Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Selfies is stocked at 145 licensed dispensaries across California, with the deepest coverage in Los Angeles, Santa Rosa, Costa Mesa, San Francisco, and San Diego. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

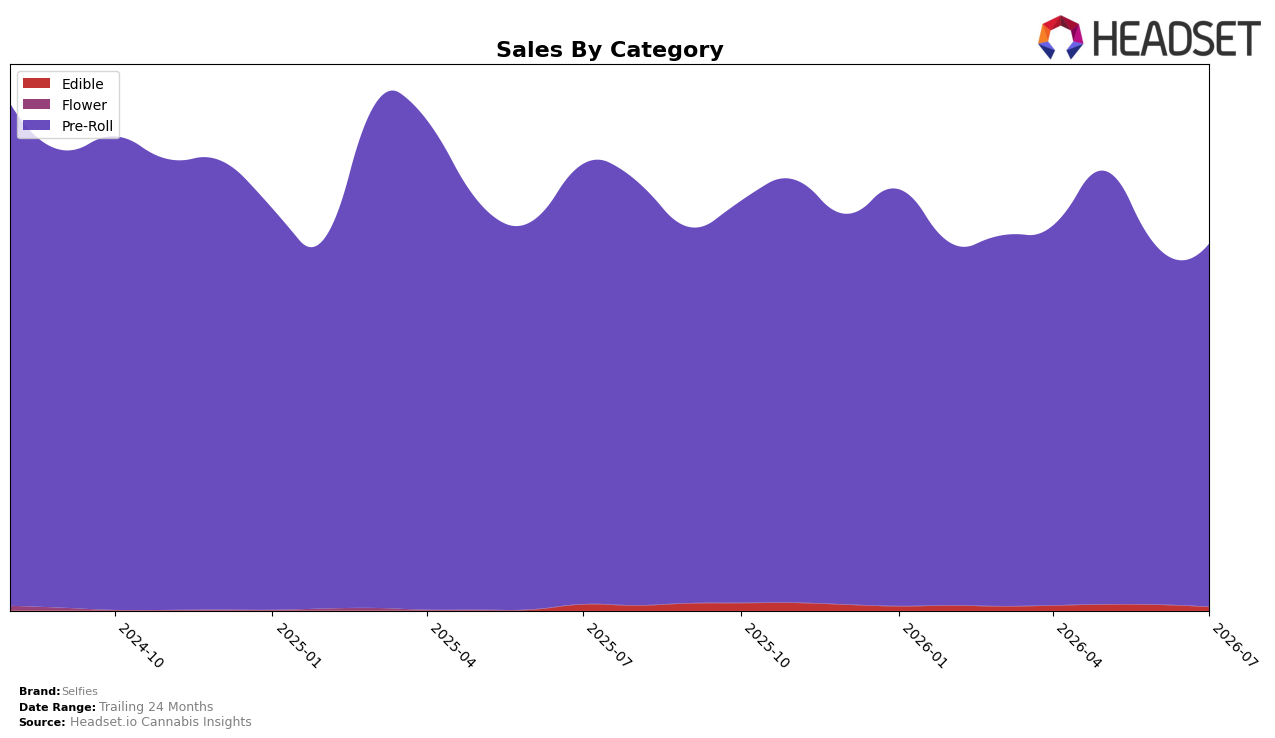

In July 2026, Selfies derived 99.09% of sales from Pre-Roll with a 1.68% month-over-month lift, while Edible held 0.91% share with a 39.78% month-over-month decline; year over year, Pre-Roll fell 17.55% and Edible contracted 43.33%. Overall brand sales declined 17.89% year over year alongside a 7.34% drop in average price, and within Pre-Roll the average price was $16.30, indicating the category is carrying volume stability despite annual contraction. The pattern implies Selfies is consolidating around Pre-Roll as its operative engine, using price to preserve velocity while de-emphasizing Edible.

