Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Florist Farms is stocked at 322 licensed dispensaries across New York and Montana, 321 of them in New York, with the deepest coverage in New York, Buffalo, Queens, Rochester, and Syracuse. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

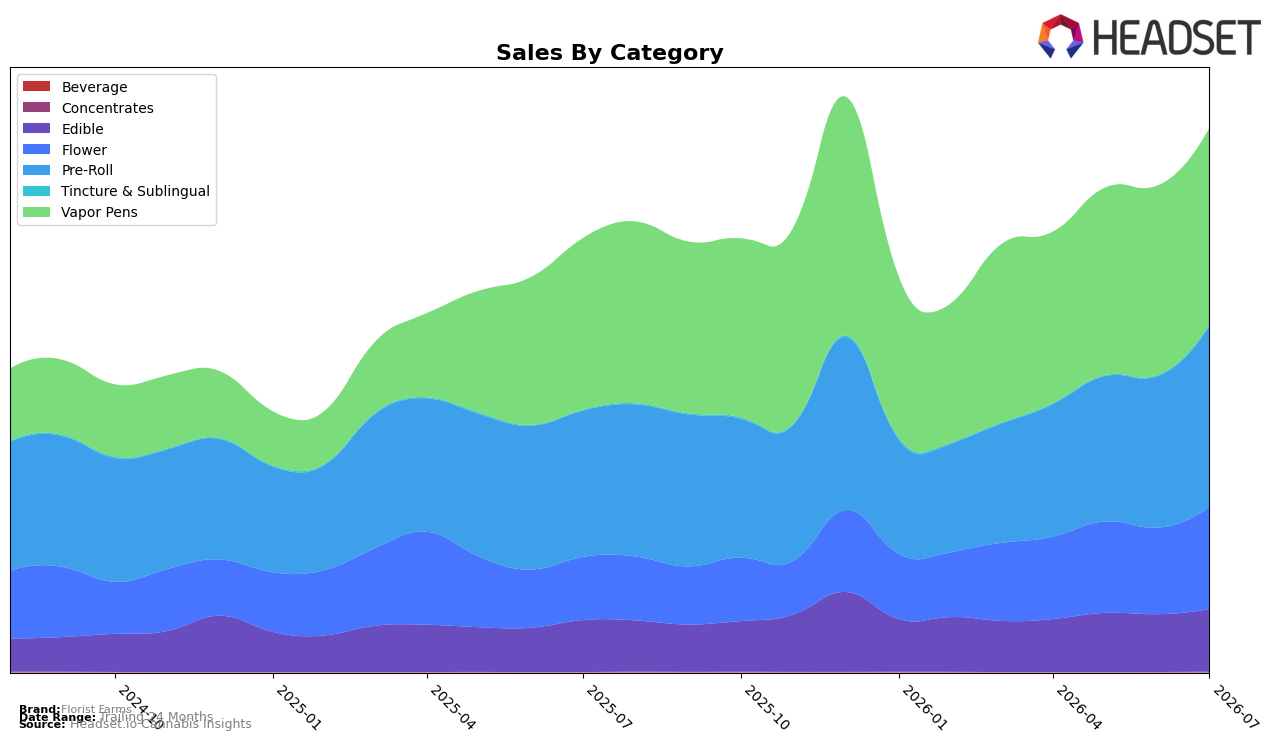

Florist Farms concentrated 36.09% of July 2026 sales in Vapor Pens with year-over-year growth of 14.23% and month-over-month growth of 3.54%, while Pre-Roll held 33.29% share with 23.79% YoY and 19.53% MoM, indicating momentum skewed toward value-accessible inhalables as the average brand price fell 13.67% YoY. Flower expanded to 18.76% share with 62.03% YoY and 18.01% MoM, and Edible accounted for 11.49% share with 20.57% YoY and 8.33% MoM, while micro-mix niches like Tincture & Sublingual (0.27% share; 139.86% YoY; 47.72% MoM) and Concentrates (0.10% share; 805.89% YoY; 302.86% MoM) grew from a small base. The pattern implies portfolio breadth is widening under a price-led strategy, with core mix stability in Vapor Pens alongside faster share-accretive growth in Pre-Roll and Flower.

With Vapor Pens ranked 6 in New York and comprising 36.09% of mix versus Pre-Roll at 33.29%, the brand sits in a diversified inhalables posture where rank-sensitive Vapor Pens growth at 3.54% MoM trails Pre-Roll at 19.53% MoM and Flower at 18.01% MoM, suggesting near-term upside comes more from joint and flower velocity than from carts. The 25.43% brand-level YoY growth paired with a 13.67% YoY price decline and higher MoM surges in Pre-Roll and Flower point to volume elasticity as the primary lever, while rapid but sub-1% share gains in Tincture & Sublingual and Concentrates function as option value rather than mix drivers; taken together, the mix tilt implies competitive positioning will be reinforced by sustaining price-accessible formats while using Vapor Pens rank maintenance to anchor awareness.

