Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

PUFF is stocked at 412 licensed dispensaries across California, New York, and 2 other states, 211 of them in California, with the deepest coverage in Los Angeles, Sacramento, Santa Rosa, San Jose, and Long Beach. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

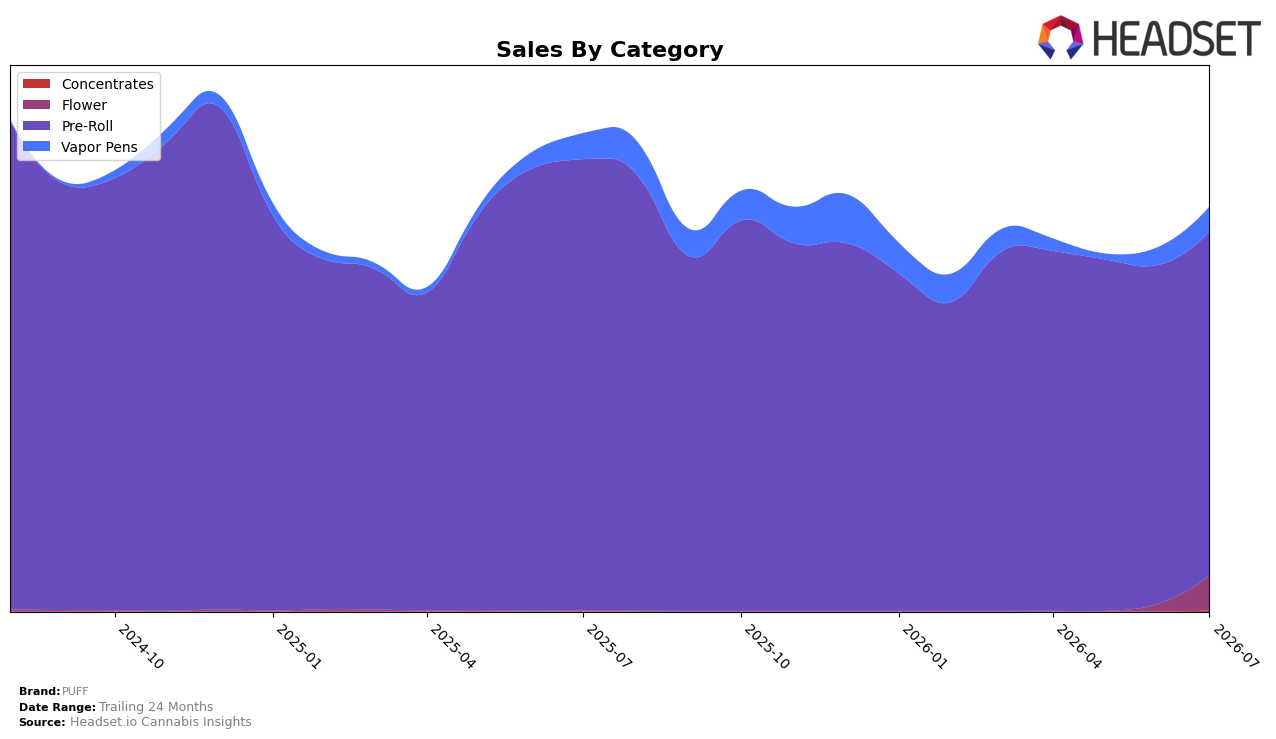

In July 2026, PUFF’s mix was dominated by Pre-Roll at 85.20% share, posting a year-over-year decline of 23.75% but a month-over-month uptick of 1.57%, while Vapor Pens held 6.04% share with a 5.22% YoY decline yet a 39.20% MoM rise. Flower expanded to 8.59% share on triple-digit momentum, rising 6,846.45% YoY and 389.85% MoM, whereas Concentrates were minimal at 0.18% share with no comparable change provided; at the same time, average price fell 6.07% YoY to $10.86, and the brand’s overall sales were down 15.41% YoY despite a 5.40% gain over 24 months. The pattern implies PUFF is partially offsetting Pre-Roll contraction with rapid re-entry or SKU expansion in Flower and a rebound in Vapor Pens, but the dominance of a shrinking Pre-Roll base keeps total sales pressured.

Holding rank 18 in Pre-Roll in California while Pre-Roll declines 23.75% YoY and grows only 1.57% MoM indicates PUFF’s core position is anchored in a softening segment, even as Flower’s 6,846.45% YoY and 389.85% MoM surges diversify exposure. With Vapor Pens improving 39.20% MoM despite a 5.22% YoY dip, and the brand’s average price down 6.07% YoY, the mix shift suggests PUFF is competing on value to stimulate trial in non-core formats while using Flower growth to hedge category risk. The implication is that sustained share gains will require reallocating assortment and marketing toward faster-growing subcategories without abandoning Pre-Roll scale, using pricing and SKU architecture to convert MoM momentum into durable share.

Competitive Landscape

PUFF sits at rank #18 in CA Pre-Roll for July 2026, down 2 positions year over year from #16, and flat versus April 2026 at #18, while its historical peak was #15 in June 2025; meanwhile, Jeeter held #1 both this July and a year ago and expanded sales by 6.1%, and Sluggers Hit climbed from #5 to #4 with a 27.3% YoY sales lift, indicating PUFF’s static-to-declining rank amid upward mobility at the top compresses room for mid-tier gains and implies the brand’s current trajectory risks further drift from its #15 peak without a share-accretive shift.

Notable Products

Lemon Cherry Gelato Pre-Roll (1g) posted the steepest movement in July 2026 with a -22.8% month-over-month drop while holding rank 6, contrasting sharply with OG Kush Pre-Roll (1g) up 48.4% at rank 3 and Uplift - Cereal Milk Pre-Roll (1g) up 9.3% at rank 1. Nine of the top ten are Pre-Roll SKUs, and within that set Grape Drink Pre-Roll (1g) advanced 30.2% at rank 4 as Orange Tree Pre-Roll (1g) rose 23.5% at rank 9, while Blue Dream Pre-Roll (1g) and Wedding Cake Pre-Roll (1g) slipped -4.2% and -5.5% at ranks 7 and 10. Sour Diesel Pre-Roll (1g) gained 9.4% at rank 2 alongside Alien OG Pre-Roll (1g) entering at rank 8 with $35,795, which, together with the declines clustered outside the top five, points to momentum concentrating in a handful of flavor-led SKUs. Taken together, the mix signals PUFF is consolidating share around a small set of faster-rising Pre-Rolls, implying near-term focus on a narrower hero-SKU lineup over broad variety.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.