Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Terra is stocked at 688 licensed dispensaries across California, Michigan, and 3 other states, 386 of them in California, with the deepest coverage in Los Angeles, San Francisco, San Diego, Sacramento, and San Jose. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

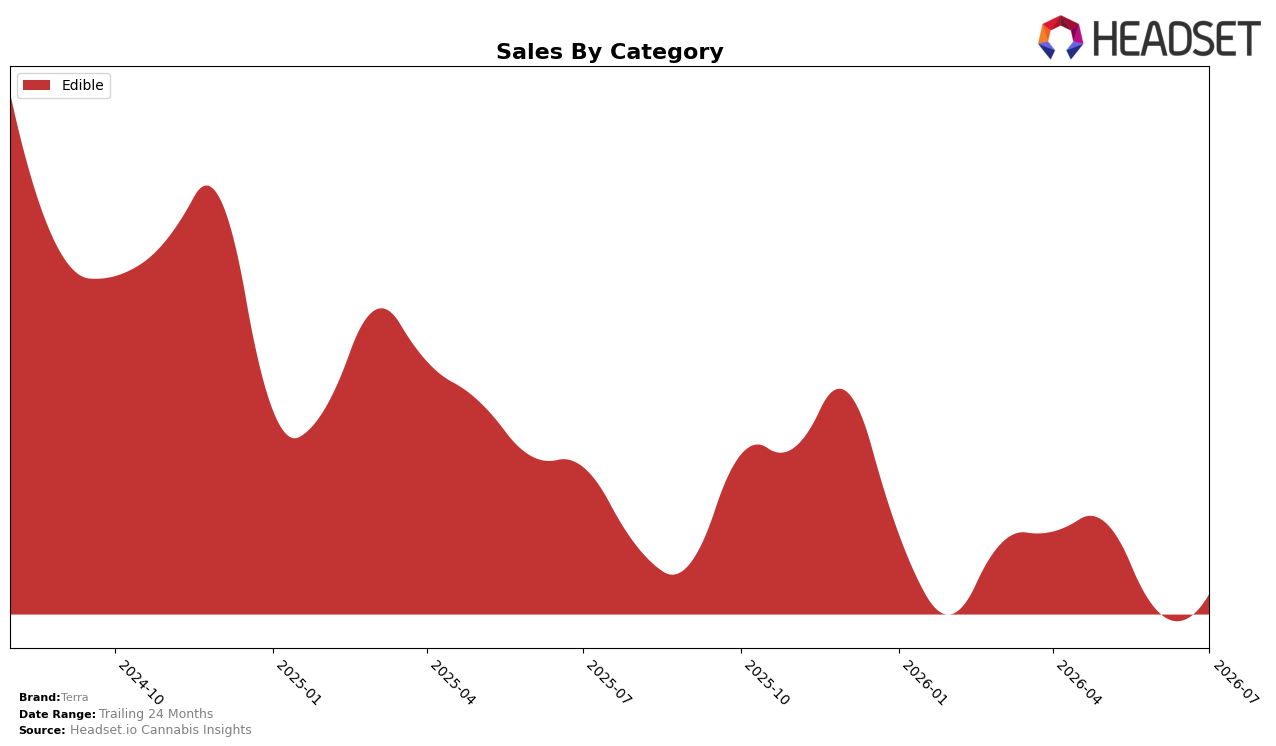

In July 2026, Terra’s category mix was fully concentrated in Edible at 100.0% share, with Edible sales up 3.18% month over month but down 18.02% year over year, while average price ticked up 0.82% YoY. Within California Edibles, Terra held rank 26, a position that juxtaposes short-term MoM stabilization against a double‑digit YoY contraction; the pattern implies Terra is leaning into a single-category bet where near‑term pricing and volume are holding, but the annual drag requires mix or demand recovery to protect share.

Given a 100.0% reliance on Edibles and a July 2026 rank of 26 in California, the 3.18% MoM lift alongside an 18.02% YoY decline suggests Terra’s positioning is tied to episodic demand spikes rather than broad-based growth, with a 0.82% YoY price rise indicating limited pricing power. The implication is that Terra’s current placement keeps it mid‑pack where incremental MoM gains are insufficient to offset annual losses, so sustaining rank 26 or improving it likely hinges on either product innovation within Edibles or a future shift that diversifies exposure beyond a single category.

