Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

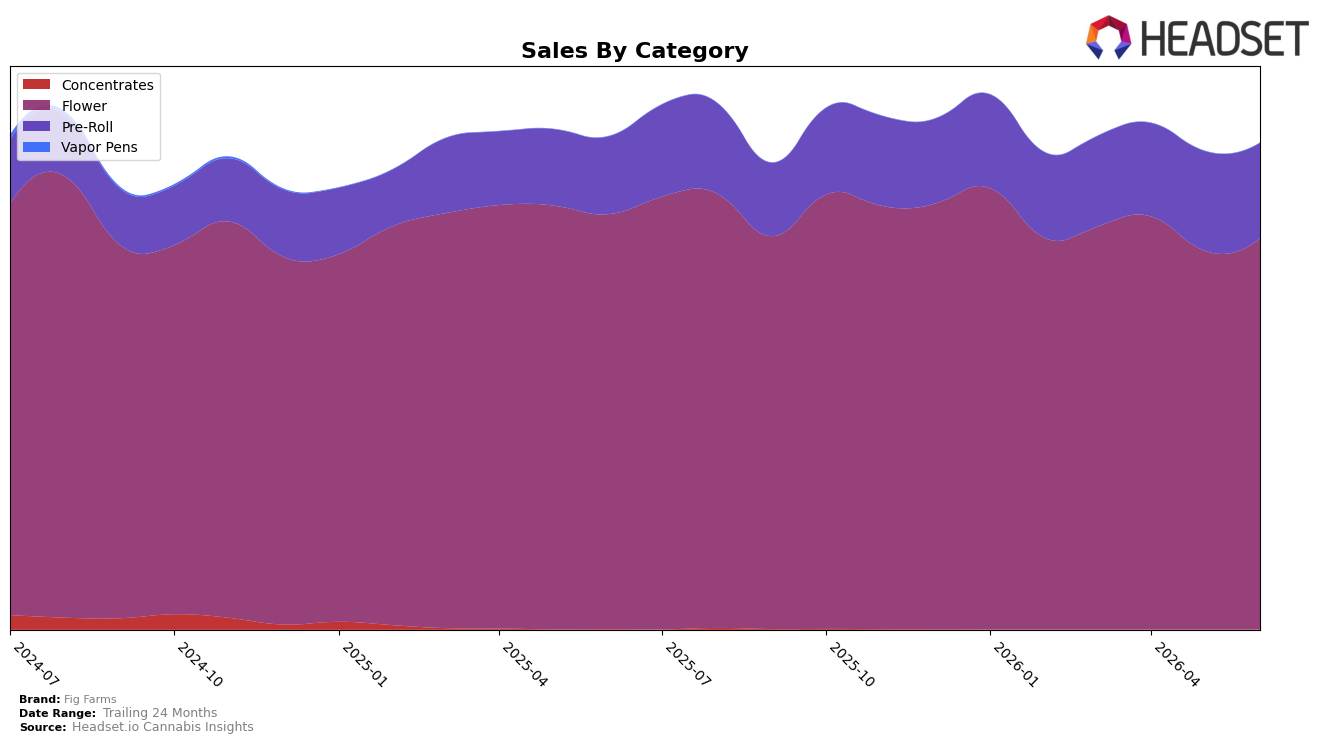

Flower holds 80.39% share in June 2026, down year over year by 5.82% but up month over month by 3.24%, while Pre-Roll sits at 19.61% share with a 23.07% YoY gain and a 4.17% MoM decline; together these shifts coexist with a 1.32% YoY brand sales dip and a 9.97% YoY decrease in average price to $26.47. Within Flower specifically, Fig Farms is ranked 9th in California and that rank, paired with Flower’s MoM uptick and Pre-Roll’s YoY surge, indicates a portfolio tilting from a historically dominant Flower base toward a gradually broader mix as Pre-Roll accumulates share stability despite short-term monthly softness.

The mix suggests pricing-led volume defense in Flower (YoY -5.82% on category sales vs. brand average price -9.97%) alongside a growth wedge in Pre-Roll (YoY +23.07% share uplift contribution vs. MoM -4.17% friction), positioning Fig Farms to use Pre-Roll as an entry lane while Flower maintains scale at rank 9 in California. The implied pattern is that June 2026 momentum relies on sustaining Flower’s MoM +3.24% while converting Pre-Roll’s YoY +23.07% into consistent monthly traction, effectively rebalancing mix away from a single-category dependency without eroding the 80.39% Flower anchor.

Competitive Landscape

Fig Farms sits at rank #9 in CA Flower in June 2026, unchanged YoY from #9, and also flat versus three months ago at #9, while its peak of #8 in November 2025 indicates a one-position slip from its best. In contrast, STIIIZY advanced from #2 to #1 with a 62.5% YoY sales increase, and CAM climbed from #3 to #2 with 56.2% YoY growth, whereas CannaBiotix (CBX) fell from #1 to #3 despite a 2.4% YoY increase. The combination of Fig Farms’ zero-rank-change YoY and a one-rank gap from its November 2025 peak implies a stalled trajectory in a tier where upward mobility is being captured by faster-advancing leaders.

Notable Products

Blue Face (3.5g) posted the headline move with a 141.7% month-over-month surge to rank 1, while Holy Moly Pre-Roll (1g) slid 13.1% to rank 3 and Fig OG (3.5g) fell 19.0% at rank 4. Four of the top ten are Flower SKUs, and within that set Krypto Chronic #1 (3.5g) rose 22.1% at rank 2 as Rapper Weed (3.5g) contracted 39.4% at rank 9, indicating share consolidation around two leaders rather than broad category lift. The mix shows Flower driving the leaderboard with one outsized gainer and one steep decliner, which implies Fig Farms is leaning into a hit-driven portfolio where a few flagship eighths can offset volatility elsewhere.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.