Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

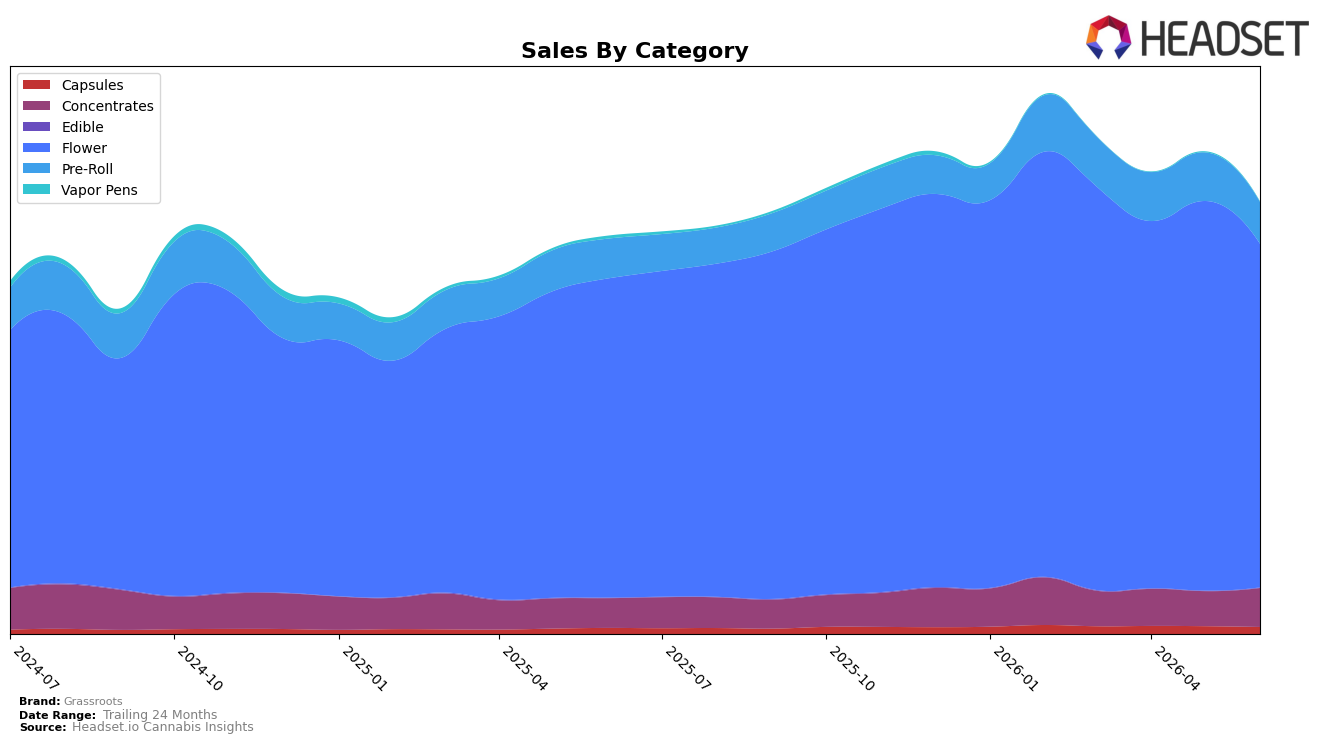

In June 2026, Grassroots concentrated 79.52% of sales in Flower with year-over-year growth of 7.65% but a month-over-month drop of 11.81%, while Pre-Roll held 9.64% share with 5.26% YoY growth and a 13.97% MoM decline. By contrast, Concentrates accounted for 8.97% share with 31.09% YoY growth and an 11.24% MoM increase, and Capsules at 1.67% share rose 15.17% YoY but fell 9.93% MoM. Vapor Pens contracted to 0.10% share with an 83.95% YoY decline and a 49.38% MoM slide, as Edible, though only 0.09% share, climbed 14.88% YoY and 22.63% MoM. The mix indicates reliance on Flower alongside an active pivot toward Concentrates, implying short-term volume softness from Flower and Pre-Roll is being partially offset by higher-velocity gains in Concentrates and selective recovery in Edible.

