Market Insights Snapshot

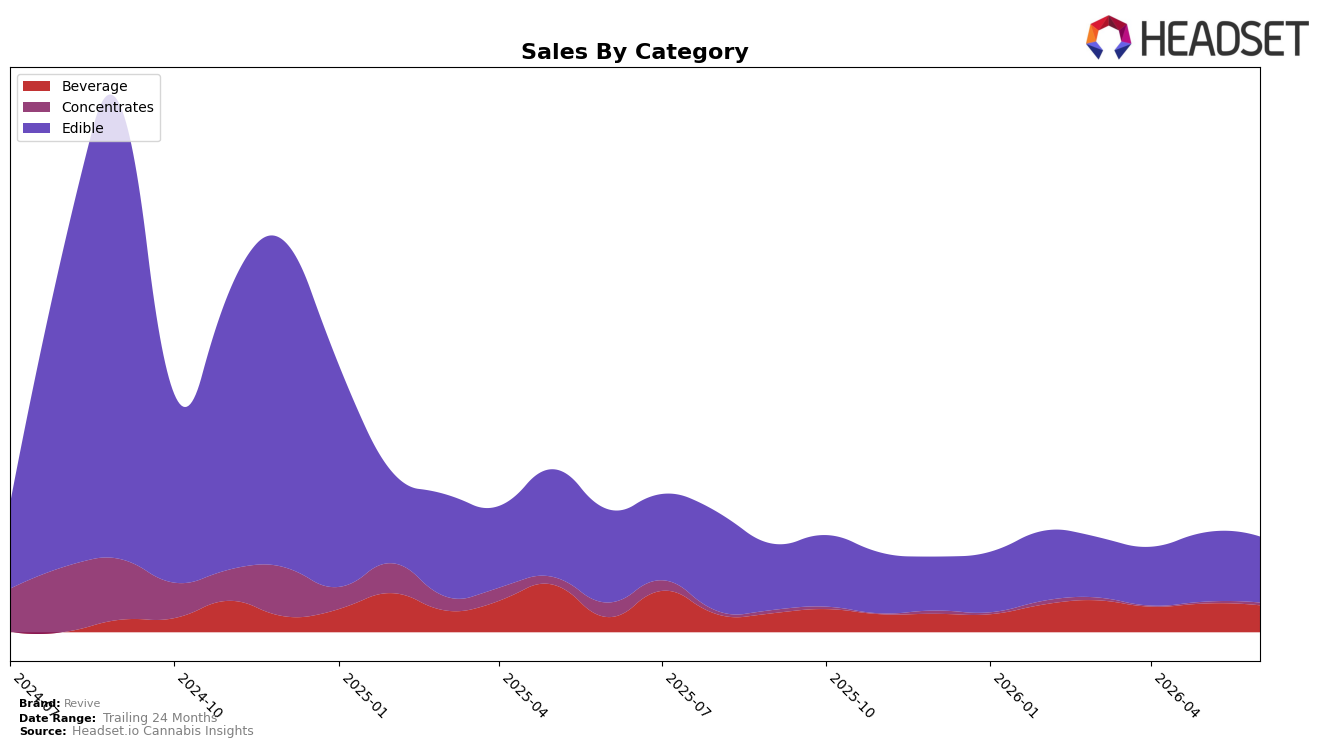

In June 2026, Revive’s category mix tilted heavily to Edible at 69.44% share with a year-over-year decline of 29.27% and a month-over-month dip of 4.67%, while Beverage expanded to 28.09% share on a 79.68% year-over-year increase but eased 6.30% month over month; Concentrates held 2.47% share with an 83.48% year-over-year contraction yet a 65.99% month-over-month rebound. Against a brand-level year-over-year sales change of -22.35% and an average price down 14.75%, the category split suggests price-led compression in Edible is not being offset by Beverage’s growth pace, and the re-acceleration in Concentrates month over month is too small in share to change trajectory, implying mix-driven headwinds outweigh isolated gains.

The shift—Edible down 29.27% year over year while Beverage up 79.68% year over year but down 6.30% month over month—positions Revive as overexposed to a weakening anchor category, reinforced by a rank of 55 in Edible in Ohio and a 4.67% month-over-month contraction in that core. With Concentrates rebounding 65.99% month over month from a 2.47% share base and brand pricing at $15.48 amid a 14.75% price drop, the pattern implies Revive’s near-term positioning hinges on stabilizing Edible velocity while using Beverage’s larger 28.09% share to absorb price pressure, rather than leaning on low-share Concentrates to drive recovery.