Competitive Landscape

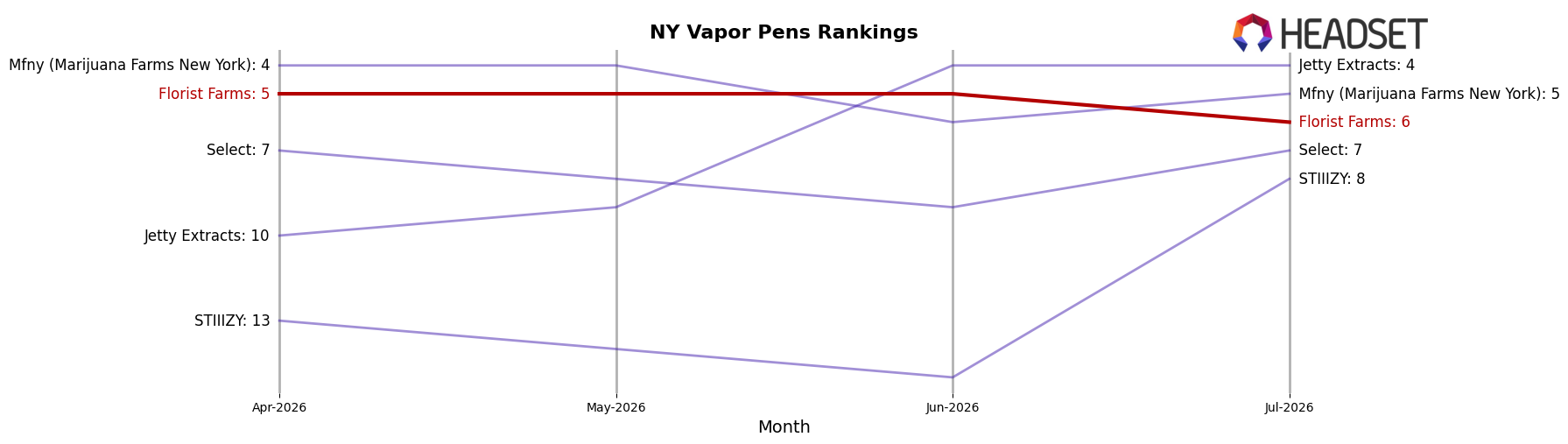

Florist Farms sits at rank #6 in NY Vapor Pens in July 2026, unchanged year over year from #6, after peaking at #5 in June 2026 and slipping 1 position quarter-over-quarter from #5 to #6; this stability contrasts with Jetty Extracts vaulting from #22 to #4 alongside a 199.3% YoY sales gain and Fernway moving from #3 to #1 with a 46.8% YoY increase, while Jaunty fell from #1 to #2 with a 24.8% YoY sales decline; the pattern implies that Florist Farms’ flat rank amid rapid reshuffling at the top signals a need for momentum to avoid being boxed out by faster risers.

Notable Products

The steepest movement in July 2026 is the Blue Dream Live Resin Cartridge (1g) sliding to rank 5 with a -6.9% month-over-month decline while Candy Jack Live Resin Infused Pre-Roll 5-Pack (2.5g) climbed 17.5% to rank 3, indicating share is tilting away from Vapor Pens toward Pre-Rolls. Happy - CBC/THC 1:1 Strawberry Lemonade Gummies 10-Pack (100mg CBC, 100mg THC) held rank 1 with a 10.4% MoM gain as Sleep - THC/CBN 1:1 Bedtime Blueberry Gummies 10-Pack (100mg THC, 100mg CBN) stayed at rank 2 with +6.1%, concentrating demand in functional Edibles while Vapor Pens lose momentum. Three of the top six are Pre-Rolls, with Dutch Hawaiian Infused Pre-Roll 5-Pack (2.5g) up 15.3% at rank 4 and Witches Brew Live Resin Infused Pre-Roll 5-Pack (2.5g) easing -4.0% at rank 6, suggesting multi-pack infused formats are consolidating ranks even as individual SKUs vary in trajectory. The mix signals a commercial pivot toward infused Pre-Rolls and functional Edibles as anchor categories, with Vapor Pens requiring assortment or pricing adjustments to prevent further rank erosion.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.