Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Ruby Farms is stocked at 276 licensed dispensaries across New York, with the deepest coverage in New York, Queens, Brooklyn, Rochester, and Buffalo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

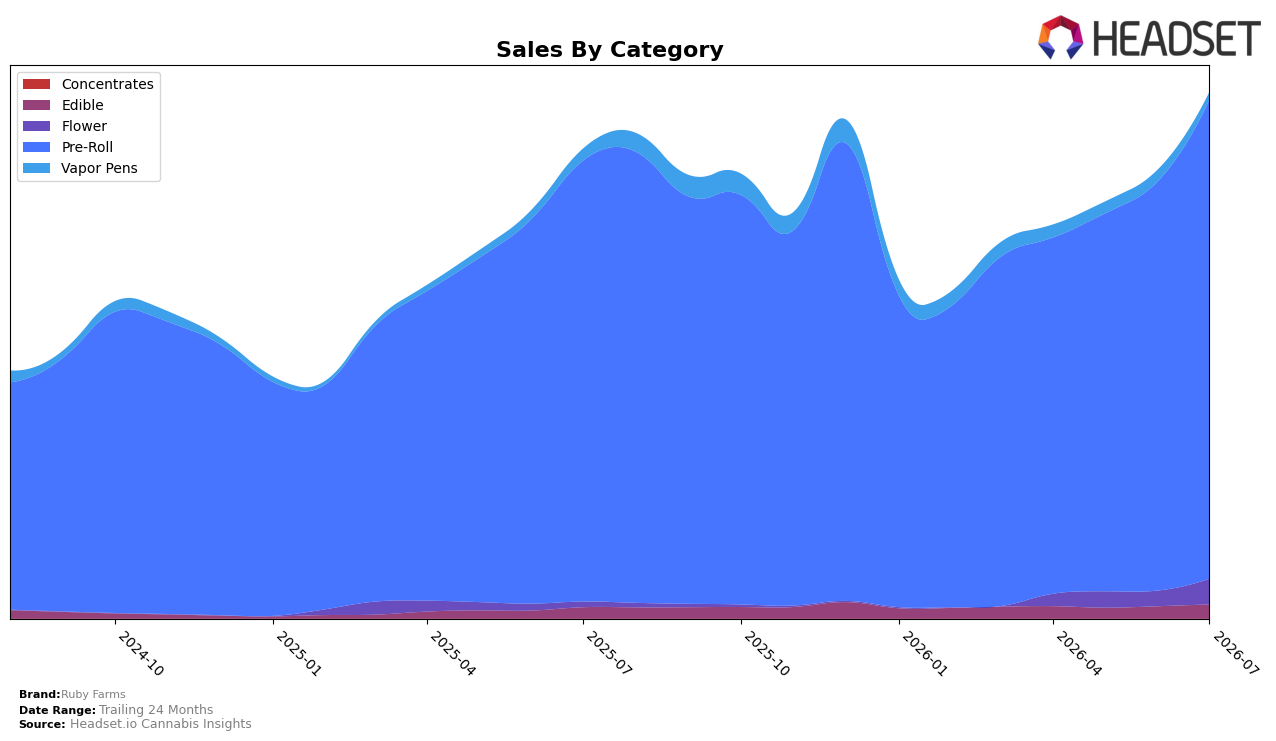

Ruby Farms concentrated 91.12% of July 2026 sales in Pre-Roll, where year-over-year growth was 8.62% and month-over-month growth was 16.99%, while Flower expanded its 4.82% share on a 385.51% year-over-year surge and a 66.15% month-over-month jump. Edible held 2.65% share with 25.30% year-over-year and 15.09% month-over-month growth, whereas Vapor Pens contracted to 1.41% share with a 36.78% year-over-year decline and a 34.97% month-over-month drop. With the brand ranked 1 in Pre-Roll in New York and average price down 0.67% year over year to $38.17, the mix points to deliberate reinforcement of the core Pre-Roll franchise while selectively scaling Flower and letting Vapor Pens retrench.