Positioning-wise, a 7.15% YoY decrease in average price paired with 8.64% YoY brand sales growth suggests Elasticity is working in Grassroots’s favor within Flower even as MoM declines in Flower and Pre-Roll (-11.81% and -13.97%) point to demand seasonality or shelf churn; in parallel, the 11.24% MoM rise in Concentrates and 22.63% MoM rise in Edible create a hedge against Flower volatility. Holding a rank of 5 in Flower in New Jersey while MD remains the top state implies runway to consolidate Flower share through pricing while expanding margin pools in Concentrates (31.09% YoY growth) and Capsules (15.17% YoY growth). Net, the pattern implies Grassroots can sustain category leadership by rebalancing promotional intensity in Flower toward retention, while allocating incremental assortment and merchandising to Concentrates where momentum is accelerating.

Competitive Landscape

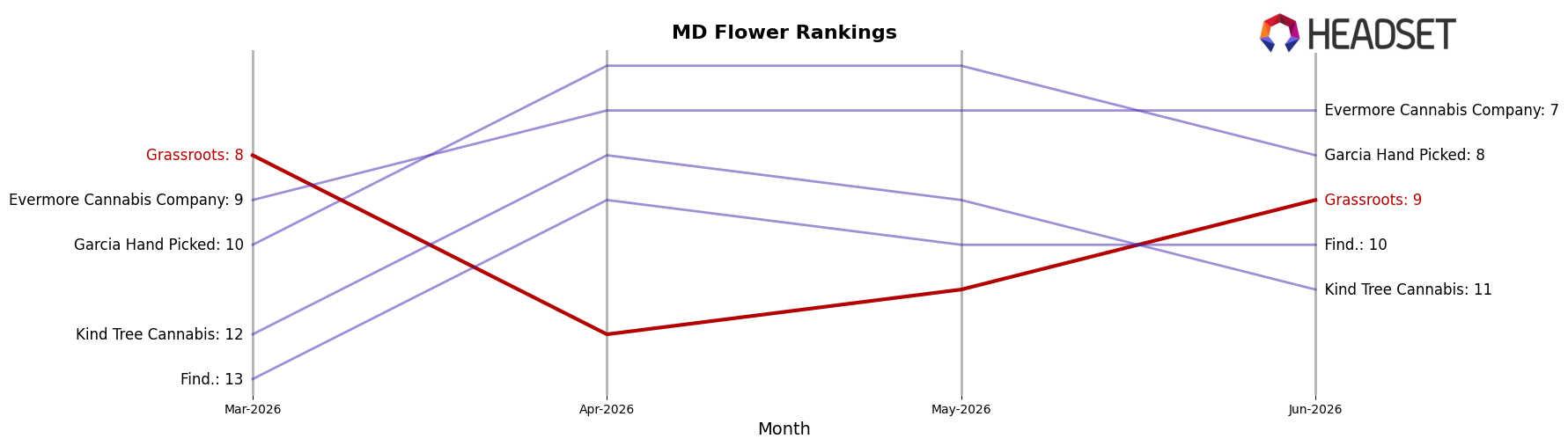

Grassroots sits at rank #9 in June 2026, slipping one position year over year from #8, and down one spot from #8 in March 2026, while still trailing its peak at #5 in September 2025; in contrast, RYTHM advanced from #3 to #2 alongside a 42.7% YoY sales increase and Strane climbed from #7 to #4 with a 58.8% YoY gain. With SunMed steady at #1 and up 13.4% YoY while Fade Co. slipped from #2 to #3 despite 23.7% YoY growth, the pattern indicates that Grassroots’ rank drift from #8 to #9 amid upward moves by rivals points to share being ceded unless rank momentum is restored.

Notable Products

Titan Express (3.5g) posted the steepest decline in June 2026 at -38.1% MoM while sitting at rank 8, and Grassroots x Dark Heart - Triple Stack (3.5g) fell -26.0% at rank 3; in contrast, Floral Frost Pre-Roll (1g) rose +24.7% to rank 1. With two of the top ten in Pre-Rolls and eight in Flower, the pullback concentrated in Flower aligns with Novarine Pre-Roll (1g) slipping -7.9% at rank 2, indicating demand is shifting toward a narrower set of winning Pre-Rolls even as several Flower SKUs lose momentum. The pattern implies Grassroots is relying more on a lead Pre-Roll to carry share while large-format and 3.5g Flower variants require SKU pruning and pricing moves to stabilize rank and mix.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.