Competitive Landscape

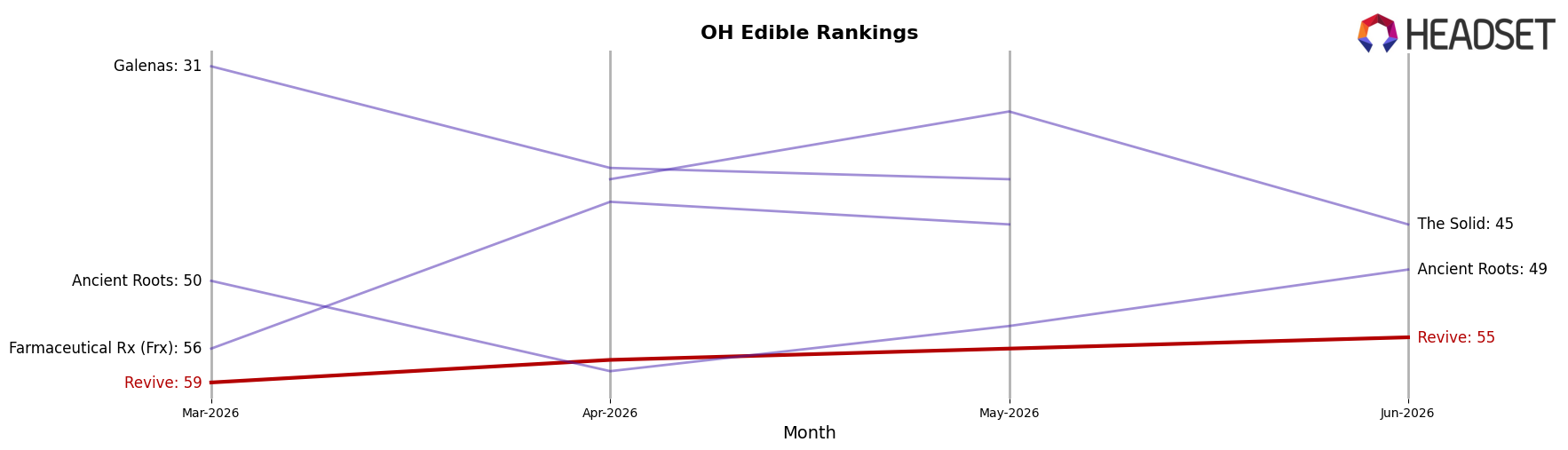

Revive is ranked #55 in Ohio Edible for June 2026, down 6 positions from #49 in June 2025, while improving 4 spots versus March 2026 when it sat at #59; against a longer horizon, the current #55 is 34 places off its peak #21 from September 2024, indicating sustained share compression. In the same period, Incredibles held #1 with a 20.1% year-over-year sales increase, and Gron / Grön advanced from #7 to #2 with a 79.4% lift, outpacing Revive’s rank decline from #49 to #55; meanwhile, UB GOOD rose from #2 to #3 as Revive moved 4 places upward since March 2026 but still trailed its prior-year position by 6. The pattern implies Revive’s recent quarter-on-quarter uptick is insufficient against faster-climbing leaders, pointing to a trajectory of relative share loss unless rank momentum exceeds competitor gains.

Notable Products

Salted Caramel Syrup (100mg) posted the steepest decline in June 2026 at -37.9% while sliding to rank 8, as Salted Dark Chocolate Squares 10-Pack (100mg) also fell -15.4% at rank 3, indicating beverage softness coexisting with pressure in legacy edibles. In contrast, THC Rich Dark Chocolate (100mg) rose +26.5% to rank 2 with $5,039 in sales, while category concentration remained clear with seven of the top ten SKUs in Edible and only two in Beverage, pointing to a portfolio increasingly anchored in chocolate-led formats rather than drinkables. The divergence between a +26.5% mover at rank 2 and declines of -19.9% and -25.8% among other edibles suggests a shift toward premium core chocolate while multi-pack and syrup extensions lose momentum. Taken together, the mix implies Revive is consolidating around fewer, higher-velocity chocolate SKUs as experimentation in syrups and select edible packs retracts.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.