The pivot signals a positioning that doubles down on Pre-Roll leadership while building a secondary growth pillar in Flower, using price stability around a 0.67% year-over-year decrease to protect volume as Pre-Roll rises 16.99% month over month and Flower jumps 66.15% month over month. With Vapor Pens down 34.97% month over month against 1.41% share and Edible advancing 15.09% month over month at 2.65% share, the pattern implies resource allocation toward ready-to-consume formats that reinforce the July 2026 rank 1 footing in New York while deprioritizing underperforming inhalables.

Competitive Landscape

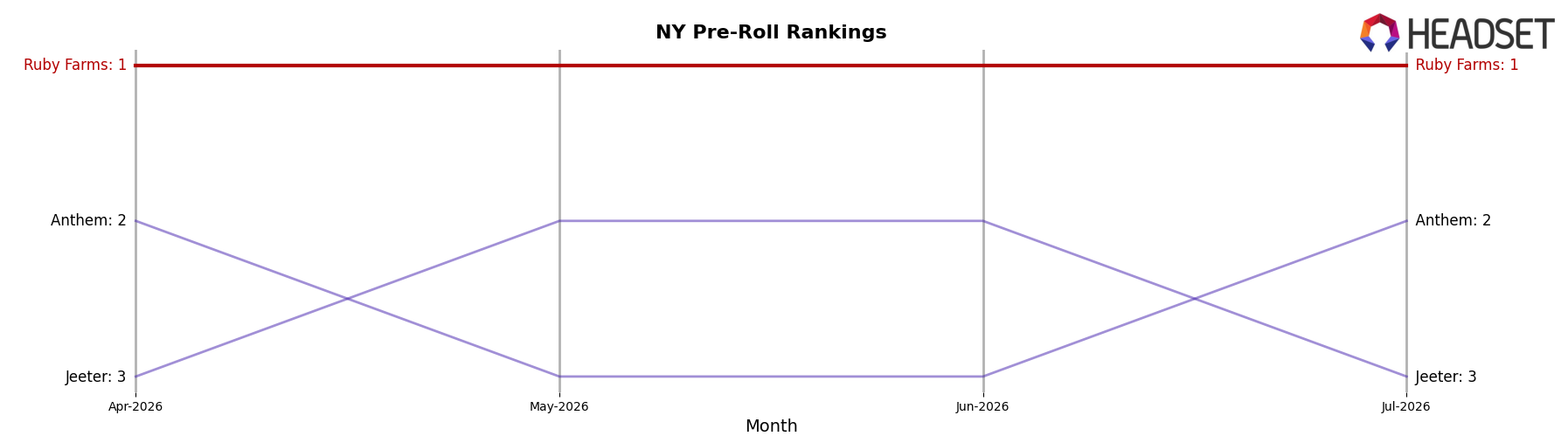

Ruby Farms holds rank #1 in NY Pre-Roll in July 2026, unchanged from #1 a year earlier, with stability at #1 also persisting over the last three months; in contrast, Anthem rose to #2 from #39 year over year alongside an 877.2% sales increase, while Florist Farms sits at #4 with a year-over-year rank position of #4 and a 23.8% sales gain, and Heady Tree is #5 with an 8-position year-over-year climb and 77.4% sales growth; this mix of a flat #1 for Ruby Farms and double-digit rank climbs beneath it implies entrenched leadership now but rising challenger momentum that could compress share if Ruby Farms’ unit velocity or price/mix does not keep pace.

Notable Products

Doobies - Super Lemon Haze Pre-Roll 7-Pack (3.5g) posted the sharpest movement in July 2026 with a +44.2% month-over-month surge, climbing to rank 8 while Doobies - Sour Tangie Pre-Roll 7-Pack (3.5g) slipped 0.2% and held at rank 10. Classics - Sour Diesel Pre-Roll 7-Pack (3.5g) remained at rank 1 with +13.2% growth and $353,503 in sales, and Doobies - White Widow Pre-Roll 7-Pack (3.5g) advanced +31.6% to rank 2. With all ten top SKUs in the Pre-Roll category and four of the top five posting gains above +14.0%, the pattern implies Ruby Farms is consolidating around multi-pack Pre-Rolls where incremental velocity is translating directly into rank stability at the top.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.