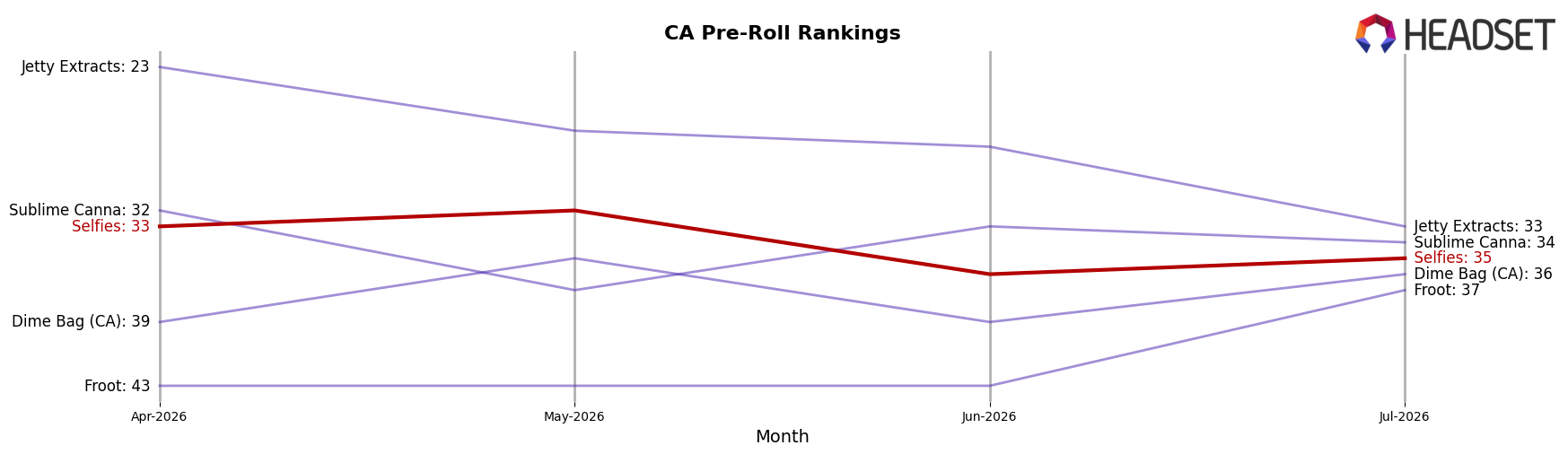

With a Pre-Roll rank of 35 in California and a 1.68% month-over-month uptick aligned to a 7.34% brand-wide price decrease, Selfies is positioning as a value-leaning Pre-Roll specialist rather than a multi-category player. The 0.91% Edible share and 39.78% month-over-month contraction, combined with a 26.46% sales decline over 24 months, indicate portfolio pruning toward a single-category focus where incremental price moves can influence rank and share more directly. This implies the brand’s near-term leverage sits in fine-tuning Pre-Roll price-pack architecture to translate small month-over-month gains into rank improvement while avoiding distraction from subscale Edible.

Competitive Landscape

Selfies sits at rank #35 in CA Pre-Roll in July 2026 after a 11-position YoY slide from #24, and a 2-position drop since April 2026’s #33, contrasting sharply with Jeeter holding #1 with 6.10% YoY sales growth and STIIIZY steady at #2 with 12.92% YoY growth; meanwhile, Kingpen remains #3 despite a -3.87% YoY decline and Sluggers Hit rose from #5 to #4 alongside 27.28% YoY growth, while CannaBiotix (CBX) climbed from #7 to #5 with 40.83% YoY growth; given Selfies’ peak at #21 in April 2025 and the subsequent descent to #35, the pattern implies a loss of relative velocity as faster-growing rivals consolidate the top ranks.

Notable Products

Wedding Cake Infused Pre-Roll (1.5g) posted the steepest movement in July 2026 with a -11.5% month-over-month drop and slid to rank 6, while Violet Ice Pre-Roll 2-Pack (1g) rose 43.5% to rank 3. Groupies - Durban Cookies Diamond Crumble Infused Pre-Roll (1.5g) grew 16.5% and held rank 1, outpacing moderate gains like 3.0% at rank 8 and 7.9% at rank 5 across the list. With eight of the top ten positioned in Pre-Roll formats and one 12-pack entry posting $33,580, the mix points to Selfies leaning into variety within pre-roll pack sizes as single-SKU volatility shifts demand toward multi-pack value.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.