Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Quiet Kings is stocked at 488 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Diego, Santa Rosa, Sacramento, and San Francisco. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

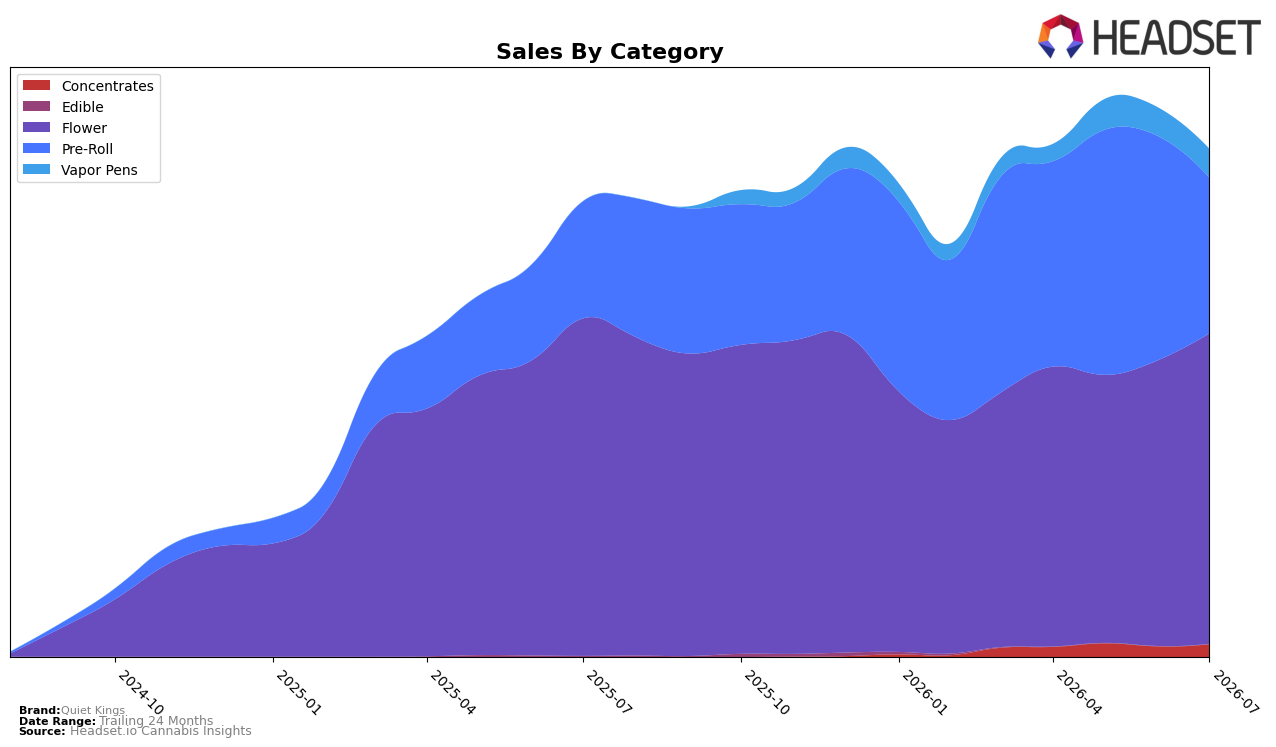

In July 2026, Quiet Kings leaned heavily on Flower at 61.18% share with month-over-month growth of 8.65% but a year-over-year decline of 8.03%, while Pre-Roll held 30.64% share with a 32.93% year-over-year increase offset by a 30.60% month-over-month drop. Vapor Pens and Concentrates remained minor at 5.64% and 2.53% share, posting month-over-month moves of 0.58% and 20.68% respectively, and Edible compressed to 0.01% share despite a 14.11% month-over-month lift after a 92.69% year-over-year fall. With an average price down 22.09% year over year to $10.14 and brand sales up 11.45% year over year, the mix suggests price-led volume capture centered on Flower and Pre-Roll, implying dependence on value tiers within California Flower where Quiet Kings ranks 12.

The July 2026 reweighting—Flower stabilizing in-month (+8.65% MoM) while Pre-Roll retrenched (-30.60% MoM) despite its 32.93% YoY rise—signals a pivot toward anchoring discovery in Pre-Roll but monetizing repeat in Flower at a 61.18% share. The simultaneous 20.68% month-over-month lift in Concentrates alongside a near-flat 0.58% for Vapor Pens indicates Quiet Kings is testing higher-potency niches without overextending from its 12th-place Flower position in California; the implication is to consolidate Flower rank while letting Pre-Roll act as a lower-price acquisition funnel given the 22.09% year-over-year price decline and the 11.45% year-over-year brand sales growth.

