Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

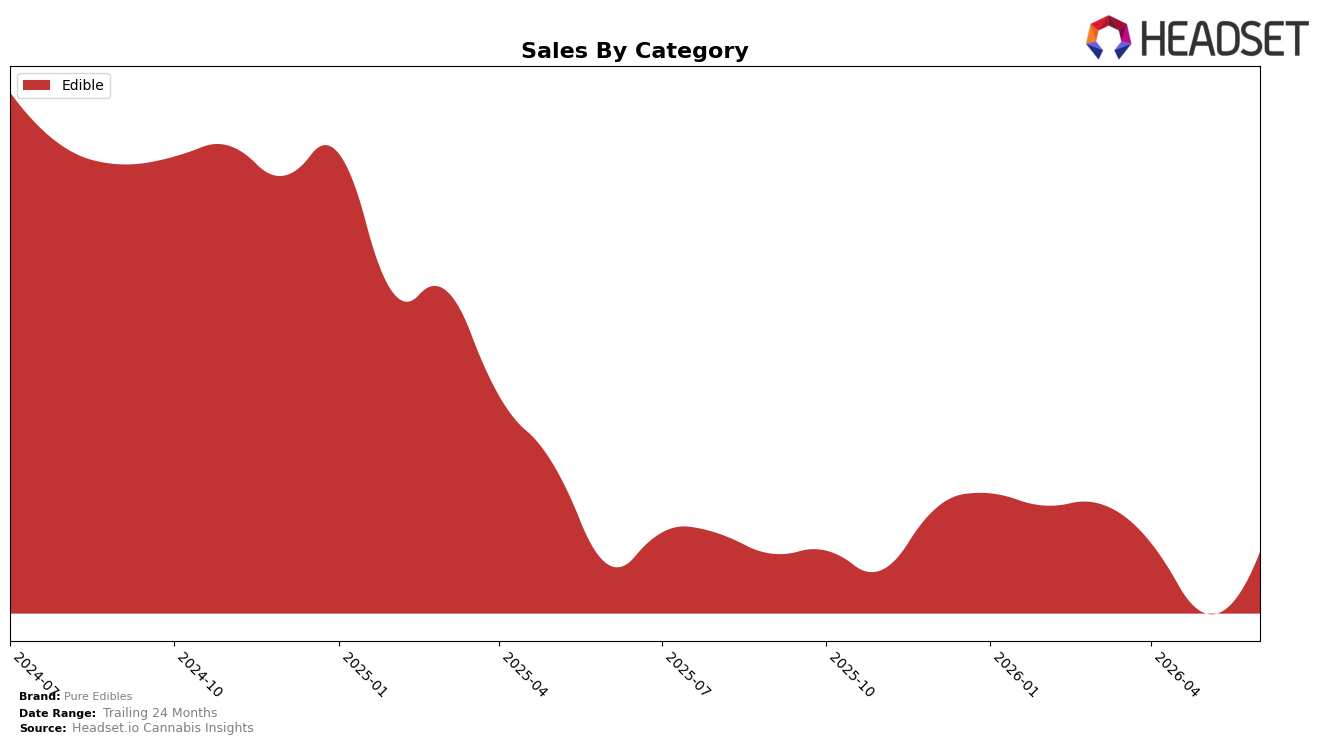

Pure Edibles operated as a single-category brand in June 2026, with Edible accounting for 100.0% of sales and a month-over-month change of 12.81% against a year-over-year change of 2.42%. Average price fell 19.72% YoY to $8.99 while sales still grew 2.42% YoY, indicating volume expansion offsetting price compression; combined with a 12.81% MoM lift in June 2026 and a category rank of 9 in Arizona, the mix signals concentration rather than diversification. The pattern implies Pure Edibles is leaning into price-led volume gains within Edibles rather than allocating share to other categories.

The shift toward lower average price alongside positive YoY and double-digit MoM sales in June 2026 suggests Pure Edibles is competing on attainable price points to defend and potentially improve its number 9 position in Arizona. With 100.0% category dependence and a 2.42% YoY sales increase occurring despite a 19.72% YoY price decline, the implied strategy prioritizes penetration and repeat purchase over premiumization; the thesis is that sustained price elasticity in Edibles can support share stability in 2026 even as longer-term 24‑month sales contraction of 46.55% constrains headroom.

