Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Flav is stocked at 260 licensed dispensaries across New York, Missouri, and 6 other states, 139 of them in New York, with the deepest coverage in New York, Queens, Bronx, Brooklyn, and Bushwick. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

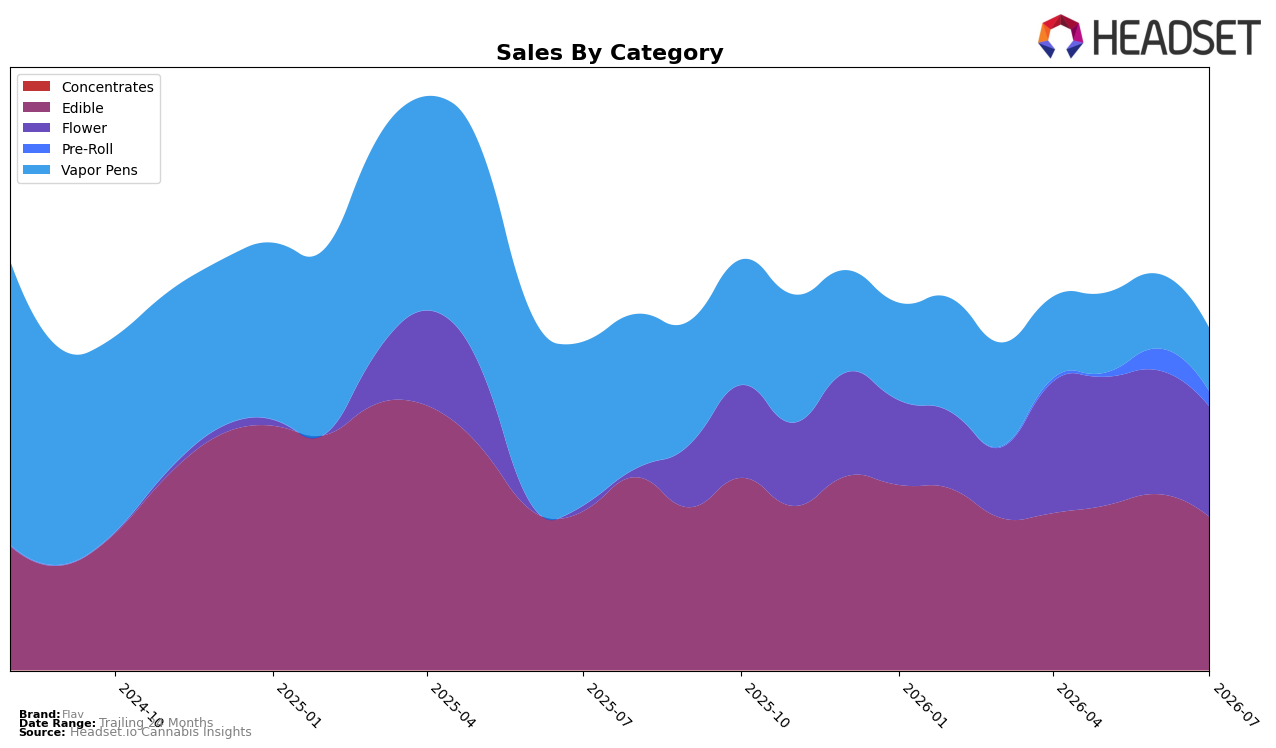

Flav’s July 2026 category mix consolidated into Edible at 44.86% share and Flower at 32.32% share, while Vapor Pens fell to 18.51% share and Pre-Roll to 4.32%. Year over year, Flower surged 1,981.65% even as Edible declined 3.67%, and month over month, Edible dropped 13.03% while Flower slipped 10.90%. Vapor Pens contracted 61.43% YoY and 15.29% MoM, and Pre-Roll fell 31.53% MoM with no year-ago comp. Despite a 4.06% YoY lift in total brand sales and a 7.32% YoY decrease in average price, the pattern implies the brand is re-weighting toward Flower volume while ceding share and velocity in Vapor Pens and Edible.

