Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

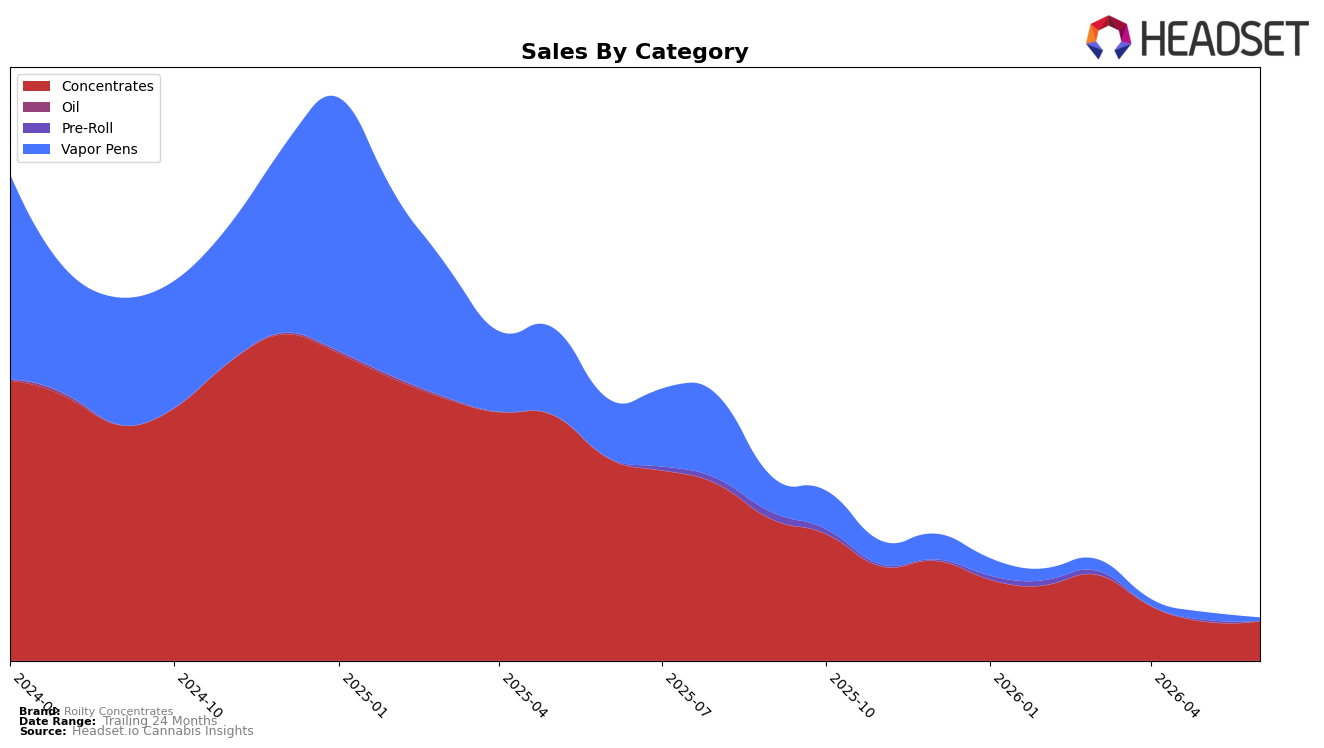

Concentrates account for 92.59% share in June 2026, up 1.05% month over month while down 80.63% year over year, whereas Vapor Pens sit at 7.41% share with a steep 58.63% month-over-month drop and a 94.65% year-over-year decline. The average price is down 3.20% year over year to $29.45, with Concentrates averaging $29.16 and Vapor Pens at $33.66, and within Alberta the brand holds rank 25 in Concentrates. The pattern implies a consolidation around core Concentrates as Vapor Pens contracts sharply and price moderation tightens the focus on volume retention in the lead category.

With Concentrates rising 1.05% month over month in share against a 58.63% month-over-month contraction in Vapor Pens, Roilty Concentrates is prioritizing depth in its primary segment while exiting or deprioritizing peripheral formats. Holding rank 25 in Alberta Concentrates alongside an 80.63% year-over-year decline in that category and a 94.65% year-over-year decline in Vapor Pens suggests the brand’s positioning hinges on stabilizing its core rather than regaining breadth, and the 3.20% average price decrease signals a trade-off toward competitive price points to protect share in a narrower lineup.

Competitive Landscape

Roilty Concentrates sits at rank #25 in AB Concentrates in June 2026, down 20 spots year over year from rank #5, and 13 places lower than March 2026 when it was #12; the brand’s peak was rank #4 in July 2025, marking a 21-place slide from that high. Meanwhile, BoxHot holds #1 after rising from #2 with 37.9% year-over-year sales growth, and Endgame sits at #2 after slipping from #1 with a 23.4% decline, indicating that Roilty Concentrates’ downward rank trajectory is occurring while leadership positions reshuffle at the top. The pattern implies Roilty Concentrates has ceded visibility as faster-moving leaders consolidate share at the top, and without a reversal in the double-digit rank declines across the last three and twelve months, future distribution and velocity could compress further.

Notable Products

Reserve - Grape Galena Live Resin (1g) posted the largest move in June 2026 with +168.8% month over month and reached rank 3, while Legendary Larry Shatter (1g) slid -17.1% to rank 2. Blacksmith's Afghan Hash (2g) also surged +97.1% to rank 1, and Super Lemon Haze Shatter (1g) was effectively flat at +0.1% at rank 4. With four of the top ten belonging to the Shatter family and two of them declining more than -26% (Pink Princess Kush Shatter at -26.3% to rank 5 and Roil Wedding Shatter at -35.6% to rank 7), the portfolio is tilting away from legacy shatter toward higher-velocity formats like live resin and hash.

Purple Dream Sugar Wax (1g) fell -66.1% to rank 9, contrasting with the rise of Blacksmith's Afghan Hash (2g) at +97.1% in rank 1 and the stability of Super Lemon Haze Shatter (1g) at rank 4. Catacomb Kush Shatter (1g) dropped -33.5% to rank 8 as Reserve - Grape Galena Live Resin (1g) advanced to rank 3, with the latter driving one of the month’s largest dollar contributions at $10,515. These divergences imply Roilty Concentrates is consolidating share in premium, terp-driven or traditional formats while pruning or de-emphasizing lower-momentum SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.