Competitive Landscape

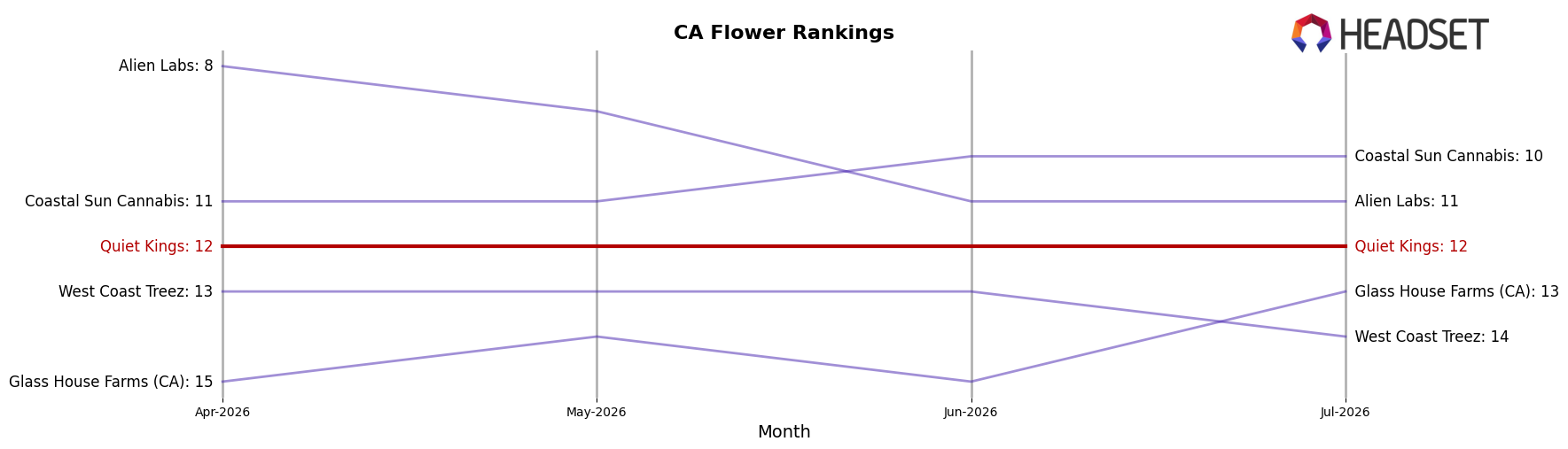

Quiet Kings sits at #12 in CA Flower for July 2026, unchanged from #12 year over year, with a prior peak of #11 in December 2025 and no movement from #12 over the last three months, indicating a stall while leaders reshuffle; meanwhile, STIIIZY climbed from #2 to #1 with 59.7% YoY sales growth and CAM rose from #4 to #3 with 52.2% YoY growth, whereas Claybourne Co. slid from #3 to #5 with a 1.4% YoY sales decline, and CannaBiotix (CBX) moved down from #1 to #2 despite 7.0% YoY growth; the juxtaposition of Quiet Kings’ flat rank and peers’ upward mobility implies the brand’s current assortment or distribution is not converting category tailwinds into share gains, and the trajectory points to entrenchment in the low-teens unless mix or activation changes.

Notable Products

With no month-over-month percentages reported for July 2026, the immediate signal comes from rank concentration: Double Dream Pre-Roll (1g) at rank 1 and Bubba Kush Pre-Roll (1g) at rank 2 anchor a top ten that is 100% Pre-Roll, and two SKUs sit in the top 3 while four land within ranks 1–5. The presence of Blueberry Blast Pre-Roll (1g) at rank 10 despite $15,586 in sales suggests a tight spread across ranks 3–10, while Mimosa Pre-Roll (1g) at rank 7 edges Purple Haze Pre-Roll (1g) at rank 6 by sales momentum implied from position shifts within the mid-pack. The clustering of ten out of ten SKUs in a single category implies Quiet Kings is consolidating around Pre-Rolls, prioritizing depth in a narrow format over breadth in adjacent categories.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.