persists.

Notable Products

Strawberry Banana Bash Flavored Distillate Disposable (2g) posted the standout move in July 2026 with a +66.9% month-over-month surge, climbing into rank 6 while Passionfruit Pleaser Flavored Distillate Cartridge (1g) also cleared the 50% threshold at +55.1% to reach rank 9. Against these gains, Maui Wowie Flavored Distillate Cartridge (1g) slid 7.8% to hold rank 1, indicating share churn within the top tier as a fast-rising 2g disposable closes the gap. With eight of the top ten as Vapor Pens and two SKUs exceeding +50% MoM, the mix points to accelerating consumer pull toward flavored disposables and higher-capacity formats, implying Punch Bowl’s near-term commercial upside skews to bulk-friendly pen configurations over legacy 1g cartridges.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.