Competitive Landscape

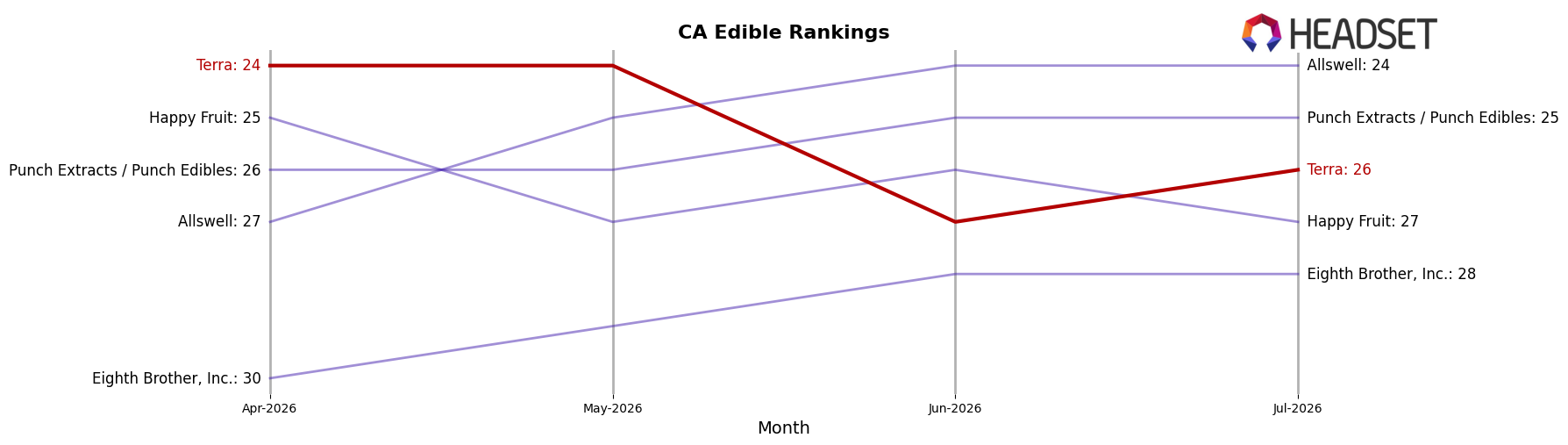

Terra ranks #26 in CA Edible in July 2026, slipping 1 position year over year from #25 and down 2 spots from #24 in April 2026, while still trailing its peak of #21 from December 2024; in contrast, Wyld held #1 with 2.20% YoY sales growth and Camino stayed at #2 with 14.77% YoY growth, indicating Terra’s relative share is being diluted as higher-ranked brands consolidate. With top-five competitors flat-to-rising and Terra’s rank drifting 4 places off its peak and 1 place YoY, the pattern implies Terra must reverse rank erosion to avoid further marginalization within the top-30 tier.

Notable Products

THC/CBN 5:1 Milk And Cookies Chocolate Bites 20-Pack (100mg THC, 20mg CBN) posted the sharpest movement in July 2026 with a +75.3% month-over-month surge while sitting at rank 7, whereas Milk Chocolate Sea Salt Caramel Bites 20-Pack (110mg) fell -63.8% to rank 8. At the top, Blueberry Milk Chocolate Bites 20-Pack (100mg) jumped +321.3% to rank 2 and Dark Chocolate Espresso Bean Bites 20-Pack (100mg) rose +199.7% at rank 1 with about $118,368 in sales. Four of the top ten are Milk And Cookies or Milk Chocolate variants, but the -12.1% decline for Milk Chocolate Sea Salt Caramel Bites 20-Pack (100mg) at rank 4 versus the +45.7% rise for THC/CBN 5:2 Milk And Cookies Chocolate Bites 20-Pack (100mg THC, 40mg CBN) at rank 3 suggests consumers are tilting toward functional CBN blends over classic milk-chocolate profiles. The product mix implies Terra is concentrating demand at the top via format consistency while migrating preference toward differentiated minor-cannabinoid SKUs that can lift mid-pack velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.