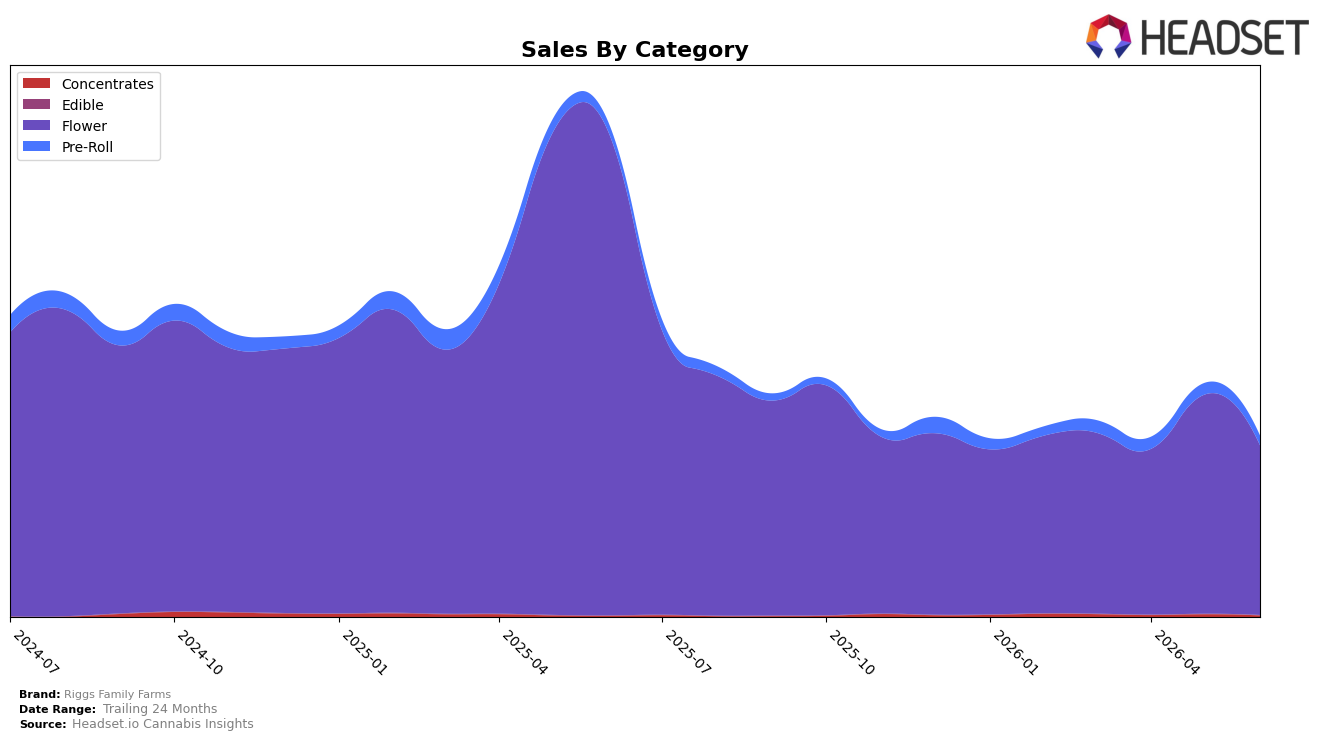

Market Insights Snapshot

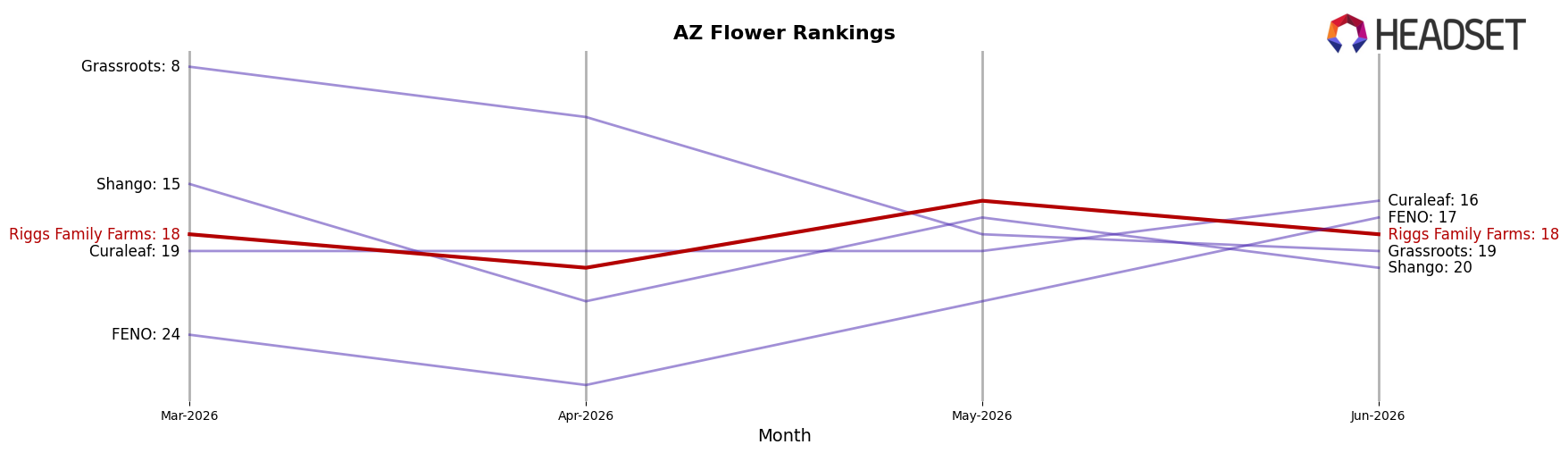

Riggs Family Farms concentrated 94.08% of June 2026 sales in Flower while Pre-Roll held 5.22% and Concentrates 0.70%, with Flower down 64.99% year over year and 22.65% month over month. Pre-Roll was flat year over year at 0.43% but fell 16.74% month over month, whereas Concentrates climbed 62.30% year over year yet dropped 49.04% month over month; average price rose 18.85% year over year to $21.84 as Flower pricing sat highest at $25.77. In Arizona Flower the brand ranked 18, and the category concentration alongside month-over-month declines implies a demand contraction amplified by mix rigidity that pulls down total share faster than the modest Pre-Roll and Concentrates bases can offset.

The mix reliance on a shrinking Flower base — 94.08% share against a 22.65% month-over-month decline and 64.99% year-over-year decline — suggests vulnerability to price elasticity as average prices rose 18.85% year over year while Pre-Roll’s smaller 5.22% share could not counter a 16.74% month-over-month dip. With Concentrates showing 62.30% year-over-year growth but a 49.04% month-over-month drop at a $26.15 average, the volatility indicates limited depth in emerging segments; holding rank 18 in Arizona Flower implies that near-term stability depends on reducing exposure to Flower’s downturn and shifting mix toward categories with steadier month-over-month trajectories.

Competitive Landscape