Competitive Landscape

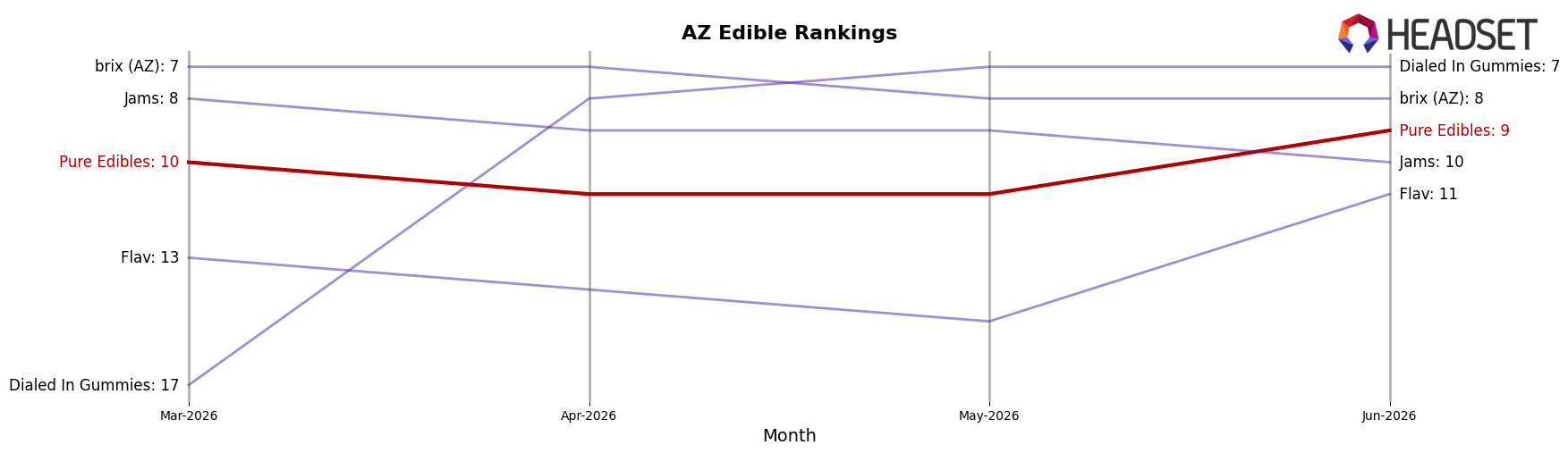

Pure Edibles sits at rank #9 in AZ Edible in June 2026, down 1 position year over year from #8 and up 1 place versus March 2026’s #10, while still trailing its peak #7 from September 2025; within this context, Wyld held #1 with a -15.28% YoY sales change and Baked Bros climbed from #4 to #3 on +30.87% YoY growth, indicating competitors are either consolidating share at the top or accelerating. The combination of a modest quarter-over-quarter climb (from #10 to #9) alongside a year-over-year slippage (from #8 to #9) implies Pure Edibles is stabilizing mid‑tier while losing relative pace to faster-moving rivals.

Notable Products

Sativa Mango Gummies 10-Pack (100mg) posted the biggest movement in June 2026 with a 47.3% month-over-month rise to rank 5, while Sativa Fruit Punch Gummies 10-Pack (100mg) climbed 22.3% to rank 3, indicating sativa-led momentum inside the top five. THC/CBN 2:1 Indica Berry Sleepy Gummies 10-Pack (100mg THC, 50mg CBN) held rank 1 with a 15.2% lift, and Indica Watermelon Gummies 10-Pack (100mg) eased 4.6% at rank 2, pointing to leadership from a sleep-oriented SKU alongside expanding daytime offerings. Four of the top ten are Sativa gummies, and three are Indica gummies, so the portfolio is concentrated in classic fruit-flavor THC gummies rather than minor-cannabinoid blends, which implies Pure Edibles is tilting toward volume drivers in familiar formats over niche formulations.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.