Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Oakfruitland is stocked at 235 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Diego, Sacramento, San Jose, and Fresno. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

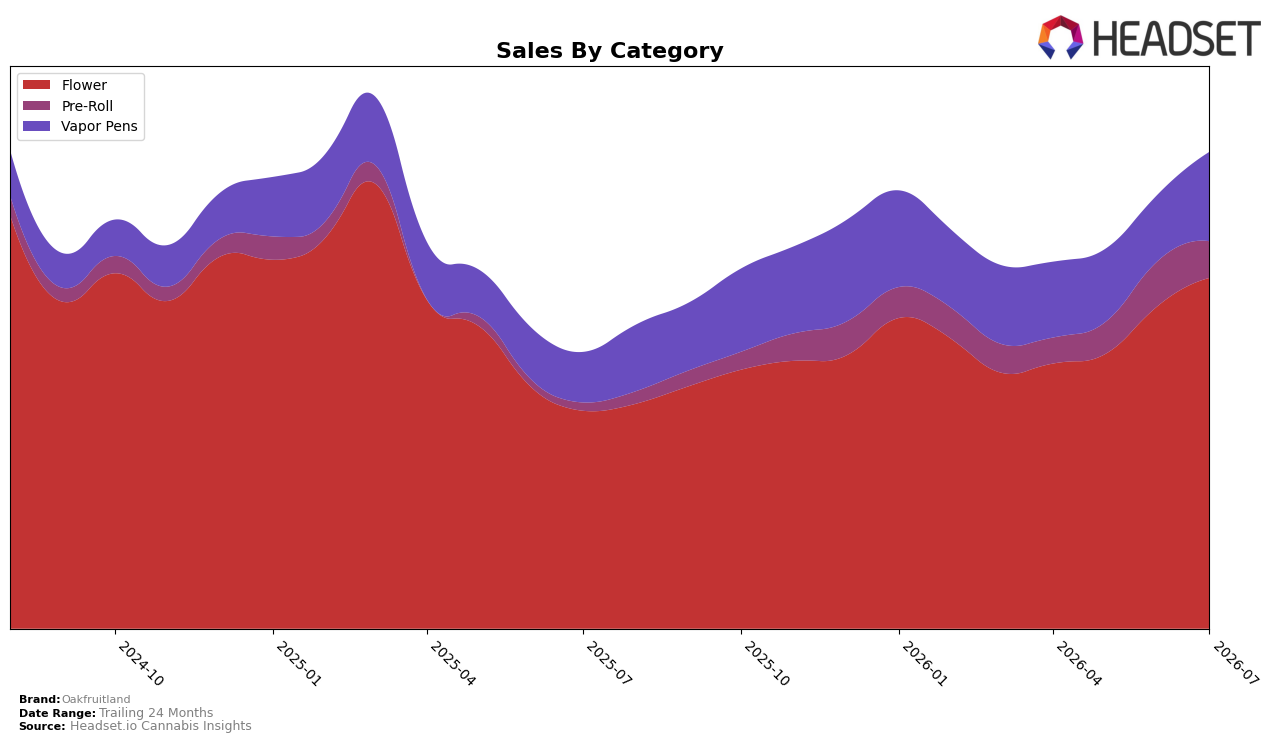

In July 2026, Oakfruitland concentrated 72.17% of sales in Flower with year-over-year growth of 59.41% and month-over-month growth of 8.49%, while Vapor Pens held 19.25% share with 69.13% YoY and a sharper 31.53% MoM lift; Pre-Roll accounted for 8.57% share with 202.90% YoY expansion but a -16.44% MoM retreat. With average price up 8.06% YoY to $30.20 alongside a Flower average price of 36.77 and Vapor Pens at 25.44, the mix is tilting toward higher-priced Flower and rapidly rebounding Vapor Pens, implying July 2026 momentum came from premium-weighted core Flower supplemented by a tactical push in Vapor Pens rather than sustained Pre-Roll velocity.

