Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Fire Dept. Cannabis is stocked at 130 licensed dispensaries across Oregon, with the deepest coverage in Portland, Salem, Bend, Eugene, and Ontario. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

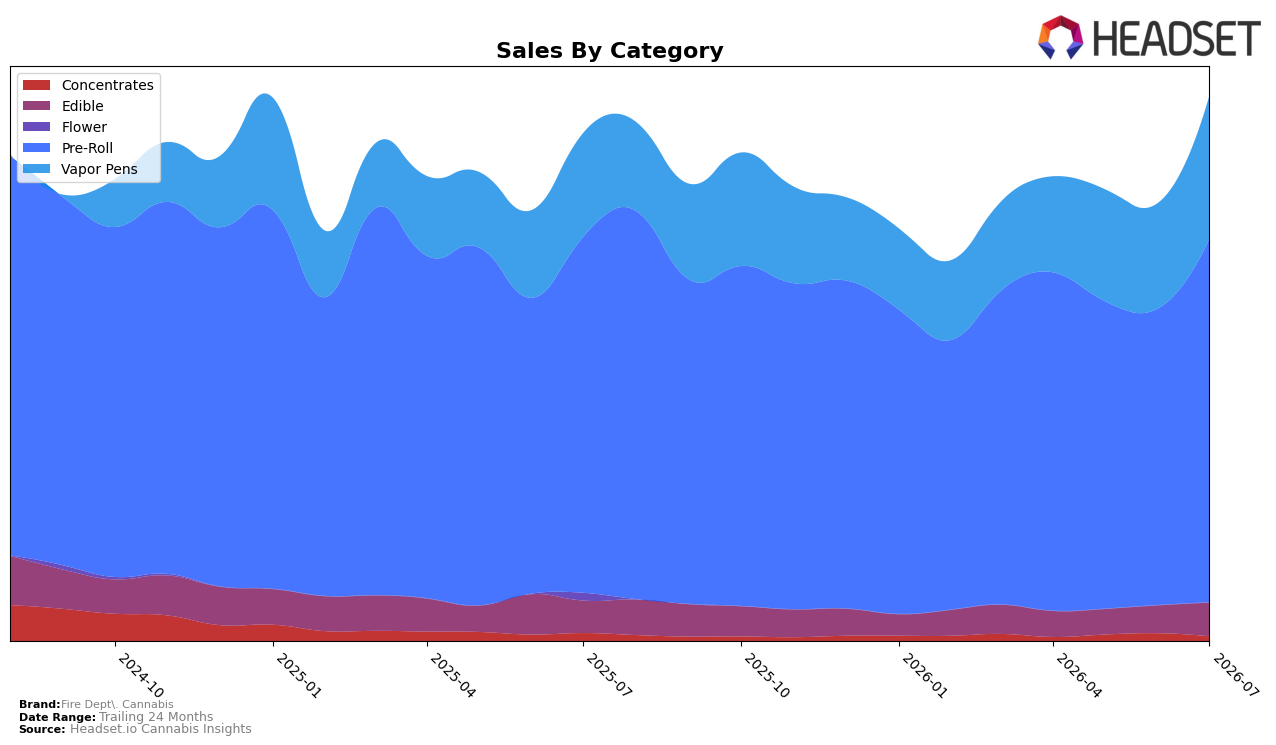

Fire Dept. Cannabis concentrated 66.80% of July 2026 sales in Pre-Roll, ranking 5 in Oregon Pre-Roll, while Vapor Pens expanded to 26.23% share; together these two categories accounted for 93.04% of mix. Month over month, Pre-Roll grew 22.67% and Vapor Pens rose 35.62%, with Edible up 21.60% and Concentrates down 40.97%; year over year, Vapor Pens advanced 37.88% and Pre-Roll edged up 2.19% as Concentrates fell 42.12%. With average price up 3.00% to one figure while total brand sales rose 7.41% year over year, the pattern implies volume and mix shifts toward higher-ticket Vapor Pens are lifting growth while a shrinking Concentrates base limits downside risk.

