Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

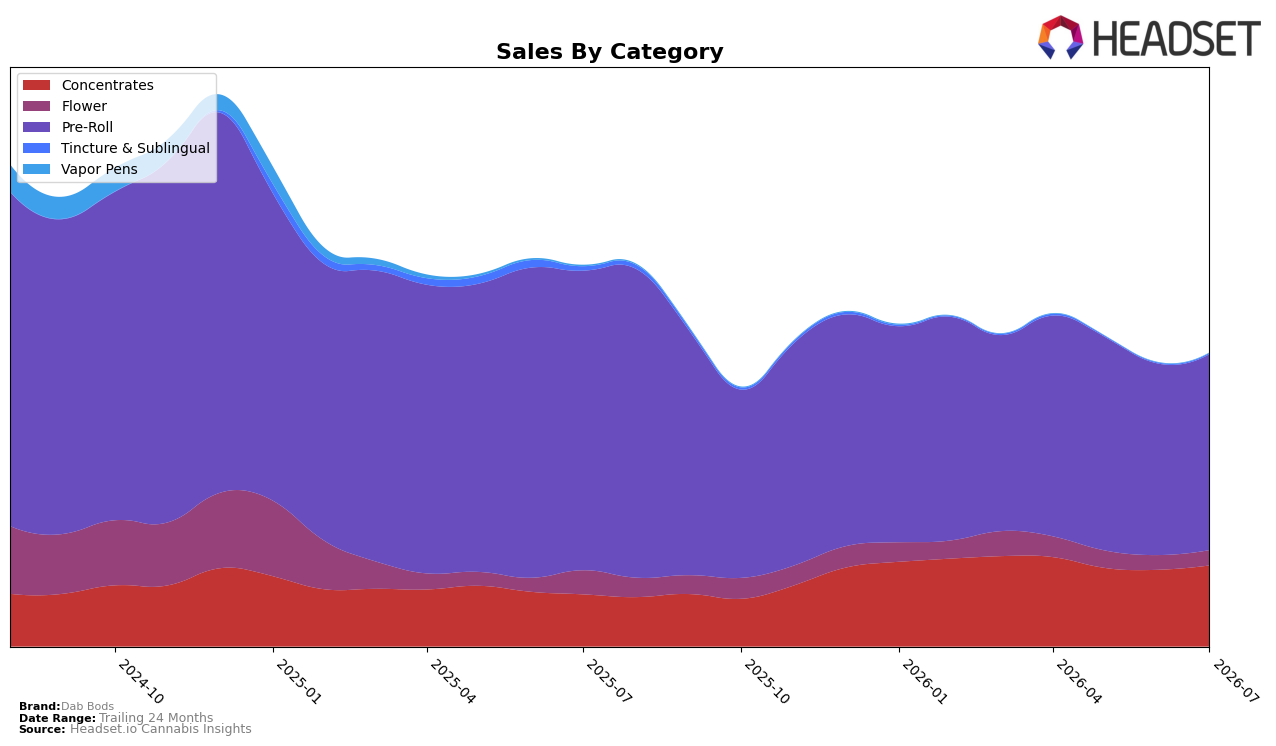

In July 2026, Dab Bods concentrated two-thirds of sales in Pre-Roll at 66.90% share, even as that category fell 34.63% year over year while edging up 2.31% month over month; by contrast, Concentrates held 27.64% share with a 55.77% year-over-year gain and a 5.68% month-over-month increase. Flower contributed 5.12% share with a 36.90% year-over-year decline and a 4.36% month-over-month rise, while Tincture & Sublingual sat at 0.28% share after a 79.95% year-over-year drop but a 24.53% month-over-month rebound; Vapor Pens were 0.05% share with an 85.61% year-over-year decline and a 15.57% month-over-month slide. With overall brand sales down 23.07% year over year and average price down 5.95%, the pattern implies a pivot toward Concentrates momentum while Pre-Roll remains the volume anchor but a drag on annual comps.

Dab Bods’ positioning skews toward value-led Pre-Roll scale (24.47 average price) paired with premium-leaning Concentrates (28.98 average price), which is gaining mix as its growth outpaces Pre-Roll declines; this mix shift increases exposure to a faster-growing segment without abandoning the 66.90% Pre-Roll base. The brand’s July 2026 rank of 15 in Alberta Pre-Roll suggests middle-tier visibility where modest 2.31% month-over-month gains are insufficient to offset a 34.63% year-over-year contraction, implying that near-term share stability depends on translating Concentrates’ 55.77% year-over-year surge into broader basket penetration and improving price architecture following a 5.95% average price reduction.