Holding rank 7 in Flower in California while Flower’s share remains above 70% and Vapor Pens delivers a 31.53% MoM surge suggests Oakfruitland is anchored in core Flower credibility but is using Vapor Pens to expand basket reach and defend shelf space. The mix shift—59.41% YoY growth in Flower against 202.90% YoY in Pre-Roll paired with a -16.44% MoM pullback—implies July 2026 positioning favors depth over breadth: reinforce Flower leadership where it already ranks 7, and selectively scale Vapor Pens to capture incremental occasions without overextending into more volatile Pre-Roll.

Competitive Landscape

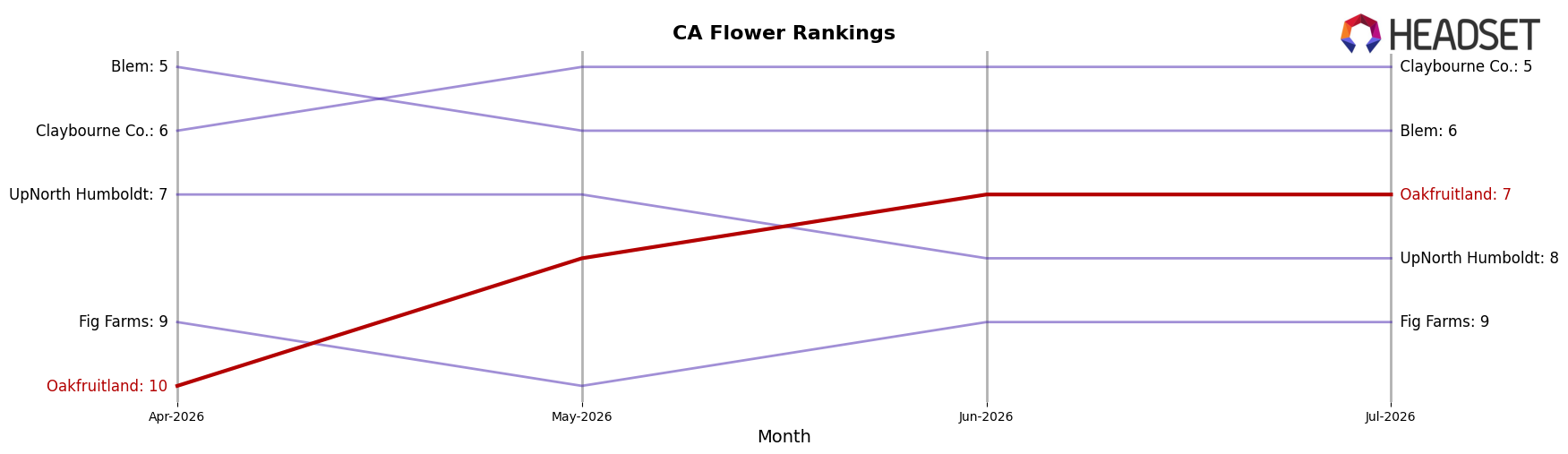

Oakfruitland sits at rank #7 in CA Flower for July 2026, an improvement of 7 positions year over year from #14, and a 3-position climb from April 2026 when it was #10. The brand’s peak was #3 in March 2025, so the current placement is 4 spots below that watermark, while top-tier momentum is consolidating at the front: STIIIZY rose from #2 to #1 and CAM advanced from #4 to #3, indicating that Oakfruitland’s mid-pack ascent is occurring as leaders pull further ahead; the pattern implies Oakfruitland is regaining share but must convert rank stability into another leap or risk getting boxed out of the top five.

Notable Products

Pandora's Box (7g) set the pace in July 2026 with a 18.7% month-over-month lift while holding rank 1, and Lucky Dragon (3.5g) advanced 18.8% alongside Oak-lato Cured Resin Disposable (1g) up 18.5% at rank 10; in contrast, Oak Lato (7g) fell 6.3% at rank 5 and Oak Lato Pre-Roll 2-Pack (2g) slid 5.8% at rank 2. Four of the top ten are Flower SKUs, and two are Pre-Roll SKUs, with Pre-Rolls mixed between a 15.2% gain and a 5.8% decline, implying consumer pull is consolidating around a few hero Flower strains rather than format-wide momentum. The top slot’s $229,636 performance combined with sub-10% declines among secondary formats indicates pricing and strain equity are sustaining volume more than pack configuration. The pattern points to Oakfruitland prioritizing flagship Flower strain depth and selective Pre-Roll support instead of broad format expansion.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.