Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

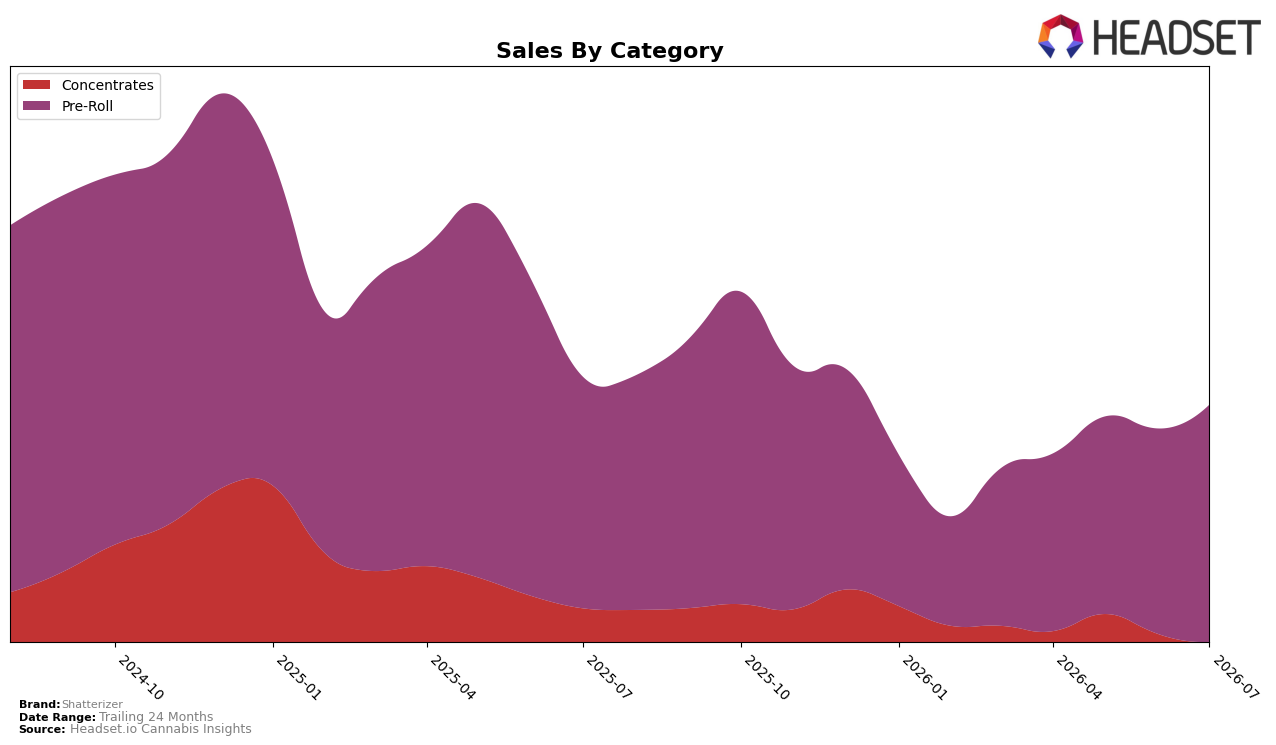

Shatterizer’s July 2026 mix is concentrated in Pre-Roll at 76.37% share with a 10.22% month-over-month lift and a 1.74% year-over-year gain, while Concentrates holds 23.63% share with a -6.96% month-over-month decline and a -24.00% year-over-year drop. The brand’s average price rose 5.69% year over year to $20.44 as Pre-Roll averaged $19.09 and Concentrates averaged $26.51, and overall brand sales fell -5.80% year over year alongside a -17.70% two-year change. With Pre-Roll ranked 51 in Ontario and expanding share month over month, the pattern implies Shatterizer is leaning further into a value-tilted Pre-Roll engine while de-emphasizing Concentrates as its contraction persists.

The sharper -24.00% year-over-year contraction in Concentrates versus the 1.74% year-over-year growth in Pre-Roll, combined with a 10.22% month-over-month Pre-Roll lift against a -6.96% month-over-month slide in Concentrates, indicates deliberate allocation toward faster-velocity formats despite the brand’s -5.80% year-over-year sales result. Given a 51 rank in Ontario for Pre-Roll and a category price gap where Concentrates’ $26.51 sits well above Pre-Roll’s $19.09 amid a 5.69% brand-wide price increase, the implication is that Shatterizer’s near-term positioning favors scale via accessible Pre-Rolls while allowing higher-priced Concentrates to contract, trading some premium margin for share stability in core joints.