Riggs Family Farms sits at rank #18 in AZ Flower in June 2026, sliding 14 places year over year from #4 in June 2025, and holding flat versus three months ago at #18, which contrasts with Just Flower rising to #1 from #1 year over year with 13.0% sales growth and The Pharm advancing to #4 from #5 on 44.1% growth; the gap widens further as Brown Bag moved to #5 from #7 with 72.8% growth while Mohave Cannabis Co. held #3 despite a 13.9% sales decline, implying Riggs Family Farms’ rank trajectory has transitioned from a peak (#4) leadership posture to lower-tier stability that now requires a mix-shift or pricing reset to re-enter the top 10.

Notable Products

Creme Brulee Pre-Roll (1g) posted the steepest movement in June 2026 with a -61.7% month-over-month decline while sitting at rank 7, and Face Off OG Pre-Roll (1g) also contracted -29.7% at rank 2, indicating share loss in Pre-Rolls despite two placements inside the top 7. The top-ranked Cookies and Cream (3.5g) fell -49.1% MoM at rank 1, even as three Flower SKUs occupy five of the top six ranks, concentrating the roster in Flower and hinting at lower repeat velocity for value ounces and eighths. With Galaxy #4 (14g) at rank 4 and Ice Widow (14g) at rank 8, Flower accounts for at least four of the top ten, and Cookies and Cream (14g) at rank 6 adds depth even as the 3.5g format softens, suggesting trade-down within the same strain family. Taken together, the mix implies Riggs Family Farms is leaning into larger-format Flower while Pre-Rolls recede, a direction that points to bulk-oriented buyers over convenience-driven shoppers.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.