The shift coincides with a Flower ranking of 50 in Missouri, indicating that category momentum has yet to translate into higher competitive standing, and that price-led gains may be needed beyond the current average price of $17.44. With Edible down 13.03% MoM and Vapor Pens down 15.29% MoM in July 2026, while Flower also declined 10.90% MoM, the simultaneous monthly pullback across core formats suggests short-term demand softness rather than a single-category misstep. Given New York as the top state and Flower as the top category, sustaining the 1,981.65% YoY Flower surge while stabilizing Edible’s 44.86% share would reposition Flav toward a two-pillar portfolio, implying that execution focus should shift from breadth to reinforcing Flower-led penetration where rank headroom exists.

Competitive Landscape

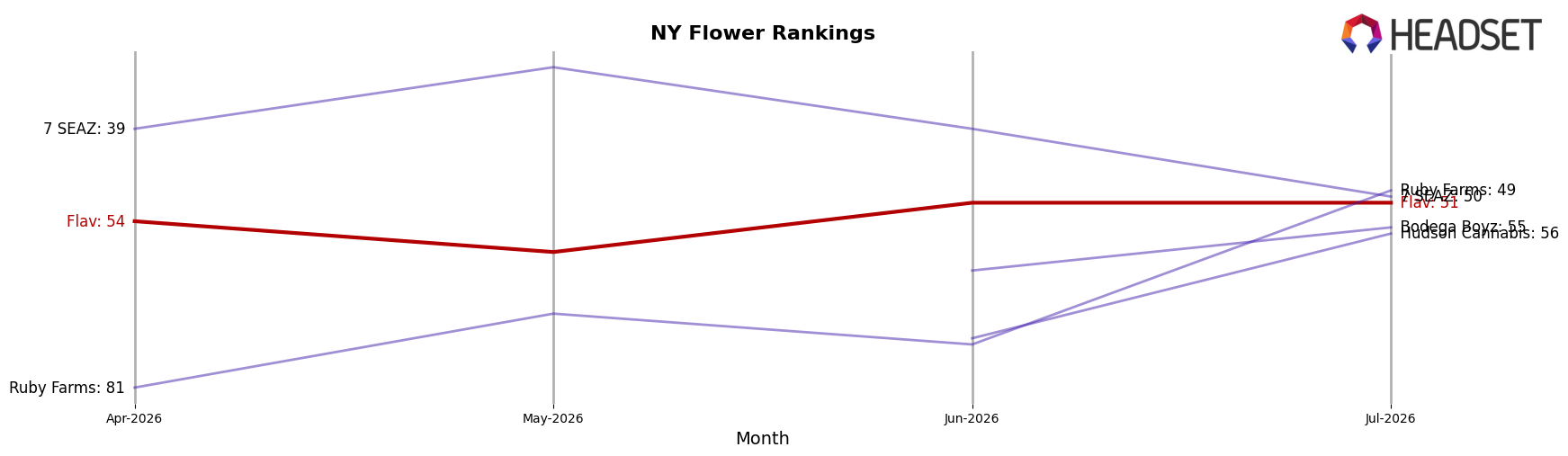

Flav sits at rank 51 in New York Flower in July 2026, improving 167 positions year over year from rank 218, and edging up 3 spots from April 2026’s rank 54, while still trailing its peak rank 36 from April 2025; in contrast, Find. rose to rank 1 with a 46.7% year-over-year sales increase and Grassroots advanced to rank 5 alongside a 79.8% year-over-year sales lift, whereas Dank. By Definition held rank 3 amid a 51.5% year-over-year sales decline, indicating that Flav’s upward rank trajectory is tied more to steady share recovery than outsized growth, implying runway to gain if it can convert modest quarter-over-quarter rank gains into sustained share capture against top-5 incumbents.

Notable Products

Sour Rainbow Mega Live Resin Gummy Belt (100mg) posted the steepest decline at -55.6% and slid to rank 10, while Rainbow Sour Live Resin Gummy Belts 10-Pack (100mg) also fell -25.8% yet held rank 1; this divergence implies single-belt trial is cooling faster than multi-pack replenishment. Strawberry Live Resin Gummy Belts 10-Pack (100mg) dropped -14.8% at rank 3 as Peach Mega Dosed Gummy Rings 2-Pack (100mg) rose +23.4% to rank 4, signaling momentum toward higher-potency two-packs even as core belts contract. With six of the top ten being Live Resin Gummy Belts and two of the top five now Mega or 2-Pack formats, July 2026 mix skews toward potency-convenience formats and suggests Flav is migrating spend from variety-led belts into concentrated ring and mega SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.