Competitive Landscape

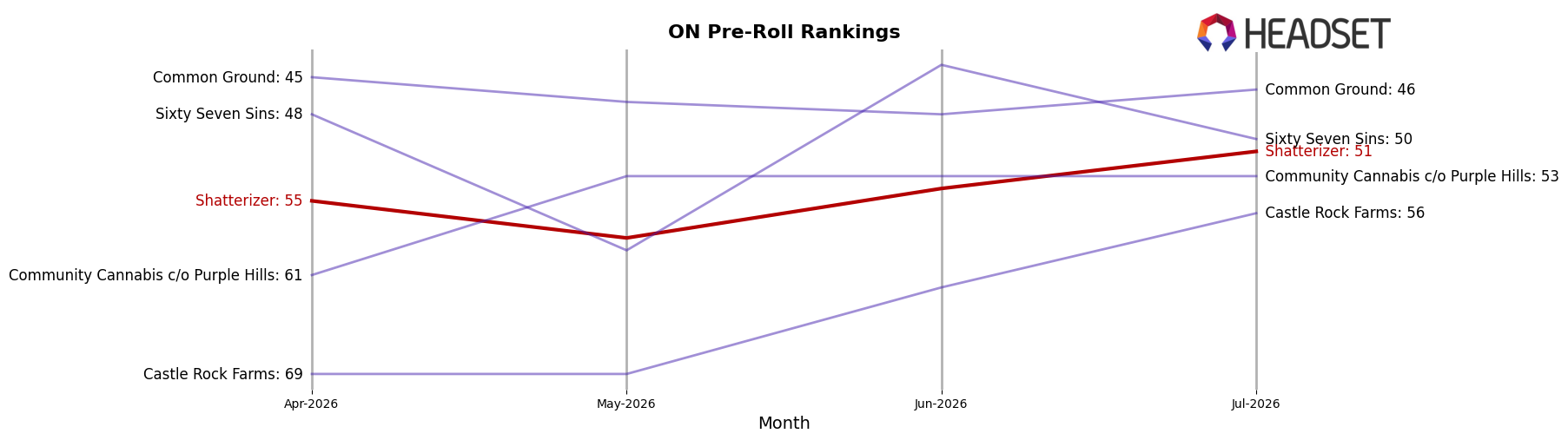

Shatterizer sits at rank #51 in ON Pre-Roll for July 2026, down 6 positions year over year from #45, and up 4 spots versus April 2026 when it was #55; versus its peak of #27 in December 2024, the current placement is 24 ranks lower and indicates a multi-quarter slide despite a short-term lift. Competitive movement is mixed: Back Forty / Back 40 Cannabis moved from #2 to #1 while growing sales 67.4% year over year, and General Admission slipped from #1 to #2 with sales down 23.2%, creating a top-tier shakeup that Shatterizer has not capitalized on. The combination of a 6-rank YoY decline and only a 4-rank rebound since April 2026 implies Shatterizer is losing relative velocity in a category where leaders are either consolidating gains or ceding ground.

Notable Products

Slurricane Double Infused Pre-Roll (1g) posted the steepest decline at -14.2% MoM while dropping to rank 4, contrasting with Pink Gas Shatter Infused Pre-Roll (1g) at rank 3 with a +44.4% MoM surge and 8 Ball Kush Shatter Double Infused Pre-Roll (1g) holding rank 1 at -2.6%. Five of the top six are Pre-Roll SKUs, and two Pink Gas formats appear in the top ten, indicating concentrated demand for infused formats over standalone concentrates, with 8 Ball Kush Shatter (1g) in Concentrates at rank 7 growing only +2.3%.

Granddaddy Purple Shatter Infused Pre-Roll 5-Pack (2.5g) slid -5.8% MoM at rank 5 while Electric Grapefruit Shatter Infused Pre-Roll 5-Pack (2.5g) rose +15.8% at rank 6, and the tied rank 8 entries each generated about $22.7k alongside double-digit MoM growth of +12.9% for Pink Gas Shatter Infused Pre-Roll 3-Pack (1.5g). The mix points to Shatterizer leaning into multi-pack and infused Pre-Rolls where share concentration and positive momentum outpace single-gram declines, implying portfolio prioritization around scalable infused SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.