The surge in Vapor Pens at 26.23% share alongside Pre-Roll’s 66.80% share suggests a two-pillar portfolio where a faster-growing, higher-priced format (22.44 average price) supplements a high-volume core (8.29 average price); this tilt likely increases revenue per unit without overexposing the brand to price-sensitive segments. Holding the 5 position in Oregon Pre-Roll while Vapor Pens post a 35.62% month-over-month gain points to headroom in adjacent inhalable occasions, and the 21.60% month-over-month lift in Edible at 6.13% share provides a buffer against Pre-Roll cyclicality. The implication is a defensible positioning anchored in Pre-Roll rank stability with incremental share capture coming from Vapor Pens, enabling margin leverage as category weights rebalance toward higher average price lanes.

Competitive Landscape

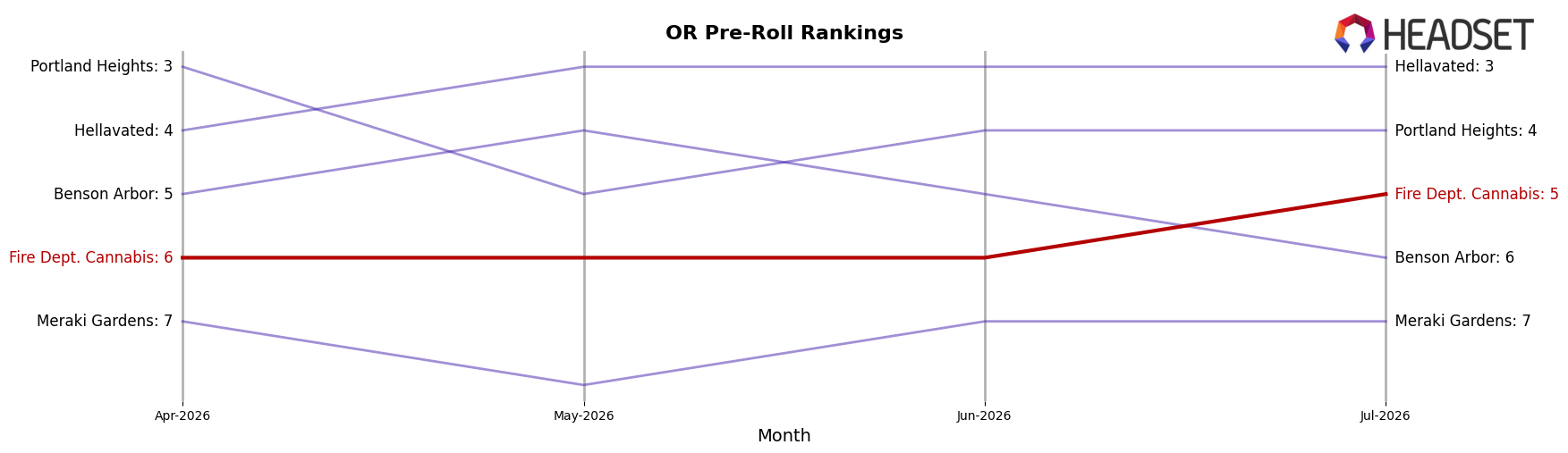

Fire Dept. Cannabis is ranked #5 in OR Pre-Roll for July 2026, unchanged YoY at #5, while improving 1 place from April 2026’s #6 and sitting two spots below its peak of #3 in March 2025; in contrast, STiCKS held #1 YoY to #1 with 148.4% sales growth and Kaprikorn climbed from #6 to #2 with 144.3% growth, whereas Portland Heights slipped from #3 to #4 alongside a 23.1% sales decline. The juxtaposition of Fire Dept. Cannabis holding #5 YoY and inching up from #6 in April 2026, while rivals either surged up the table or lost ground, implies a stable mid-tier position that requires a step-change to convert incremental rank gains into a return toward the historical #3 ceiling.

Notable Products

Purple Milk Pre-Roll (0.5g) posted the largest movement in July 2026 with a +68.9% month-over-month surge and rose into the top 5 at rank 5, while Blue Dream Pre-Roll (0.5g) fell -26.9% and slid to rank 6. Kush Mints Pre-Roll (0.5g) grew +32.8% to hold rank 1, and Jack Herer Pre-Roll (0.5g) dipped -1.1% yet maintained rank 3, indicating stability at the top despite volatility mid-pack. Seven of the top ten are Pre-Roll SKUs, and the presence of a single 10-pack format alongside multiple 0.5g singles suggests basket-size experimentation against a predominantly single-stick mix. The pattern points to Fire Dept. Cannabis leaning into Pre-Roll depth with selective pushes on fast-rising strains to consolidate leadership while pruning underperforming variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.