Competitive Landscape

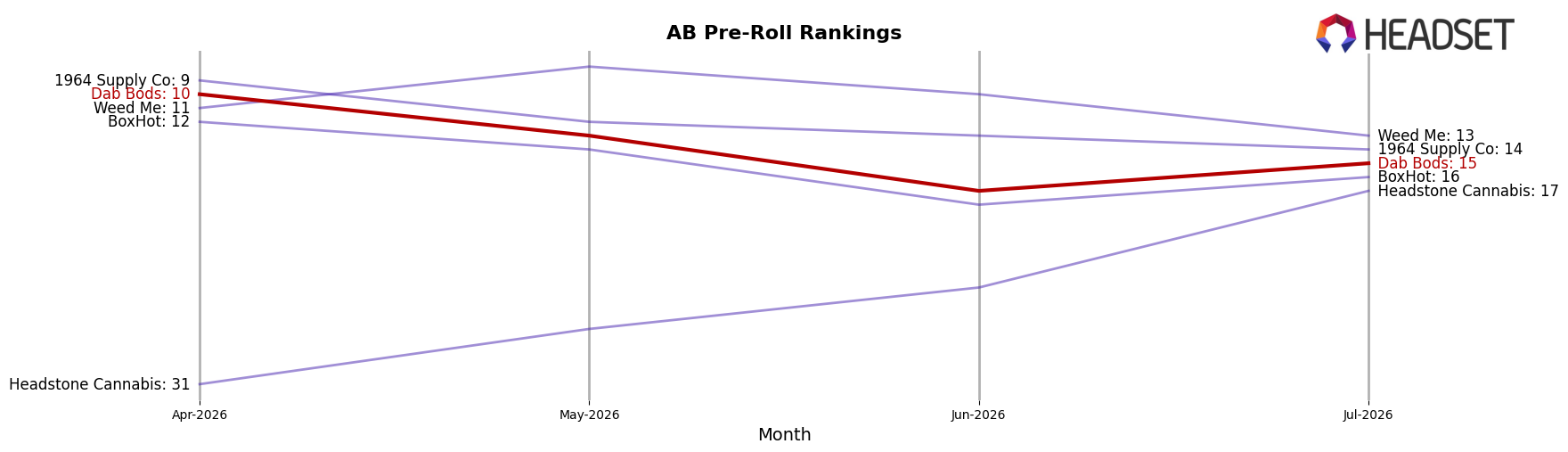

Dab Bods sits at rank #15 in AB Pre-Roll in July 2026, down 6 positions year over year from #9, and 5 spots below its April 2026 placement at #10, while the brand’s historical peak was #2 in January 2025; meanwhile, General Admission held #1 with a 0-position YoY change but saw a -14.5% YoY sales shift, and Back Forty / Back 40 Cannabis climbed from #6 to #2 alongside a 34.3% YoY sales increase. Compared with Space Race Cannabis at #3 (down from #2 with -37.9% YoY sales) and Thumbs Up Brand vaulting from #24 to #5 on 138.3% YoY growth, Dab Bods’ 5-rank slide since April 2026 and 13-rank gap to its January 2025 peak imply share is consolidating among faster-rising competitors, and the trajectory signals a need to counter momentum shifts concentrating at the top five.

Notable Products

60s- Blue Lobster Double Infused Pre-Roll 3-Pack (1.5g) led July 2026 with a 91.8% MoM surge to $197,436 while jumping to rank 1, as Electric Dartz - Berrylicious Super Slim Pre-Roll 10-Pack (4g) slipped 8.6% MoM and sat at rank 5. Electric Dartz - Pineapple Express Super Slim Pre-Roll 10-Pack (3.5g) climbed 115.4% MoM to rank 3, and its sibling Pineapple Express Pre-Roll 10-Pack (4g) rose 24.2% MoM to rank 4, indicating momentum concentrated in two adjacent SKUs. With eight of the top ten positioned in Pre-Roll, the category concentration alongside one Concentrates entry up 21.3% implies Dab Bods is leaning into infused and multi-pack formats as the commercial backbone.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.